Personal Loan Eligibility Calculator: Your Quick Guide

Imagine needing ₹50,000 for an urgent medical expense. You approach a lender, only to be told your application is rejected. Disheartening, right?

Now, picture this: you use an online eligibility calculator beforehand, discover you qualify for ₹60,000, and secure the needed funds smoothly. This is the power of understanding your personal funds eligibility.

Many applicants focus solely on interest rates. What most people miss is that eligibility is the first hurdle. Without meeting it, the rate is irrelevant. This guide demystifies personal borrowing eligibility, explaining what lenders look for and how a calculator can save you time and potential rejection.

Why financing Eligibility Matters

Lenders assess your eligibility to gauge your ability to repay the credit. It's a risk management tool for them and a crucial step for you. A reliable personal financing eligibility calculator provides an estimate of how much you can borrow. This prevents disappointment and helps you plan your finances better.

- Risk Mitigation for Lenders: Ensures they lend to creditworthy individuals.

- Financial Planning for Borrowers: Helps set realistic borrowing expectations.

- Saves Time: Avoids applying to multiple institutions without knowing your chances.

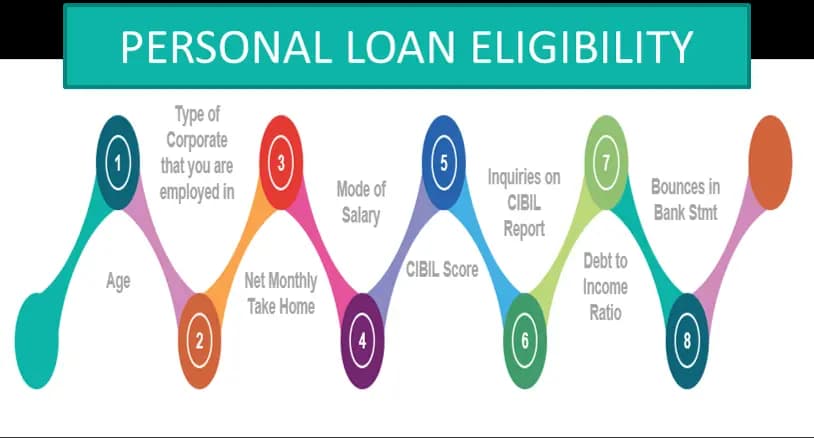

Factors Influencing Your Eligibility

Several key factors determine if you qualify for a personal borrowing. Lenders review these meticulously.

- Credit Score (CIBIL Score): This is a primary indicator of your creditworthiness. A score above 750 is generally considered good by most institutions. A lower score might lead to rejection or higher finance charge rates. How does this affect your CIBIL score? Your payment history, credit utilisation, and length of credit history all contribute significantly.

- Income: Your monthly or annual income shows your capacity to handle funds instalments. Lenders often have a minimum income requirement, typically ranging from ₹15,000 to ₹30,000 per month, varying by lender and location.

- Debt-to-Income Ratio (DTI): This compares your monthly debt obligations (including the potential new credit EMI) to your gross monthly income. A lower DTI (ideally below 40%) is favourable.

- Age: Most lenders require applicants to be between 21 and 60 years old. Salaried individuals might have a higher upper age limit than self-employed ones.

- Employment Stability: Lenders prefer applicants with a stable employment history, usually requiring at least 6 months to 2 years with the current employer. For self-employed individuals, a minimum business vintage (e.g., 3 years) is often mandated.

- Existing Loans: Having multiple active loans can reduce your eligibility for new financing.

The reality is, lenders use proprietary algorithms to weigh these factors. While a high CIBIL score is beneficial, a strong income can sometimes compensate for a slightly lower score, and vice-versa.

How to Use a Personal funds Eligibility Calculator

A personal financing eligibility calculator on platforms like Six Finance is a simple yet powerful tool. It provides an instant estimate of your borrowing potential.

Step-by-Step Walkthrough

- Visit Six Finance: Navigate to the personal credit section on our platform.

- Locate the Calculator: Find the 'Personal financing Eligibility Calculator' tool.

