Direct Answer Snippet 1: What is a loan with a grace period?

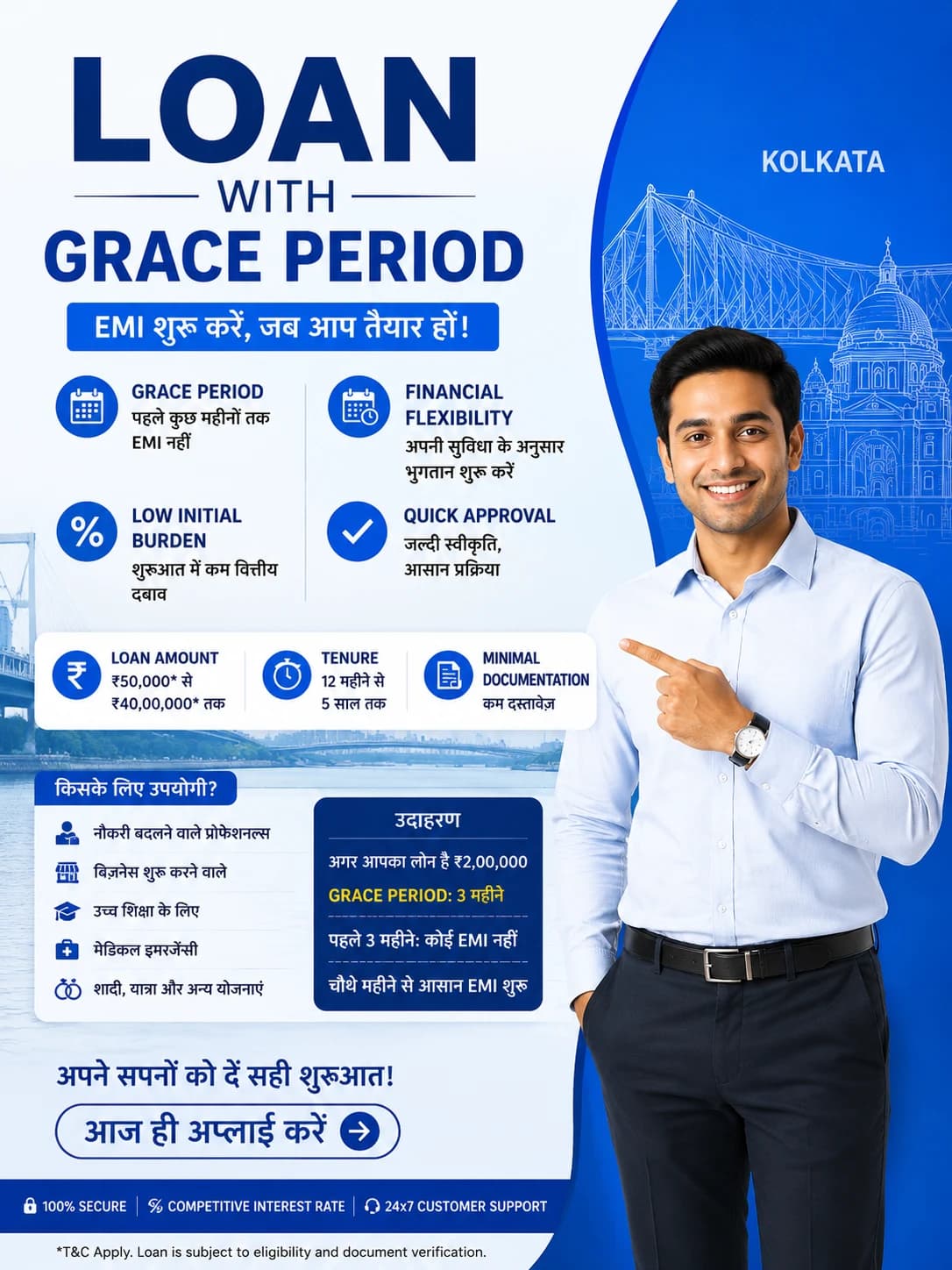

A loan with grace period is a borrowing agreement that gives you extra time before your first payment is due, or a monthly window after the due date to pay without penalties. During this time, you will not face late fees, and your credit score remains protected from negative reporting.

Direct Answer Snippet 2: Does interest accrue during a grace period?

Whether interest builds up during a loan with grace period depends on your specific contract. For some options, like subsidized student loans, interest does not accumulate. However, for most personal and auto loans, interest still grows daily even though you are not required to make a payment yet.

Direct Answer Snippet 3: How does a grace period affect your credit score?

Using a loan with grace period will not hurt your credit score as long as you pay within the specified timeframe. Lenders only report late payments to credit bureaus after the grace period ends. It acts as a safety net to keep your financial record clean during tight months.

Introduction

Taking out a loan is a major financial step that requires careful planning. Sometimes, unexpected life events can make it hard to start paying it back right away. This is where a loan with grace period becomes incredibly useful for borrowers.

A grace period offers breathing room when you need it most. It allows you to organize your finances before your monthly bills start arriving. Understanding how this feature works can save you money and protect your financial future.

In this guide, we will break down everything you need to know in simple terms. You will learn how these loans operate, the different types available, and how to use them wisely.

What is a Loan with Grace Period?

At its core, a loan with grace period is a standard lending agreement with a built-in safety net. It gives you a specific window of time where regular payment rules are relaxed. This window usually appears at the very start of the loan or as a monthly extension.

