Bank and NBFC Co-Lending Model Guidelines for Priority Sector MSME

Micro, Small, and Medium Enterprises (MSMEs) form the financial backbone of developing economies, creating millions of local jobs. However, small business owners often struggle to secure fast, affordable bank credit to grow their operations.

To solve this issue, the central bank created a cooperative financial system. This system is governed by the bank and nbfc co lending model guidelines for priority sector msme framework, combining the strengths of traditional public banks and private finance networks.

This introductory guide will explain how this joint credit system functions, who qualifies under priority sector targets, and how small business entrepreneurs benefit from these collaborative lending laws.

What are the bank and nbfc co-lending model guidelines for priority sector MSMEs?

These are official regulatory directions that allow commercial banks and Non-Banking Financial Companies (NBFCs) to fund a single MSME loan together. By blending a bank's cheap capital with an NBFC's wide geographic network, the framework delivers low-cost credit directly to underserved micro-enterprises.

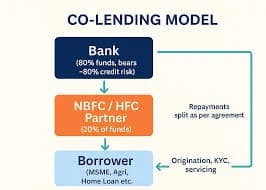

What is the standard risk-sharing ratio under the co-lending model?

Under standard co-lending arrangements, the funding partners share the loan exposure in a structured ratio. Typically, the primary commercial bank provides up to 80% of the loan capital, while the originating NBFC retains a minimum 10% to 20% share on its own balance books.

How does co-lending lower the interest rate for an MSME borrower?

The final interest rate is structured as a weighted average. The bank offers a lower interest rate on its large share of the loan, while the NBFC charges a slightly higher rate on its smaller portion. Blending these two rates results in an affordable repayment plan.

Understanding the Need for a Cooperative Lending Framework

Traditional commercial banks possess massive amounts of low-cost capital from public savings accounts. However, their strict document checks and limited rural branches make it difficult for them to reach deep micro-enterprises.

On the other side, private NBFCs excel at local doorstep servicing, utilizing digital tools to verify small shops instantly. However, their internal cost of borrowing funds is high, making their final loans expensive for regular shopkeepers.

The bank and nbfc co lending model guidelines for priority sector msme framework merges these two worlds. It uses the deep pockets of big banks and the unmatched operational reach of local financial networks.

Before extending credit to individual borrowers, the participating bank and the private NBFC must enter into a formal, board-approved Master Agreement.

This foundational legal contract details the operational guidelines, target industry sectors, and geographical borders of their credit partnership.

Mandatory Risk Retention: The originating NBFC must keep a clear financial stake in every single loan file to ensure they maintain strict credit checks.

The Escrow Account Rule: All incoming customer EMI repayments and outgoing loan amounts must route through a secure, automated escrow account to prevent fund mixing.

No Promoter Group Ties: Commercial banks are strictly banned from entering into co-lending agreements with private NBFCs that belong to their own corporate promoter group.

Benefits for Priority Sector MSME Borrowers

This joint lending architecture offers major practical advantages to small factories, boutique workshops, and local retail operations.

True Single-Point Customer Interface

Borrowers do not need to visit multiple corporate branch offices. The local NBFC manages the full lifecycle of the loan, running the initial document scans and managing doorstep cash collections.

Affordable Blended Pricing Models

Because a major portion of the loan comes directly from a bank’s low-cost fund vault, the total interest rate drops significantly compared to standalone private finance products.

Faster Processing Timelines

By using the advanced mobile onboarding apps built by modern fintech NBFCs, small business owners get their loans cleared within days rather than waiting weeks for old bank committees.

Asset Classification and Grievance Management Rights

The central bank protects your consumer rights carefully under this model. Lenders must follow strict transparency and reporting laws.

Both funding institutions must maintain a unified view of your loan account status. If a borrower defaults on an EMI, the account is classified uniformly across both balance sheets based on real-time data logs.

Consumer Protection Fact: The loan contract must explicitly name the primary institution responsible for solving customer complaints, providing a clear single point of contact for dispute resolution.

Conclusion: A Collaborative Path to Financial Inclusion

Following the bank and nbfc co lending model guidelines for priority sector msme framework creates an efficient path for small enterprise growth. It breaks down the old barriers of expensive capital and distant banking locations.

By understanding how this collaborative credit model functions, tracking your blended interest statements, and maintaining steady business deposits, you can utilize this system to scale your manufacturing startup smoothly.

Frequently Asked Questions

Can a service-sector micro-enterprise qualify for co-lending credit?

Yes. The priority sector definition covers both manufacturing and service-sector entities. Local logistics firms, small diagnostic labs, and computer repair centers easily qualify under the MSME classification guidelines.

Do I receive separate loan account numbers from the bank and the NBFC?

Behind the scenes, both lenders maintain individual accounts for their specific risk exposure. However, for the customer, the NBFC provides a single unified statement showing your total outstanding balance and integrated payments.

Can an NBFC charge hidden service fees on top of the blended interest rate?

No. All service charges, file processing fees, and documentation costs must be clearly disclosed upfront in the primary joint loan agreement. Lenders cannot introduce hidden fees later in the cycle.

What is Priority Sector Lending (PSL) status in Indian banking?

PSL is a central bank mandate requiring commercial banks to direct a specific percentage of their total bank credit to vital national sectors like agriculture, education, housing, and micro-scale MSMEs.

Can I apply for a co-lending loan if my business operates in a remote village?

Yes. The co-lending model was specifically designed to help rural enterprises. Lenders utilize the field networks of local NBFCs to provide secure funds to businesses outside major cities.

What should I do if a co-lending partner delays my loan closure document?

Once your final installment hits absolute zero, both institutions must clear their liens. You can lodge an official complaint with the named grievance desk, and if it is not resolved in thirty days, you can approach the Banking Ombudsman.