- Enter Basic Details: You'll typically need to provide information such as:

- Your age

- Monthly income (Net or Gross, as specified)

- Existing monthly EMI obligations (if any)

- Employment type (Salaried or Self-employed)

- Years of work experience / Business vintage

- Input CIBIL Score (Optional but Recommended): Some calculators allow you to input your estimated CIBIL score for a more accurate projection.

- Submit Information: Click the 'Calculate' or 'Check Eligibility' button.

- View Results: The calculator will display an estimated borrowing amount you might be eligible for. It may also provide a range based on different lender criteria.

In practice, the calculator uses the data you provide against predefined lender criteria. It’s an approximation, not a final borrowing sanction.

What the Results Mean

The output gives you a figure representing the potential funds amount. This helps you:

- Set Expectations: Know what credit amount to apply for.

- Shortlist Lenders: Identify institutions likely to approve your application.

- Budget Appropriately: Plan your finances around the estimated EMI.

Remember, this is an estimate. Actual approval depends on the lender's final verification and your specific financial profile at the time of application.

Do's and Don'ts for funds Eligibility

Maximise your chances of approval by following these guidelines.

Do's

- Maintain a Good CIBIL Score: Pay all your EMIs and credit card bills on time. Avoid frequent credit inquiries.

- Provide Accurate Information: Ensure all details entered in the calculator and application are truthful.

- Calculate Your Repayment Capacity: Ensure the potential EMI fits comfortably within your budget. The RBI suggests keeping total EMIs below 40% of your net monthly income.

- Check Pre-approved Offers: Sometimes, lenders offer pre-approved loans based on your existing relationship, simplifying the process.

- Understand Lender Criteria: Different institutions have varying eligibility benchmarks.

Don'ts

- Don't Apply with Multiple Lenders Simultaneously: Multiple rejected applications can negatively impact your credit score.

- Don't Overestimate Your Income: Be realistic about your earnings and monthly instalment capacity.

- Don't Ignore Existing Debts: Factor in all current credit obligations.

- Don't Use the Calculator as a Guarantee: It's an estimation tool, not a financing sanction.

FAQs on Personal funds Eligibility

What is the minimum CIBIL score required for a personal credit?

While some NBFCs (Non-Banking Financial Companies) might consider scores as low as 650-700, most banks prefer a CIBIL score of 750 or above for optimal financing terms. A lower score might result in financing rejection or a higher rate rate.

The numbers tell a clear story.

How does my employment type affect eligibility?

Salaried individuals are often seen as having more stable income streams, making them generally easier to approve. Self-employed applicants usually need to demonstrate longer business continuity and provide more documentation (like ITRs, financial statements) to prove income stability.

Can I get a personal credit with a low income?

It depends on the lender's minimum income criteria and your overall financial profile. Some lenders specialise in offering loans to individuals with lower incomes, but the borrowing amount might be smaller, and the rate rate potentially higher. Your DTI ratio is also critical here.

What if my eligibility is lower than expected?

Focus on improving your CIBIL score by paying bills on time. Reduce existing debt if possible. Consider applying with lenders who have more lenient eligibility criteria or explore options like a joint funds with a co-applicant who has a strong financial profile.

How long does the eligibility check take?

Online calculators provide instant estimates. The lender's internal assessment might take a few hours to a couple of days, while the final funds approval process, including document verification, can take anywhere from 24 hours to a week, depending on the institution.

Small differences in rates compound significantly.

Final Thoughts on credit Readiness

Understanding your personal borrowing eligibility is the first step towards securing necessary financing. By using an online eligibility calculator, you gain valuable insights into your borrowing potential.

This proactive approach empowers you to make informed decisions, approach the right lenders, and avoid unnecessary rejections. Always remember that the calculator provides an estimate; the final decision rests with the lending institution after thorough verification.

Disclaimer: This content is for educational purposes only and does not constitute personalized financial advice. Eligibility criteria and financing offers can vary significantly between lenders and are subject to change. Always review the lender's terms and conditions carefully before applying for any credit product.

Always consult a certified financial advisor before making major financial decisions.