20 Lakh Home Loan Repayment Tenure Options: A Beginner's Guide

Buying a home is a wonderful dream, but managing the long-term payment structure requires smart planning. When you apply for a housing loan, choosing how many years you take to return the money is just as important as finding the right property.

If you are planning to borrow a 20 lakh loan, banks will give you multiple timeline choices to clear your debt. The period you select to pay back the bank is known as the repayment tenure, and it has a massive impact on your routine family expenses.

This guide explores the various 20 lakh home loan repayment tenure options available in the Indian banking system. We will break down how different timelines alter your monthly outgoings and help you pick the best plan for your financial security.

Direct Answer Snippets for Quick Reference

What are the standard 20 lakh home loan repayment tenure options in India?

Indian banks and housing finance companies typically offer flexible repayment tenure options ranging from 5 years up to a maximum of 30 years. Most everyday borrowers choose between standard blocks of 15, 20, or 30 years to match their career stability and monthly savings.

Urban Money

How does a short 10-year tenure affect a 20 lakh home loan?

Opting for a short 10-year tenure on a 20 lakh loan keeps your overall interest costs remarkably low, meaning you get debt-free very quickly. However, it requires a much higher monthly payment, which can place significant pressure on your routine household budget.

Is a 30-year tenure recommended for a 20 lakh home loan?

A 30-year tenure is highly useful if you want the lowest possible monthly payment to keep your current budget comfortable. The major downside is that stretching a loan across three decades causes your long-term interest burden to swell heavily, making the loan far more expensive overall.

Understanding Your 20 Lakh Home Loan Repayment Tenure Options

When you take out a home loan, your Equated Monthly Installment (EMI) is calculated using three main puzzle pieces: the principal amount, the interest rate, and the repayment tenure. Since your loan amount is fixed at 20 lakhs, your tenure becomes the primary tool you can adjust to control your monthly budget.

SBI Home Loan

The repayment timeline creates a direct, natural trade-off in financial planning. If you increase the length of your loan, your monthly payment drops, but the total interest you pay over time goes up.

Conversely, shortening your timeline increases your immediate monthly burden but slashes your long-term interest costs dramatically. Let us look at how different tenures operate so you can see this trade-off clearly.

Short-Term Tenure Options (5 to 10 Years)

A short-term tenure is an excellent choice for individuals who want to clear their liabilities quickly and dislike holding long-term debt. It is highly suitable for mid-career professionals or business owners who expect a stable, high income in the immediate future.

Let us evaluate the math behind a 10-year tenure for a 20 lakh loan, assuming a standard competitive interest rate of 8.5% per annum.

Approximate Monthly EMI: Around 24,797

Total Interest Cost: Roughly 9.75 lakhs

Total Lifetime Payout: Around 29.75 lakhs

The great benefit here is financial freedom. You completely clear your housing debt in just a decade, and your total interest cost stays safely below your original 20 lakh principal amount. The downside is that you need to comfortably spare nearly 25,000 every single month.

Medium-Term Tenure Options (15 to 20 Years)

The 15 to 20-year window is the most popular sweet spot chosen by everyday home buyers in India. It offers a balanced compromise, preventing your regular monthly payments from being too high while keeping long-term interest accumulation under control.

Let us look at how the financial breakdown changes when we use the same 8.5% interest rate across these medium-term horizons.

20 Lakh Home Loan Cost Across Medium Tenures (At 8.5% Interest)

Repayment Tenure Option | Monthly EMI Amount | Total Interest Burden | Total Lifetime Cost |

|---|---|---|---|

15 Years | 19,695 | 15,45,066 | 35,45,066 |

20 Years | 17,356 | 21,65,541 | 41,65,541 |

Moving from a 15-year plan to a 20-year plan drops your regular monthly obligation by roughly 2,339. This reduction provides valuable breathing room for your household expenses. However, notice the long-term cost: extending the timeline by 5 years adds over 6.20 lakhs to your lifetime interest bill.

Long-Term Tenure Options (25 to 30 Years)

Long-term horizons are primarily engineered for young corporate beginners, first-time job holders, or families operating on a tight monthly salary constraint. Stretching the loan to 30 years brings your monthly liability down to the absolute minimum level possible.

Let us look at the financial layout for a maximum 30-year tenure at an 8.5% interest rate.

Approximate Monthly EMI: Around 15,378

Total Interest Cost: Roughly 35.36 lakhs

Total Lifetime Payout: Around 55.36 lakhs

While a monthly payment of 15,378 feels highly manageable and safe for a beginner, the long-term view requires careful thought. Over 30 years, you end up paying 35.36 lakhs in interest alone, which is significantly more than the initial 20 lakhs you borrowed from the bank.

