Building or buying a home is a milestone that brings immense joy and stability to your family. When your personal savings fall slightly short, a mid-range budget home loan provides the perfect financial bridge.

Planning your finances before signing a bank contract ensures you do not strain your household budget. Understanding how a 10 lakh home loan EMI for 20 years operates helps you manage your monthly cash flow with zero stress.

Direct Answer Snippets for Quick Reference

What is the monthly EMI for a 10 lakh home loan for 20 years?

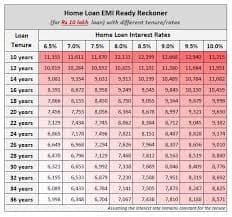

At an average interest rate of 8.5% per annum, the monthly installment for a 10 lakh home loan EMI for 20 years is approximately 8,678. If the interest rate rises to 9.5% per annum, the monthly installment climbs to around 9,321.

How much total interest do you pay over 20 years?

Borrowing 10 lakh at an 8.5% interest rate for 20 years results in a total interest payout of roughly 10.83 lakh. This means your total repayment to the financial institution over two decades will stand at approximately 20.83 lakh.

Is a 20-year tenure good for a 10 lakh loan?

Yes, a 20-year tenure offers an excellent middle ground for middle-class households. It provides highly affordable monthly installments that fit easily into a standard salary, while keeping the long-term interest cost much lower than a 30-year layout.

What Goes Inside Your Monthly Home Loan EMI?

Before diving deep into the exact numbers, you must understand how a bank calculates your Equated Monthly Installment (EMI). Every monthly payment you send to the lender is divided into two distinct parts.

The first part is the principal component, which directly reduces the actual 10 lakh debt you borrowed. The second part is the interest component, which is the fee the bank charges you every month for utilizing their capital.

In the initial years of a 20-year tenure, a larger portion of your monthly installment goes toward clearing the interest. As the years roll by, this equation flips, and your payments actively slash the core principal balance.

Detailed EMI Breakdowns Across Different Interest Rates

Home loan interest rates in India are flexible and shift based on your credit score and choice of lender. Let us examine how your monthly outgoings change across realistic interest rate scales.

ICICI Bank

Option A: Prime Bank Rates (8.5% Interest Per Annum)

If you possess a stellar credit score above 750, top public sector banks can offer you a highly competitive rate of around 8.5% per annum.

Axis Bank

Under this framework, your monthly installment sits at 8,678. Over 20 years, you pay an interest value of 10.83 lakh, bringing your total payment closure to 20.83 lakh.

Option B: Standard Market Rates (9.0% Interest Per Annum)

A 9.0% rate is the most common bracket for regular salaried individuals and first-time property buyers across urban towns.

Here, your 10 lakh home loan EMI for 20 years calculates to roughly 8,997 per month. The total interest payable over twenty years hits 11.59 lakh, and the overall repayment reaches 21.59 lakh.

Option C: Small Finance Banks & HFCs (9.5% Interest Per Annum)

If you are self-employed or lack formal income tax return forms, you might secure a rate around 9.5% per annum from housing finance firms.

Your monthly commitment rises to 9,321 under this structure. The interest accumulation over two decades reaches 12.37 lakh, making the total maturity repayment around 22.37 lakh.

Key Factors That Alter Your 10 Lakh Home Loan EMI

Your final monthly obligation is not random. Lenders utilize specific personal benchmarks to calibrate your exact interest parameters.

1. The Credit Score Scale

Your credit report card is the very first document a loan officer evaluates. A high credit score shows you pay your bills with extreme discipline.

Maintaining a credit score above 750 unlocks the lowest interest brackets, which directly drops your monthly installment amount and saves you thousands over 20 years.

ClearTax

2. Employment Categories

Salaried individuals working with government departments or established corporate brands get access to cheaper interest models.

Self-employed professionals face slightly higher margins due to the seasonal nature of business earnings, which slightly inflates their monthly home loan installment.

3. The Loan-to-Value (LTV) Ratios

The down payment you make out of your personal pocket changes the bank's risk level. If you pay a large amount upfront, the bank feels highly secure.

ICICI Bank

A lower loan-to-value ratio allows you to negotiate a lower interest rate, reducing your overall debt burden right from day one.

v

You do not have to stick to a rigid 20-year payment timeline just because your initial loan book says so. You can actively outsmart the system using smart banking rules.

Initiate Yearly Part-Payments

Whenever you receive an annual workplace bonus, an insurance maturity payout, or extra business profits, use that money to make a principal part-payment.

Even depositing just one extra month's installment value every single year can cut down your total remaining tenure by almost three to four years.

Use the Step-Up Payment Plan

As you gain experience in your career, your monthly earnings will naturally expand. You can request your lender to increase your EMI value by 5% or 10% every year.

This gradual pacing matches your natural career growth and aggressively erases your core principal balance long before the 20-year deadline arrives.

Conclusion: Plan Logically for a Happy Home

Choosing a 10 lakh home loan EMI for 20 years is a highly balanced, intelligent financial strategy for modern home buyers. It keeps your monthly commitment under the 10,000 threshold, allowing you to manage children's school fees, emergency medical funds, and kitchen bills comfortably.

Always check your credit health before applying, read the processing fee clauses thoroughly, and focus on clearing your principal balance early through small part-payments. Step into your beautiful new home with absolute clarity and complete peace of mind.

Frequently Asked Questions (FAQs)

One: Can a 45-year-old applicant get a 10 lakh home loan for a 20-year tenure?

Yes, a 45-year-old applicant can secure a 20-year tenure, provided they show strong income proof or possess a stable business model. Banks require the entire loan amount to be fully paid back by the time the applicant reaches 65 to 70 years of age.

Two: Are there any penalties if I pay off my 10 lakh home loan before 20 years?

According to the Reserve Bank of India guidelines, banks cannot charge any prepayment or foreclosure penalties on floating interest rate home loans. You can pay back your outstanding principal using your personal savings whenever you wish without paying extra fees.

Three: Does the 10 lakh home loan EMI change if market interest rates alter?

Yes, if you choose a floating interest rate loan, your monthly outgoings can change when the central bank alters its baseline repo rates. Usually, banks prefer to increase or decrease your total remaining tenure months rather than changing your immediate monthly installment amount.

Four: Can I add my spouse as a co-applicant to lower our monthly installment?

Adding your earning spouse as a joint co-applicant does not automatically lower the interest rate, but it expands your total loan eligibility capacity. If your spouse is a woman, many top Indian lenders provide a special 0.05% interest rate concession, which lowers your EMI.

Five: Is insurance mandatory when taking a 10 lakh home loan for 20 years?

While loan insurance is not legally mandatory by central banking laws, most lenders highly recommend buying a basic term plan or home loan protection layout. This safeguard ensures that your family retains absolute ownership of the house if any unexpected tragedy occurs.

Six: Can I get tax benefits on a 10 lakh home loan under the old tax regime?

Yes, under the old tax regime, you can claim a deduction of up to 1.5 lakh per year on your principal repayment under Section 80C. You can also claim a deduction of up to 2 lakh per year on the interest component under Section 24b.