5 Lakh Home Loan for First Time Buyer: A Beginner's Complete Guide

Stepping into the world of property ownership is a major and deeply rewarding life milestone. If you are taking this big step for the very first time, managing your initial credit choices smartly ensures a stress-free experience.

Choosing a highly manageable financing amount, like five lakh rupees, is the perfect way to build or purchase a house without overwhelming your household budget. A 5 lakh home loan for first time buyer plan is tailored to offer low interest rates, minimal paperwork, and powerful government support.

This honest, clear guide cuts out all confusing banking jargon to show you standard eligibility criteria, monthly EMI structures, special tax benefits, and step-by-step methods to get your application approved instantly.

Google Featured Snippet Answers

How do banks evaluate a 5 lakh home loan for first time buyer application? Banks evaluate a 5 lakh home loan for first time buyer application by analyzing three primary criteria: your age, your credit history, and your regular monthly income. Lenders look for a steady job history, a CIBIL score above 720, and a minimum net monthly paycheck starting around fifteen thousand rupees.

Can first-time buyers get government benefits on a 5 lakh housing loan? Yes, first-time buyers can claim massive government financial benefits through the Pradhan Mantri Awas Yojana interest subsidy program. Eligible lower-income households receive an upfront interest discount of up to 1.80 lakh rupees credited straight into their loan account, which directly slashes future monthly installments.

Home Loan, Housing Loan Finance Company in India+ 1

What is the monthly EMI for a 5 lakh first-time buyer loan over 10 years? Assuming a standard, competitive interest rate tier of 7.90% per annum, a five lakh loan carries highly affordable payment terms. Your predictable monthly installment bill over a ten-year repayment tenure will sit at approximately 6,043 rupees, making it safe for beginners.

Why a 5 Lakh Loan is Perfect for First-Time Homeowners

When purchasing your very first property, overextending your financial limits with a huge, multi-crore debt line can lead to severe long-term budget stress. Sticking to a smaller principal balance like five lakh rupees is an incredibly safe personal finance decision.

A small-tier credit portfolio allows you to enjoy quick repayment tenures, saving you massive amounts of money on long-term compound interest charges. It acts as an excellent funding choice to purchase open plots in growing sectors, finish rural home self-construction, or add floors to an existing ancestral structure.

Furthermore, because five lakh rupees is a safe, low-risk balance tier for lenders, major public and private banks process these applications with rapid speeds and offer their lowest benchmark interest rates.

Estimated Payment Structure by Tenure

To visualize your future monthly outlays before scheduling a consultation with a branch manager, review this clear breakdown calculated at a baseline interest rate of 7.90% per year:

Total Loan Amount | Annual Interest Rate | Repayment Tenure | Expected Monthly EMI | Total Interest Payable | Total Overall Repayment |

|---|---|---|---|---|---|

5 Lakhs | 7.90% | 5 Years | 10,117 Rupees | 1,07,014 Rupees | 6,07,014 Rupees |

5 Lakhs | 7.90% | 10 Years | 6,043 Rupees | 2,25,147 Rupees | 7,25,147 Rupees |

5 Lakhs | 7.90% | 15 Years | 4,750 Rupees | 3,54,984 Rupees | 8,54,984 Rupees |

5 Lakhs | 7.90% | 20 Years | 4,151 Rupees | 4,96,257 Rupees | 9,96,257 Rupees |

Core Eligibility Rules for First-Time Property Applicants

To successfully pass standard banking clearance logs for an affordable housing loan, your professional and financial profile must meet simple national lending benchmarks.

1. The "First-Time Buyer" Legal Definition

To qualify for exclusive beginner benefits, you must fulfill a strict property ownership rule. The applicant, their working spouse, and their minor dependent children must not own a permanent brick or pucca house anywhere in India.

Stashfin

2. Credit Score Repayment Report Cards

Your credit score is a three-digit rating monitored by central tracking bureaus like CIBIL that acts as your financial report card. Keeping your credit history above 720 proves you pay off credit cards and retail store invoices on time, unlocking fast approvals.

CIBIL Score Above 720 + First-Time Homeowner = Lowest Interest Rate Offers

3. Basic Age and Income Thresholds

Lenders accept loan submissions from resident Indian citizens who are at least twenty-one years old when applying. For a five lakh principal line, salaried individuals should show a minimum monthly take-home pay of fifteen thousand rupees, while self-employed shopkeepers should show two years of steady business income.

