Taking a personal loan or a business loan is a great way to manage financial needs in India. However, if you miss an Equated Monthly Installment (EMI) or fail to submit a document on time, banks historically applied heavy financial penalties.

For decades, lenders used these defaults to quietly compound your debt, making it incredibly difficult for an ordinary borrower to break free. To put an end to these unfair revenue practices, the central bank completely reformed the lending system.

By enforcing the modern non compliance penal charges vs penal interest rbi fair lending guidelines, the RBI has completely reshaped how penalties are structured. This beginner's guide explains your consumer rights and details how these changes protect your personal budget from compounding debt traps.

Direct Answer Snippets for Quick Understanding

What is the difference between penal charges and penal interest under RBI rules?

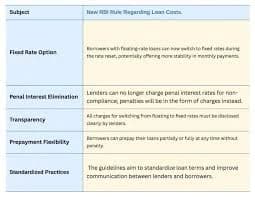

The core difference under the non compliance penal charges vs penal interest rbi fair lending guidelines is that penal interest increases your actual loan interest rate and compounds over time. Conversely, penal charges are flat, separate fees levied for defaults that can never be used to calculate further interest.

How do RBI fair lending guidelines prevent penalties from compounding?

The updated guidelines strictly prohibit the "capitalization" of penalties. This means lenders are completely banned from adding penalty fees to your outstanding loan principal. Because the penalty stays separate, banks cannot charge you "interest on interest" or "interest on penalties."

Can a bank use loan defaults to increase its corporate revenue?

No, the Reserve Bank of India explicitly states that penalties for loan defaults must only be used as a negative incentive to build credit discipline. Regulated financial entities are legally barred from using penal rates or hidden administrative charges as a tool to enhance their corporate revenue.

The Core Problem: How the Old Penal Interest System Worked

To appreciate the modern fair lending rules, it helps to understand how traditional banks used to penalize borrowers. Under the old system, when you defaulted on an EMI, lenders applied what was called "Penal Interest."

Lenders would add an extra percentage, usually two to three percent per year, directly on top of your existing interest rate. For example, if your base home loan rate was nine percent, it would instantly skyrocket to eleven percent on your overdue balance.

The worst part of this mechanism was a financial process called capitalization. The bank would merge that extra penal interest directly into your core loan principal at the end of the month. As a result, the next month you would pay regular interest on your original debt, plus interest on the previous penalty. This created a toxic debt spiral.

What Counts as a Material Non-Compliance?

Lenders do not just penalize you for missing your monthly EMI dates. There are several operational milestones inside a loan agreement, and breaking any of them counts as a contractual non-compliance. Lenders can apply penal charges for the following common triggers:

1. Loan Payment Defaults

This is the most frequent trigger. It happens when your bank account lacks a sufficient balance on your automated NACH mandate date, causing your monthly EMI payment to bounce.

2. Delay in Security and Asset Creation

For secured credits like home loans or car loans, you must submit your property registration documents or vehicle hypothecation papers within a fixed timeline. Failing to do so triggers a non-compliance fee.

3. Non-Submission of Crucial Financial Statements

Business owners borrowing working capital must submit regular stock statements, audited balance sheets, or net-worth certificates. Under the non compliance penal charges vs penal interest rbi fair lending guidelines, missing these submission deadlines results in standard penal charges rather than an increased interest rate.

Strict Rules Governing the Quantum of Penal Charges

The Reserve Bank of India did not just change the vocabulary from interest to charges; it also established rigid boundaries to ensure these fees remain completely fair and non-discriminatory.

The Test of Reasonableness

Banks cannot arbitrarily decide to charge an astronomical fee for a minor loan delay. The quantum of the penal charge must be directly proportional to the severity of the non-compliance, ensuring it acts as a basic deterrent rather than a financial punishment.

Uniformity Across Customer Profiles

Lenders are strictly banned from discriminating between individual borrowers within the same loan product category. For example, a bank cannot charge a higher default fee to an ordinary salaried citizen while giving a cheaper penalty rate to an influential borrower for the exact same category of non-compliance.

Corporate Ceilings and Board Approvals

Every financial institution must formalize a detailed, comprehensive Penal Charges Policy approved directly by their top Board of Directors. Furthermore, the penal charges applied to individual borrowers for personal use can never be higher than the fees levied on commercial corporate entities.

Summary Summary Matrix: Penal Interest vs. Penal Charges

Financial Operational Feature | Old Old Penal Interest Regime | Modern Modern Penal Charges Regime |

Basic Core Structure | Added directly to the loan interest percentage | Kept as an independent, flat physical fee |

Compounding Tracking | High (Capitalized into principal every month) | Strictly Banned (Zero interest on penalties) |

Primary Lender Intent | Often utilized as an extra revenue stream | Used solely to build consumer credit discipline |

Upfront Disclosure | Frequently buried deep in fine print pages | Must be highlighted in the Key Fact Statement |

How to Verify Penal Charges on Your Active Loan

To ensure that your lender is fully complying with the central bank's fair lending guidelines, you should run a quick audit on your personal loan account profile.

Start by opening your official Key Fact Statement (KFS) or your Most Important Terms and Conditions (MITC) sheet. Lenders are required by law to display the exact fee structure for every single type of non-compliance transparently on these forms.

When you receive an automated late-payment reminder message on your mobile phone, check if the bank clearly mentions the exact penal charge amount and the specific reason for it. If you notice that a digital app is still trying to compound your penalties or alter your annual interest rate after a delay, lodge an immediate internal corporate complaint or escalate the matter directly to the online RBI Ombudsman portal.

Conclusion

The non compliance penal charges vs penal interest rbi fair lending guidelines represent a monumental victory for consumer protection in India. By eliminating the predatory practice of interest capitalization, the central bank has built a safe environment where a temporary financial emergency will not snowball into a permanent debt trap.

Always remember that while you are legally bound to repay the real money you borrow, you have an absolute right to fair, honest, and transparent treatment. Stay aware of your credit deadlines, read your Key Fact Statements carefully, and use these protective guidelines to keep your financial journey fully safe and secure.

Frequently Asked Questions (FAQs)

1. Do the new RBI penal charge guidelines apply to credit cards?

No, the specific non compliance penal charges vs penal interest rbi fair lending guidelines do not apply to credit card accounts. Credit cards operate under a separate master directive, which allows card issuers to continue charging interest on unpaid balances according to their standard billing cycles.

2. Can a bank charge Goods and Services Tax (GST) on penal charges?

Yes, because penal charges are classified as an independent service fee rather than a direct interest payout, banks are required to levy the standard operational Goods and Services Tax (GST) on top of the penalty fee amount.

3. What is a reasonable grace period before penal charges are applied?

Many compliant banks and fintech platforms follow guidelines from the Fintech Association for Consumer Empowerment (FACE) and offer a basic grace period of up to three working days for accidental delays, though this remains an internal discretionary policy.

4. If I do not pay a penal charge, can the bank levy a penalty on that unpaid fee?

No, lenders are strictly banned from charging secondary penalties on an unpaid penal charge amount. Additional penal components cannot be piled on top of old, outstanding penalty accounts under the current fair lending framework.

5. Does a penal charge still hurt my CIBIL credit score?

Yes, while the new rules stop your debt from compounding excessively, missing a repayment deadline still counts as a default. The lender will report this delay to the credit bureaus, which will lower your overall CIBIL score.

6. Do these fair lending guidelines apply to older loans signed before 2024?

Yes, the RBI mandated that all existing personal and business loans must be completely transitioned into the new, non-compounding penal charges system during their next official contract review or renewal cycle.