The Two Main Types of Grace Periods

There are two common ways lenders structure a loan with grace period:

The Post-Approval Window: This happens right after you receive the money. You might not have to make your first payment for 30, 60, or even 90 days.

The Monthly Due Date Extension: This is a recurring window every month. If your bill is due on the 1st, the lender might give you until the 15th to pay before charging a late fee.

Why Lenders Offer This Feature

Lenders offer a loan with grace period to make their financial products more attractive. It gives borrowers peace of mind, knowing they have a buffer zone if their payday aligns poorly with the bill due date.

It also builds trust between the borrower and the financial institution. When a lender offers flexibility, it shows they understand that real life does not always run on a rigid schedule.

How Interest Works During a Grace Period

This is the most critical part of a loan with grace period to understand. Many people confuse a grace period with "free money," but they are very different. You must know whether your loan is accruing interest during this time.

Subsidized vs. Unsubsidized Periods

In some cases, the government or the lender pays the interest for you during the buffer zone. This is common with a student loan grace period that is subsidized. Your balance stays exactly the same until you start paying.

With an unsubsidized loan with grace period, interest starts growing the moment the funds hit your account. Even though you do not have to make a payment today, the total amount you owe is getting bigger every single day.

Calculating the Long-Term Cost

If interest accrues, it will eventually capitalize. This means the unpaid interest gets added to your main loan balance. Future interest will then be calculated on this new, larger amount, costing you more over time.

Common Types of Loans with Grace Periods

Different financial products handle these buffer zones in unique ways. Let us look at how they apply to the most common types of borrowing.

Student Loans

The student loan grace period is the most famous example. Most federal and private student loans give graduates six months after leaving school before payments begin. This time is meant to help new graduates find a job and settle into a career.

Personal Loans

Finding a personal loan grace period is less common but highly valuable. Some lenders offer a 10 to 15-day window after your monthly due date. This helps if your monthly income arrives on a variable schedule.

Credit Cards

Credit cards are the most common form of an interest-free grace period. If you pay your statement balance in full every month by the due date, the card company will not charge you any interest on new purchases.

Benefits of Choosing a Loan with Grace Period

Opting for a loan with grace period offers several distinct advantages for your peace of mind and financial health.

Stress Reduction

Money issues are a leading cause of stress for students and adults alike. Having a few extra days or months to gather your funds takes the immediate pressure off your shoulders.

Protection for Your Credit Score

Late payments can ruin your credit score for years. A loan with grace period ensures that a delay of a few days will not be reported to the credit bureaus as a missed payment.

Better Cash Flow Management

If you are changing jobs or waiting for a bonus, the buffer zone allows you to align your bill payments with your actual income dates perfectly.

Potential Pitfalls to Watch Out For

While a loan with grace period sounds amazing, you must read the fine print carefully to avoid hidden traps.

The False Sense of Security

It is easy to forget about a debt when you do not have to pay it immediately. Some borrowers spend carelessly during the buffer zone, only to be shocked when the first real bill arrives.

Hidden Fees and Conditions

Some lenders state they offer a loan with grace period, but they attach strict conditions. For example, if you miss the extended deadline by even one minute, they might cancel the benefit and charge retroactively.

How to Maximize the Value of Your Grace Period

If your financial product has a buffer zone, you should use it strategically rather than just letting the time pass by passively.

Make Small Payments Anyway

If you have an unsubsidized loan with grace period, try to pay at least the interest while you wait. This prevents your total balance from growing before official repayment starts.

Build an Emergency Fund

Use the months without required payments to save up a cash buffer. This ensures that when the regular bills do start, you already have money set aside to cover them.

Conclusion

A loan with grace period is an excellent financial tool that offers flexibility, safety, and peace of mind. Whether you are dealing with a student loan grace period after graduation or a monthly buffer on a personal loan, it helps you manage your cash flow without fear of penalties.

However, honesty with yourself is key when managing debt. Always remember to check if interest is growing in the background, and use the extra time to plan your budget wisely. Treat the grace period as a tool for financial success, not an excuse to ignore your responsibilities.

Frequently Asked Questions

1. Does a personal loan grace period mean I do not have to pay interest?

No. For most personal loans, interest still accumulates every day during the buffer zone. The grace period simply means you will not be charged a late fee and your credit score will not be harmed if you pay within that window.

2. How long does a student loan grace period usually last?

A standard federal student loan grace period typically lasts for six months after you graduate, drop below half-time enrollment, or leave school. Private student loan lengths vary depending on the specific lender you chose.

3. Will using a loan with grace period hurt my credit score?

Using the grace period will not hurt your credit score. Lenders are only allowed to report your payment as late to the credit bureaus if you fail to pay after the entire grace period window has fully closed.

4. Can a lender cancel my grace period?

Yes, a lender can cancel a loan with grace period benefit if you violate the terms of your contract. For example, if you consistently bounce payments or break other terms, they may revoke the promotional window.

5. What is the difference between a grace period and loan deferment?

A grace period is an automatic window given at the start of a loan or monthly due date. Deferment is a formal request you make to pause payments later during the loan term due to financial hardship or job loss.

6. Should I pay off my loan during the interest-free grace period if I can?

Yes, absolutely. If you have the financial means to make payments during an interest-free grace period, you should do so. Every dollar you pay goes directly toward reducing your principal balance, saving you a lot of money in the long run.