Incredible Government Subsidies and Tax Shshields

One of the biggest reasons to enter the housing market as a beginner is the access to special state-backed wealth shields that reduce your long-term cost burden.

Home Loan, Housing Loan Finance Company in India

The PMAY Urban 2.0 Interest Subsidy Reward

First-time buyers belonging to the Economically Weaker Section or Low Income Group can leverage the central Interest Subsidy Scheme. The government offers deep interest discounts on small-tier housing credits, providing an upfront credit of up to 1.80 lakh rupees straight into your bank account.

PMAY (U)+ 1

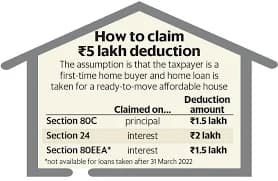

Annual Income Tax Deductions

If you file your income taxes using traditional, old-regime deductions, carrying a active housing loan acts as a powerful financial shield:

Section 24(b): Allows you to deduct up to two lakh rupees of your annual loan interest payments directly from your taxable income pool.

Section 80C: Lets you claim up to 1.50 lakh rupees for your annual principal repayments, which includes your initial property stamp duty and legal registration charges.

Stashfin

Step-by-Step Application Roadmap for Beginners

Do not feel intimidated by the thought of interacting with bank officers. Follow these clear, systematic steps to complete your loan application seamlessly.

Step 1: Polish Your Credit Profile and Gather Paperwork

Three months before applying, check your credit report to ensure it contains zero typing errors. Organize your basic Know Your Customer identity documents, such as your Aadhaar card and PAN card, inside a secure folder.

Step 2: Request an In-Principle Sanction Letter

Visit your preferred public sector bank or housing finance company and request an in-principle approval. This official letter states exactly how much money the bank is willing to lend you based on your income slips, allowing you to finalize property deals securely.

Step 3: Complete Technical Property Appraisals

Once you select your home site, the bank will send independent engineers and legal panels to inspect the property blueprints. If the land deeds are completely clear of boundary disputes, the lender will release the five lakh funds straight to the seller.

Conclusion

Securing a 5 lakh home loan for first time buyer package is an exceptionally safe, smart, and accessible strategy to kickstart your personal wealth-building journey. By keeping your principal small, mapping out a clear ten-year tenure, and utilizing government interest subsidies, you can move into your own home safely.

Take your time to monitor your credit rating early, double-check that your identity documents contain zero spelling errors, and shop around to compare multiple lenders online. With disciplined preparation, you can confidently build your permanent house while keeping your absolute financial freedom protected.

Frequently Asked Questions

Does a 5 lakh home loan for first time buyer program require female ownership? If you intend to claim special lower-income interest subsidies under central government programs like PMAY, registering the property with an adult female family member as a primary owner or joint co-owner is a mandatory requirement.

Home Loan, Housing Loan Finance Company in India

Can I get a home loan if I have just started my very first job? Banks typically look for at least one to two years of continuous work experience to confirm your income stability. If you are entirely fresh to the workforce, adding an senior earning family member as a co-applicant guarantees a smooth approval.

What hidden fees should a first-time buyer budget for outside of the loan? Lenders calculate your loan principal based solely on the core value of the building structure. You must arrange separate out-of-pocket cash to cover state stamp duties, asset registration fees, technical evaluation charges, and local legal search costs.

Stashfin

Is it smart to choose a floating interest rate or a fixed interest rate? Floating interest rates start out significantly lower than fixed rates and reduce automatically whenever national policy rates drop. They also allow you to make early part-payments to clear your debt ahead of schedule without facing any bank penalty fees.

Basic Home Loan

What happens if I miss a monthly loan payment due to a personal emergency? Missing an installment results in immediate late payment penalty charges and causes deep damage to your credit report. If you face a cash emergency, always speak directly with your branch manager to explore alternative payment timelines safely.

Can I use a first-time buyer loan variant to fund a home repair project? Yes, standard housing credit lines cover home construction, direct flat purchases, property expansions, and major structural renovations. You can utilize the five lakh funds to add a new room or convert a temporary roof into a permanent concrete setup.