What is a small personal loan? A small personal loan is a type of installment debt, usually ranging from $500 to $5,000. It is typically unsecured, meaning no collateral is required. Borrowers receive a lump sum and repay it through fixed monthly payments, including interest, over a term of 12 to 60 months.

How do I qualify for a small personal loan? To qualify for a small personal loan, lenders typically require proof of steady income, a valid ID, and a decent credit score. While some lenders cater to those with poor credit, a higher score usually results in lower interest rates and better repayment terms.

Where can I get a small personal loan quickly? You can obtain a small personal loan from online lenders, credit unions, or traditional banks. Online lenders often provide the fastest service, sometimes funding loans within 24 hours. Credit unions are excellent for members seeking lower rates and more personalized service.

Understanding the Basics of a Small Personal Loan

When you start looking for a small personal loan, you will notice they differ from credit cards.

Unlike a credit card, which is "revolving" credit, a loan provides a one-time payment.

You know exactly how much you owe every month, which makes budgeting much easier for students and beginners.

How Loan Amounts Work

Most lenders define a small personal loan as anything under $5,000.

Some specialized lenders may even offer "micro-loans" as low as $300 to $500 for emergencies.

The amount you can borrow depends heavily on your monthly income and your existing debt levels.

Fixed vs. Variable Interest Rates

Most personal loans come with a fixed interest rate.

This means your monthly payment will never change during the life of the loan.

Variable rates can start lower but may increase over time, making them riskier for a small personal loan.

Why People Choose Small Personal Loans

There are several common reasons why someone might seek out a small personal loan.

Since these loans are versatile, the money can be used for almost any personal expense.

Emergency Expenses

Life is unpredictable, and sometimes you need cash for a medical bill or an urgent home repair.

A small personal loan can provide those funds faster than saving up over several months.

Debt Consolidation

If you have multiple high-interest credit cards, you can use a loan to pay them off.

This leaves you with just one monthly payment, often at a lower interest rate.

Building Credit History

For students or beginners, taking out a small personal loan and paying it back on time is a great way to build credit.

Consistently making payments shows future lenders that you are a responsible borrower.

Where to Find a Small Personal Loan

Not all lenders are the same, and where you go can change the cost of your loan significantly.

Online Lenders

Online lenders are popular because they are fast and often have lower overhead costs.

They use automated systems to check your credit, allowing for "pre-qualification" in minutes.

Credit Unions

Credit unions are member-owned, meaning they often offer lower rates than big banks.

If you are a student, check if your university has a credit union, as they often have specialized small personal loan products.

Traditional Banks

Large banks offer personal loans, but they often have stricter credit requirements.

If you already have a checking account with a bank, they might offer you a loyalty discount on your rate.

Eligibility: What You Need to Apply

Before you apply for a small personal loan, gather your documents to speed up the process.

Lenders want to make sure you can afford to pay them back without falling into financial distress.

Credit Score Requirements

Your credit score is a three-digit number that represents your "creditworthiness."

A score of 670 or higher is generally considered good and will get you the best rates.

However, some lenders specialize in "bad credit loans" if your score is below 580.

Proof of Income

Lenders will ask for recent pay stubs, bank statements, or tax returns.

They want to see a consistent flow of money entering your account each month.

Debt-to-Income Ratio (DTI)

This is a comparison of how much you earn versus how much you owe in debt.

Lenders prefer a DTI below 36% to ensure you aren't overextended.

The Hidden Costs of Borrowing

A small personal loan isn't just about the interest rate; there are other fees to watch out for.

Always read the "fine print" before signing any loan agreement.

Origination Fees

Some lenders charge a fee just for processing the loan, usually between 1% and 8%.

This fee is often taken out of the loan balance before you even receive the money.

Prepayment Penalties

Surprisingly, some lenders charge you a fee if you pay the loan off early.

Look for a small personal loan with "no prepayment penalties" so you can save on interest by paying extra when you can.

Late Payment Fees

Missing a payment can result in a flat fee or a percentage of the amount due.

More importantly, late payments can damage your credit score significantly.

