5 Lakh Home Loan Monthly EMI Calculator: A Simple Beginner's Guide

Taking a step toward buying or improving your home is an incredible milestone. When borrowing a smaller amount, like five lakh rupees, planning ahead ensures your household budget remains smooth and stable.

The best tool to help you budget is a 5 lakh home loan monthly EMI calculator. This tool calculates your Equated Monthly Instalment, or EMI, so you know exactly what your monthly outlays will look like.

This guide removes all complex banking equations to show you how calculation math works, what your monthly costs look like over various timelines, and how to use this data to save money.

Google Featured Snippet Answers

How does a 5 lakh home loan monthly EMI calculator work?

A 5 lakh home loan monthly EMI calculator uses three distinct pieces of information to determine your cost: your total loan principal, your bank's annual interest rate, and your chosen loan tenure. It instantly processes these variables to show your predictable monthly bill, total interest cost, and absolute final repayment sum.

What is the monthly EMI for a 5 lakh loan at 8.5% interest?

Using a standard calculation rate of 8.5% interest per year, a five lakh loan features highly predictable paths. A five-year tenure requires roughly 10,258 rupees monthly. Shifting to a ten-year tenure reduces the bill to 6,199 rupees, while a fifteen-year tenure brings the payment down to 4,924 rupees.

Why should beginners use a home loan monthly calculator?

Beginners should use a calculator to visualize the long-term impact of their borrowing choice before speaking to a bank. Adjusting the input sliders allows you to find an optimal balance between an affordable monthly invoice and the lowest possible total interest paid over the life of the loan.

The Math Behind a 5 Lakh Home Loan Monthly EMI Calculator

While an online portal gives you instant answers, knowing how the mathematical mechanics function helps you understand your loan balance better.

An electronic monthly calculator runs on a standardized financial formula that looks at your principal loan amount, the monthly interest rate, and the total number of monthly installments.

In the initial years of your repayment timeline, your monthly payments are heavily weighted toward paying off the interest fees. As your remaining principal drops over the years, a larger percentage of your cash goes toward erasing the actual borrowed debt.

Amortization Breakdown by Tenure

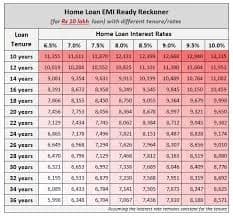

To see how a 5 lakh home loan monthly EMI calculator projects your finances, review this clear breakdown across standard tenures at a baseline interest rate of 8.40% per annum:

Principal Amount | Annual Interest Rate | Loan Tenure (Years) | Estimated Monthly EMI | Total Interest Payable | Total Overall Repayment |

5 Lakhs | 8.40% | 5 Years | 10,239 Rupees | 1,14,357 Rupees | 6,14,357 Rupees |

5 Lakhs | 8.40% | 10 Years | 6,174 Rupees | 2,40,891 Rupees | 7,40,891 Rupees |

5 Lakhs | 8.40% | 15 Years | 4,897 Rupees | 3,81,373 Rupees | 8,81,373 Rupees |

5 Lakhs | 8.40% | 20 Years | 4,308 Rupees | 5,33,830 Rupees | 10,33,830 Rupees |

Why You Should Never Skip Using an EMI Calculator

Using a digital calculator is not just an optional research step; it is your ultimate financial shield against taking on an expensive or unmanageable debt load.

1. It Protects Your Monthly Household Budget

An online calculator shows your true future costs in plain sight. If your household's net income is thirty thousand rupees a month, seeing a monthly bill of ten thousand rupees warns you that a short five-year tenure might put a strain on your daily living costs.

2. It Reveals the Real Cost of Borrowing

Many buyers only focus on keeping their monthly payments as low as possible. However, inputting longer timelines into a 5 lakh home loan monthly EMI calculator reveals that a twenty-year loan causes your interest fees to exceed the actual five lakh principal you borrowed.