Key Factors to Evaluate When Choosing Your Repayment Plan

You should not pick a timeline simply because it sounds common. Your choice among the 20 lakh home loan repayment tenure options should depend entirely on your unique life situation.

Consider these vital elements before finalizing your contract:

Your Current Age and Retirement Horizon

Banks legally require that your entire home loan balance must be fully settled by the time you reach your official retirement age, which is usually 60 years for salaried individuals. If you are applying for a loan at age 40, the bank will cap your maximum tenure option at 20 years.

Future Career and Income Growth

If you are a young professional expecting regular salary appraisals and performance bonuses over the next few years, you can safely opt for a longer tenure today to keep your initial risk low. As your income grows, you can make prepayments to cut the timeline short.

Other Vital Life Milestones

Remember that a home loan is a multi-decade commitment. Ensure that your chosen monthly payment leaves enough cash in your bank account to save for other crucial life milestones, such as your children's higher education, family medical security, and your personal retirement fund.

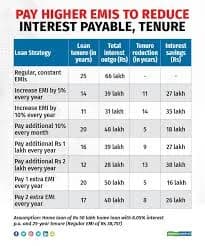

Smart Trick: The Power of Part-Prepayments

Choosing a long-term tenure option for safety does not mean you are locked into that timeline forever. You can use smart payment habits to manually shorten a 30-year loan into a 15-year loan.

Because Indian banks do not charge prepayment penalties on individual floating-rate loans, you can pay extra money toward your principal whenever you have spare cash.

The 1 Extra EMI Hack: Paying just one additional monthly installment every calendar year can cut your total loan tenure down by roughly 4 to 5 years.

Utilizing Annual Increments: Whenever you get an annual work appraisal, increase your monthly home loan payment by a small percentage. This simple adjustment slashes your long-term interest burden dramatically.

Conclusion

Evaluating your 20 lakh home loan repayment tenure options carefully is the secret to a stress-free homeownership journey. Medium-term tenures of 15 to 20 years offer an excellent middle ground for most families, while a 30-year plan serves as a practical safety net to keep initial monthly costs low.

Take the time to review your household cash flow, check your career retirement goals, and pick a timeline that allows you to live comfortably today while securing your financial future. With a balanced repayment plan and disciplined money habits, you can happily move into your new home with complete peace of mind.

Frequently Asked Questions (FAQs)

1. Can I change my 20 lakh home loan tenure after the loan is disbursed?

Yes, you can request your bank to modify your repayment tenure after disbursement. If your income increases, you can ask the bank to raise your monthly payment and shorten your overall tenure. If you face a financial crunch, you can request an extension, provided you stay within your maximum retirement age limits.

2. Is the interest rate the same for a 10-year and a 30-year home loan?

Generally, yes. Most leading Indian commercial banks charge the same base floating interest rate regardless of the tenure you select. Your interest rate depends primarily on your personal credit history and CIBIL score, though a few lenders might apply a tiny premium for maximum 30-year tenures due to long-term risk.

3. Do older individuals get access to a 30-year tenure option?

No, senior citizens or individuals close to retirement cannot access a 30-year repayment option. Lenders want to ensure the loan is cleared during your active earning phase, so they strictly limit the tenure to ensure full repayment by age 60 or 65.

4. Can I choose an unusual tenure like 13 or 17 years for my housing loan?

Yes, you do not have to stick to round numbers like 15 or 20 years. Banks allow you to customize your repayment timeline to any specific number of months, up to their maximum permissible limit. You can choose any custom timeline that fits your specific monthly target.

5. What happens to my tenure option if the RBI repo rate changes?

When the central bank adjusts the market repo rate, floating interest rates move accordingly. By default, when interest rates rise, banks automatically extend your remaining loan tenure to keep your monthly payment unchanged. If the tenure reaches your maximum age limit, the bank will increase your monthly payment instead.

ClearTax

6. Does a longer tenure affect my eligibility for other loans?

Yes, running a long-term home loan means that specific liability stays visible on your credit profile for decades. When you apply for a new car loan or a personal loan in the future, lenders will factor in your active home loan obligation, which can lower the amount they are willing to lend you.

For a deeper dive into modern borrowing strategies, watch this Home Loan 2026 Lowest Rates and EMI Hacks Guide. This video offers practical tips on navigating modern interest structures, improving your credit score, and choosing the perfect repayment path to save lakhs on your long-term borrowing journey.