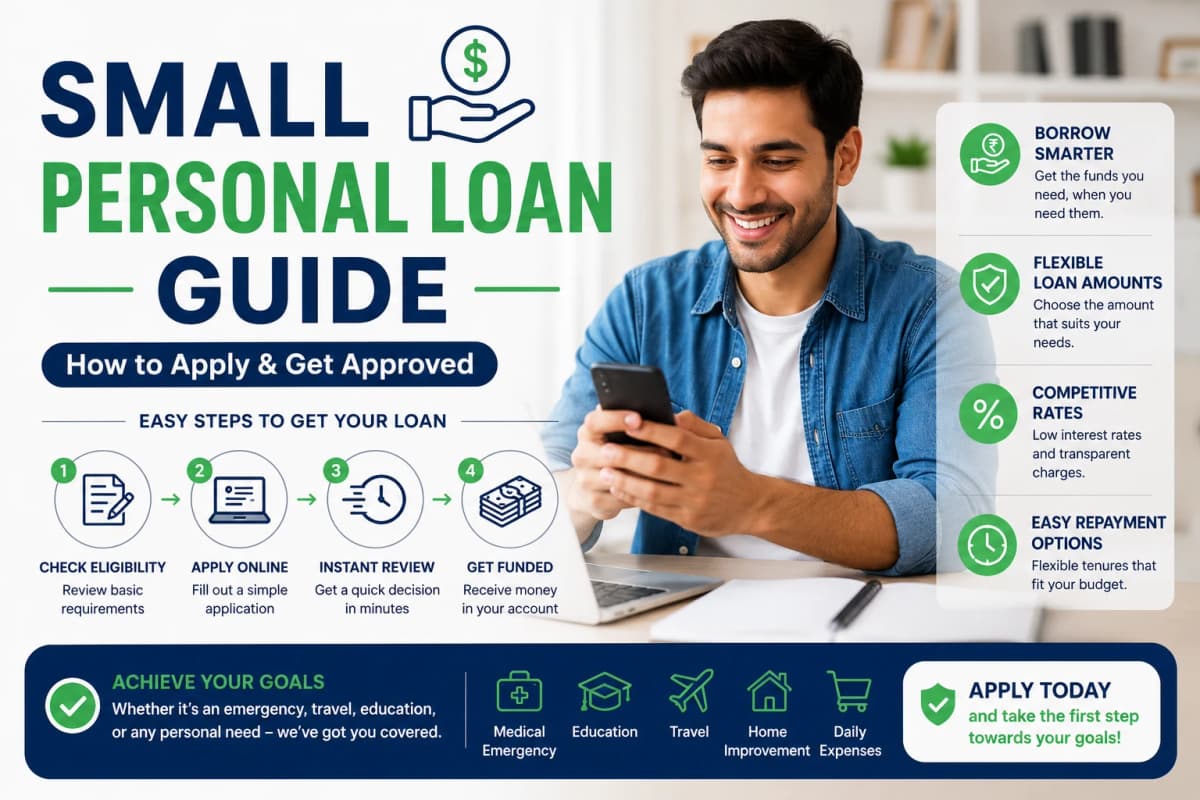

How to Apply for a Small Personal Loan: Step-by-Step

If you’ve decided that a loan is right for you, follow these steps to ensure a smooth process.

Step 1: Check Your Credit

Get a free copy of your credit report to check for errors.

If your score is low, try to pay down some credit card debt before applying.

Step 2: Compare Multiple Lenders

Don't settle for the first offer you see.

Use "soft pull" pre-qualification tools that let you see rates without hurting your credit score.

Step 3: Submit a Formal Application

Once you pick a lender, you will provide your Social Security number and income details.

This will trigger a "hard" credit pull, which may temporarily dip your credit score by a few points.

Step 4: Review and Sign

Check the Annual Percentage Rate (APR), which includes both interest and fees.

If everything looks correct, sign the digital documents and wait for the funds.

Tips for Managing Your Loan Responsibly

Getting the money is the easy part; paying it back requires discipline.

Set Up Autopay

Most lenders offer a small interest rate discount (usually 0.25%) if you use autopay.

It also ensures you never forget a payment and avoid late fees.

Pay More Than the Minimum

If your budget allows, add an extra $20 or $50 to your monthly payment.

This reduces the principal faster and lowers the total interest you pay over time.

Avoid Taking Multiple Loans

It can be tempting to take out another small personal loan once you get the first one.

However, "stacking" debt can lead to a cycle that is very hard to break.

Conclusion

A small personal loan can be a powerful tool for achieving your goals or handling emergencies.

By choosing the right lender and understanding the total cost of borrowing, you can protect your financial future.

Always remember to borrow only what you need and have a clear plan for repayment.

With a bit of research and careful planning, you can navigate the world of personal finance with confidence.

Frequently Asked Questions (FAQs)

1. Will applying for a small personal loan hurt my credit score? When you first check your rates via "pre-qualification," it usually does not affect your score. However, once you officially apply, the lender performs a "hard inquiry," which can cause a small, temporary drop in your score.

2. How long does it take to get the money? Online lenders are incredibly fast and can often deposit funds into your bank account within one to two business days. Traditional banks may take a week or longer to process the paperwork.

3. Can I get a loan if I am currently unemployed? It is difficult but not impossible. You must show an alternative source of income, such as Social Security benefits, investment income, or a co-signer who is employed and has good credit.

4. What is the difference between APR and interest rate? The interest rate is the cost of borrowing the principal amount. The APR (Annual Percentage Rate) includes the interest rate PLUS any fees like origination fees, giving you a more accurate picture of the total cost.

5. Is a payday loan the same as a small personal loan? No. Payday loans are high-interest, short-term loans that must be paid back by your next paycheck. A small personal loan has much lower interest rates and is paid back over months or years.

6. Can I use a personal loan to start a small business? Yes, most lenders allow you to use personal loan funds for business expenses. However, if the business fails, you are still personally responsible for paying back the loan.