10 Lakh Home Loan Monthly EMI Calculator: A Simple Beginner's Guide

Taking a home loan is an incredibly smart way to turn your property dreams into a physical reality. When you manage your budget with a mid-range loan size like 10 lakh, you must know exactly how much cash moves out of your wallet every month.

Planning your household budget requires highly accurate forecasting of your future bank commitments. Learning to use a 10 lakh home loan monthly EMI calculator structure helps you track your core numbers clearly, ensuring you never face unexpected financial surprises.

Direct Answer Snippets for Quick Reference

What is the monthly EMI for a 10 lakh home loan?

Using a standard 10 lakh home loan monthly EMI calculator, a 10 lakh loan at an 8.5% annual interest rate for 20 years results in a monthly payment of roughly 8,678. Shortening the tenure to 15 years increases your monthly installment to approximately 9,847.

How does your tenure alter the total interest payout?

Stretching your 10 lakh loan over a long 20-year cycle creates affordable monthly EMIs but results in a high interest accumulation of about 10.83 lakh. Choosing a shorter 10-year timeline increases your monthly payment but slashes your overall interest loss down to roughly 4.93 lakh.

What mathematical formula runs behind an EMI calculator?

The fundamental formula used by an automated housing calculator is $EMI = P \times R \times \frac{(1+R)^N}{(1+R)^N-1}$. Within this equation, $P$ represents your core principal loan amount, $R$ stands for your monthly interest fraction, and $N$ represents the total number of repayment months.

The Core Math Behind Your Monthly Installments

Before analyzing charts and grids, you must understand what happens behind the screen of a digital banking application. Every monthly installment you pay to a lender is split into two moving sections.

The first portion acts as your interest fee, which pays the lender for providing you with capital. The remaining portion serves as your principal payment, which chips away at your core 10 lakh debt.

In the initial years of your housing loan, the interest part dominates your monthly check. As your outstanding balance drops over the years, the equation flips, and your payments begin to erase the core principal balance at a rapid speed.

The Mathematical Housing Loan EMI Formula Explained

If you enjoy doing manual calculations or want to understand the exact mathematical logic, you can easily use the standard global banking equation.

The formula is written as follows:

$$EMI = P \times R \times \frac{(1+R)^N}{(1+R)^N-1}$$

To make this formula easy for beginners and students to understand, let us break down each individual letter symbol step by step:

P (Principal): This is the base amount of money you borrow from the bank. For our specific case study, $P$ equals exactly 1,00,0000 (10 lakh).

R (Monthly Interest Rate): Annual interest must be divided by 12 months. For example, if your annual rate is 8.5%, you calculate $R$ as $\frac{8.5}{12 \times 100} = 0.007083$ per month.

N (Number of Months): This represents your total repayment months. If you borrow for a standard 20-year period, your $N$ value equals $20 \times 12 = 240$ months.

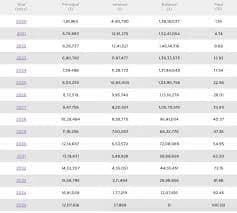

10 Lakh Home Loan EMI Calculations Across Diverse Timelines

To show you how the timeline choice impacts your pocketbook, let us analyze a fixed, realistic market interest rate of 8.5% per annum across three popular tenures.

1. The 10-Year Repayment Plan (The Fast Track)

Opting for a short 10-year timeline means you want to free your family from debt quickly. Your monthly home loan installment will stand at approximately 12,399.

The absolute benefit here is raw financial savings. You only pay a total interest of about 4.88 lakh over the entire decade, keeping your total repayment restricted to 14.88 lakh.

2. The 15-Year Repayment Plan (The Balanced Scale)

A 15-year timeline provides a highly practical middle ground for standard salaried households. Your calculated monthly payment drops down to roughly 9,847.

This plan keeps your monthly outgoings under the 10,000 mark. The total interest accumulated over fifteen years rises to 7.72 lakh, making your overall maturity payment 17.72 lakh.

3. The 20-Year Repayment Plan (The Low-Pressure Safety Net)

Stretching your loan timeline to 20 years brings your monthly commitment down to its lowest point of approximately 8,678.

While the low EMI leaves you with plenty of extra cash for children's school admissions and emergency savings, the long twenty-year interest accumulation climbs to 10.83 lakh. You end up paying back a total sum of 20.83 lakh to the bank.

Crucial Variables That Change Your Calculated EMI Output

An online calculator generates estimates based on standard inputs, but real-world banking contracts can shift due to individual personal habits.

CIBIL Credit Scores

Your personal credit tracking score acts as your financial reputation card. Maintaining an active CIBIL score above 750 encourages banks to offer you their absolute lowest interest rates.

A lower credit score forces the bank's automated algorithm to increase your interest margin, which inflates your monthly installment and increases your lifetime interest load.

Floating vs Fixed Interest Frameworks

Choosing a floating interest model means your monthly installments are tied directly to the central bank's repo rate changes. If the national lending rate drops, your loan cost goes down.

A fixed interest model locks your rate securely for the full duration of your loan, giving you completely predictable payments but missing out on helpful market rate cuts.

Tips to Outsmart Your Calculator and Save Capital

You do not have to follow a slow 20-year payment track just because your initial loan book says so. You can break free early using simple banking rules.

First, practice making regular small principal part-payments. Depositing just one extra month's EMI amount every single year can slash your total remaining timeline by up to four years.

Second, consider an automated step-up strategy. Ask your bank to increase your monthly installment value by 5% or 10% every year to match your natural annual workplace salary hikes.

Conclusion: Use Digital Tools for Smart Planning

Utilizing a 10 lakh home loan monthly EMI calculator methodology is the single most important step you can take before signing a final home buying agreement. It removes guesswork, highlights the long-term impact of interest rates, and helps you pick a timeline that protects your family's financial freedom.

Compare multiple tenures side by side, keep a close eye on hidden processing fees, and plan your repayments with discipline to build your dream home safely and comfortably.

Frequently Asked Questions (FAQs)

One: Can a student apply as a primary borrower using an EMI calculator?

A student can apply for a home loan, but they must add an earning parent or close relative as a primary financial co-applicant. Banks require a verified, steady monthly source of income to guarantee that future monthly installments are paid on time.

Two: Do online home loan calculators include processing fees and taxes?

No, standard online calculators display only the base principal and interest amounts. Upfront expenses like loan processing fees, legal documentation fees, property valuation charges, and government GST taxes must be paid separately during the loan application phase.

Three: Why does my bank balance statement show a different initial EMI date?

Your actual monthly repayment cycle begins only after the bank transfers the 10 lakh to the seller or releases the funds in stages for home construction. The calculator assumes instant disbursement, whereas real-world processing creates a tiny delay.

Four: Can I reduce my monthly housing loan installment if market interest rates drop?

Yes, if you hold a floating interest rate home loan, a market interest drop gives you two choices. You can either keep your monthly installment the same and shorten your total tenure months, or ask your bank to reduce your immediate monthly payout amount.

Five: What happens if I miss a monthly installment payment on my 10 lakh loan?

Missing an installment deadline damages your CIBIL credit score instantly and triggers standard banking bounce fees. Lenders will levy a penal interest charge on the overdue amount, which increases your total outstanding loan balance.

Six: Can I use an EMI calculator for home renovation and expansion loans?

Yes, the mathematical formula operates identically for home purchase, plot construction, and home renovation loans. You simply enter your required loan budget of 10 lakh and select your preferred interest rates to see your accurate monthly payout numbers.