Longer Tenure Slider = Smaller Monthly Bill + Much Higher Interest Accumulation

3. It Allows for Instant Bank Offer Comparisons

If Bank A offers you an 8.5% rate with a 2,000 rupee processing fee, and Bank B offers an 8.75% rate with zero processing charges, a calculator helps you make an accurate choice. You can calculate the precise difference over ten years to see which route genuinely saves you money.

How to Input Your Information Correctly for Accurate Results

To get highly reliable outputs from a digital calculator, you need to input realistic numbers rather than rough guesses.

Loan Principal Amount: Enter exactly five lakh rupees, or the remaining sum required after subtracting your personal down payment cash from the house purchase price.

Interest Rate Percentage: Avoid typing in old, historic interest rates. Look up current, live benchmark lending rates from major institutions like the State Bank of India to input a realistic baseline, such as 8.25% to 8.75%.

Tenure Duration: Input your target timeline in years or total months. A standard baseline for a smaller loan size is typically five to ten years.

Practical Ways to Optimize Your Monthly Calculator Outputs

Once you see your initial calculation results, you can use several smart personal finance habits to make the final layout much more affordable.

Improve Your CIBIL Score First

Lenders determine your actual interest rate tier based on your personal credit score. Boosting your CIBIL score above 750 before applying allows you to type a much lower interest percentage into your calculator, reducing every future monthly bill.

Add a Bit More to Your Down Payment

If the monthly calculator shows a payment that feels tight for your current salary, try to save a little extra cash before finalizing the paperwork. Lowering your required loan amount down to four lakh rupees drops your monthly bills instantly.

Schedule Early Principal Prepayments

You do not have to stick to the rigid schedule shown on a bank's amortization table. Making small, occasional part-payments directly toward your loan principal cuts down your remaining tenure drastically, saving you thousands in interest.

Conclusion

A 5 lakh home loan monthly EMI calculator is an indispensable tool that replaces guesswork with solid, verifiable numbers. Whether you choose a short five-year timeline to clear your debt quickly or a ten-year structure to preserve your monthly cash flow, the choice is entirely yours to control.

Take your time to test different combinations, maintain a clean credit file, and budget honestly for extra processing costs. By mastering your loan numbers before signing a contract, you can build your home with absolute confidence and security.

Frequently Asked Questions

Are online home loan monthly calculators completely accurate?

Online calculators provide highly precise mathematical calculations based on the exact numbers you input. However, your final bank bill might vary slightly because of hidden processing fees, local stamp duties, documentation charges, or changing floating interest rates.

Can I use this calculator to estimate costs for an existing loan?

Yes, you can input your current remaining principal balance and your existing interest rate to see what your future payments look like. This is highly useful if you are planning to switch banks via a balance transfer for a better rate.

Does changing the calculator tenure impact my home loan eligibility?

Yes, changing your tenure modifies your eligibility profile. Banks require that your monthly loan payment does not consume more than forty to fifty percent of your income. If a short tenure pushes the bill past that mark, extending the timeline helps you qualify.

How often do floating loan interest rates change inside a calculator?

Floating loan interest rates are tied to external benchmark rates managed by central banking authorities. While the calculator math stays uniform, you should update your interest rate inputs whenever central policy rates shift to keep your estimates accurate.

Is there a penalty fee if I pay more than the calculator's stated monthly EMI?

If your housing loan relies on a standard floating interest rate, banking guidelines protect you from early repayment penalties. You can pay extra cash into your loan account whenever you have it to clear your debt ahead of schedule.

Can students use an EMI calculator to plan a family house extension?

Yes, anyone can use a calculator to study financial scenarios. While a student will need a working parent or guardian as a co-signer to secure real approval, mapping out the numbers early helps the entire family plan their finances responsibly.

For a complete visual walkthrough on comparing rates from major lenders and managing your tenure choices effectively, you can watch this comprehensive guide on Understanding Housing Loans and EMI Calculation Hacks. This video breaks down real-world bank structures and interest differences to help you make the smartest financial decision.