20 Lakh Home Loan Processing Fee Comparison: A Complete Bank Guide

Planning for a home loan involves looking at more than just the regular monthly installments. Many first-time home buyers forget to calculate the upfront administrative fees that banks charge before releasing the money.

When you apply for a 20 lakh housing loan, financial institutions levy a one-time administrative charge known as a processing fee. This fee covers the cost of checking your credit score, verifying your employment profile, and evaluating your property papers.

This guide provides an honest, clear 20 lakh home loan processing fee comparison across top lenders in India. Knowing these hidden costs beforehand ensures you choose the most budget-friendly bank.

Direct Answer Snippets for Quick Reference

Which bank charges the lowest processing fee for a 20 lakh home loan?

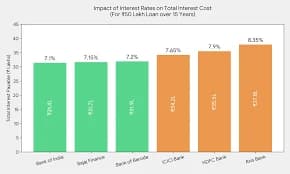

State Bank of India (SBI) generally charges the lowest processing fee, averaging 0.35% of the total loan amount, which equals roughly 7,000 plus taxes for a 20 lakh loan. SBI also completely waives this fee for government employees and defence personnel under special schemes.

Do private banks charge higher processing fees for a 20 lakh home loan?

Yes, private sector banks like ICICI Bank, HDFC Bank, and Axis Bank typically charge higher processing fees ranging from 0.50% to 2.00% of the loan amount. For a 20 lakh home loan, these private processing charges can vary between 10,000 and 15,000, depending on your professional profile.

Is the home loan processing fee refundable if my application gets rejected?

No, the home loan processing fee is entirely non-refundable across all Indian banks. Lenders collect this fee upfront to cover the immediate costs of structural legal verification and technical property valuation, regardless of whether your loan application gets approved or rejected.

What exactly is a Home Loan Processing Fee?

Before diving into the 20 lakh home loan processing fee comparison charts, it is essential to understand what this fee actually covers. Think of it as an administrative entry ticket for your loan.

Banks do not just take your word when you apply for a loan; they hire independent lawyers to check the property title and engineers to value the construction. The processing fee helps the bank pay these external professionals for their validation work.

Most banks split this charge into two separate parts. You pay a small login fee when you submit your documents, and the bank collects the remaining balance amount right before your final loan money is handed over.

Comprehensive 20 Lakh Home Loan Processing Fee Comparison Across Top Lenders

Different banks use different math rules to calculate their administrative fees. Some charge a flat fixed rate, while others charge a shifting percentage based on your total loan ticket size.

Let us look at a direct breakdown of what leading public and private banks charge for a standard 20 lakh home loan application.

Processing Fee Breakdown by Top Banks

Bank Name | Standard Processing Fee Scale | Approximate Cost for a 20 Lakh Loan | Special Conditions |

State Bank of India (SBI) | 0.35% of loan amount | 7,000 + GST | Full waivers available for defence and government staff |

HDFC Bank | Up to 0.50% of loan amount | 10,000 + GST | Minimum standard charge is capped at 3,300 |

ICICI Bank | Up to 1.00% to 2.00% of loan amount | 10,000 to 15,000 + GST | Charges vary based on salaried vs self-employed profiles |

Axis Bank | Up to 1.00% of loan amount | 10,000 + GST | Collects an initial upfront fee of 5,000 during application |

As you can see, choosing a public sector lender like SBI can save you thousands of rupees upfront compared to choosing premium private banking institutions.

Hidden Charges That Operate Alongside the Processing Fee

When studying a 20 lakh home loan processing fee comparison, you must remember that additional secondary small fees might appear during the loan approval journey.

These supplementary charges are usually billed separately from your standard processing fees:

Goods and Services Tax (GST)

All banking services in India attract a standard central tax rate of 18% GST. This tax is always added over and above the advertised processing fee, meaning an advertised fee of 10,000 will actually cost you 11,800 out of pocket.

Central Registry (CERSAI) Charges

The Indian government operates a central security registry to prevent property frauds and double-mortgages. For any home loan above 5 lakhs, banks legally collect a mandatory, small registry fee of 100 plus taxes.

Document Retrieval and Administrative Fees

Some private lenders levy separate small fees for digital credit bureau checks or physical document upkeep. Always ask your loan officer for a clear, written list of all extra charges before submitting your file.

How to Negotiate and Lower Your Loan Processing Costs

You do not always have to pay the standard listed price when dealing with home loan administrative costs. If you have an excellent financial profile, you can use certain strategies to secure a discount.

Here are the most effective ways to lower your upfront processing burden:

Maintain a Credit Score Above 750: Lenders love safe borrowers. Having an excellent credit record gives you strong leverage to request the branch manager for a partial or full fee waiver.

Apply During Major Festive Seasons: Banks run competitive loan campaigns during major festivals like Diwali or New Year. Applying during these promotional periods often helps you get a 100% waiver on processing charges.

Leverage Existing Payroll Relationships: Always check for home loan options with the specific bank that manages your regular corporate salary account. Banks regularly offer lower fees to existing, loyal customers.

Conclusion

Conducting a detailed 20 lakh home loan processing fee comparison is a vital step toward keeping your home-buying journey affordable. While private banks offer faster digital approvals, public banks like SBI remain highly cost-effective due to their lower percentage caps and specialized waiver schemes.

Never hesitate to ask transparent questions about hidden costs, non-refundable elements, and applicable GST layers before signing your application form. By staying informed and comparing your options wisely, you can protect your hard-earned savings right from day one.

Frequently Asked Questions (FAQs)

1. Why do banks collect the processing fee before approving the loan?

Banks collect the processing fee upfront because they incur immediate expenses to evaluate your profile. They must pay internal verification teams and external legal experts to check your property authenticity, regardless of whether your final loan application is approved or rejected.

2. Can the processing fee be adjusted or deducted from my final 20 lakh loan amount?

No, the processing fee cannot be adjusted against your disbursed loan principal. It is an independent administrative cost that you must pay out of pocket via a check or digital payment when you submit your official loan application documents.

3. Does a high CIBIL score automatically qualify me for a zero processing fee?

An excellent CIBIL score helps you secure the lowest available interest rates and fast-tracks your documentation checks. However, it does not automatically eliminate the processing fee unless the bank is running a specific zero-fee promotional campaign at that time.

4. Is the processing fee higher for self-employed individuals compared to salaried workers?

Yes, many private financial institutions charge a slightly higher processing percentage or minimum fee limit for self-employed business owners. This extra cost covers the deeper auditing required to verify business balance sheets, tax filings, and profit stability.

5. What happens to my paid processing fee if I decide to cancel my loan application?

Because the processing fee is strictly non-refundable, you will lose that money if you decide to cancel your application halfway through the process. The bank will not return the cash since they have already spent those resources on legal and technical checks.

6. Do housing finance companies (HFCs) charge more processing fees than traditional commercial banks?

Yes, housing finance companies generally charge slightly higher processing fees, sometimes ranging from 1.00% to 2.00% of the loan amount. They take on higher risk profiles and charge higher administrative fees to offset their operational structures.