5 Lakh Home Loan Repayment Tenure Maximum: A Complete Beginner's Guide

When you plan to build or buy your dream house, managing finances is the most important step. A small budget home loan can bridge the gap between your savings and the actual construction costs.

Understanding your repayment options helps you plan your monthly budget without stress. Choosing the right timeline ensures you do not burden your family with heavy financial liabilities.

Direct Answer Snippets for Quick Reference

What is the maximum tenure for a 5 lakh home loan?

The 5 lakh home loan repayment tenure maximum is generally up to 30 years for most banks and housing finance companies. However, this upper limit depends heavily on the borrower's age at the time of loan application and their retirement profile.

How does tenure affect your monthly EMI?

A longer tenure lowers your monthly EMI but increases the total interest you pay over time. Conversely, a shorter tenure increases your monthly EMI payment but helps you clear your debt faster, saving you a massive amount of interest money.

Who can get the maximum 30-year tenure?

Young salaried individuals aged between 21 and 35 years usually qualify for the maximum 30-year repayment window. Banks offer this because these borrowers have many active working years left before they reach the standard retirement age.

Understanding the 5 Lakh Home Loan Repayment Tenure Maximum

When you apply for a micro or mini housing loan, banks look at your repayment capacity. The maximum time a bank gives you to pay back the loan is known as the maximum tenure.

For a 5 lakh housing loan, most financial institutions offer a flexible timeline ranging from 1 year to 30 years. This 30-year limit is the absolute 5 lakh home loan repayment tenure maximum allowed by the banking regulatory framework.

While a 30-year window sounds highly attractive, it might not always be the best choice for every individual. The right tenure balance keeps your pockets happy while protecting your hard-earned savings from excessive interest rates.

Key Factors That Decide Your Maximum Loan Tenure

Banks do not blindly give a 30-year timeline to every single applicant who walks through their doors. They calculate risks using multiple personal and professional metrics.

1. Age of the Applicant

Your age is the primary deciding factor for your loan timeline. Banks want the entire loan cleared before you retire from your job.

If you apply at age 25, you can easily get the 5 lakh home loan repayment tenure maximum of 30 years. If you apply at age 45, your tenure will likely be restricted to 15 or 20 years.

2. Employment Type and Stability

Salaried employees working in government sectors or reputed corporate companies get preferential treatment. They have a predictable income graph.

Self-employed individuals or freelancers might face stricter terms. Banks might limit their tenure to 15 or 20 years due to the fluctuating nature of business earnings.

3. Property Age and Document Validity

The house or plot you are financing acts as collateral security for the bank. The structural life of the building matters.

If you are buying an old property, the bank will ensure the loan tenure does not outlive the remaining lifespan of the building. New constructions easily get longer timelines.

Monthly EMI Breakdown for a 5 Lakh Home Loan

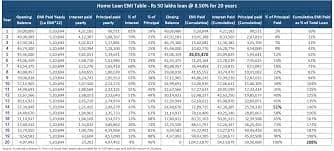

To make a smart decision, you must see how the numbers shift when you change your repayment years. Let us look at a realistic example assuming an average interest rate of 9% per annum.

Short Tenure Option: 10 Years

Choosing a 10-year period means you want to get rid of your debt quickly. Your monthly EMI will be higher, sitting around 6,334.

The benefit here is the total interest paid over 10 years is roughly 2.60 lakh. Your total repayment to the bank stands around 7.60 lakh.

Medium Tenure Option: 20 Years

This option acts as a middle ground for middle-class households. Your monthly EMI drops down significantly to approximately 4,499.

However, because the clock ticks for an extra ten years, the total interest climbs up to 5.80 lakh. You pay back a total of 10.80 lakh.

Maximum Tenure Option: 30 Years

If you stretch your timeline to the 5 lakh home loan repayment tenure maximum of 30 years, your EMI becomes incredibly cheap at around 4,023 per month.

The catch is the shocking interest accumulation. Over 30 years, you pay around 9.48 lakh just in interest, making your total repayment 14.48 lakh.

Pros and Cons of Opting for the Maximum Repayment Tenure

Stretching your loan to the maximum limit is a double-edged sword. Let us look at both sides honestly so you can weigh your choices.

The Advantages

Highly Affordable EMIs: Your monthly commitment is low, leaving you with enough cash for daily household expenses.

Higher Loan Eligibility: Low EMIs mean your fixed obligations are low, allowing banks to approve your loan easily.

Stress-Free Emergency Management: If you face a medical crisis or job loss, managing a small monthly EMI is less stressful.

The Disadvantages

Massive Interest Outflow: As shown in the breakdown, you end up paying almost double the loan amount just in interest.

Long-Term Financial Liability: You carry the mental burden of a debt into your senior years or retirement phase.

Slower Equity Growth: Your initial payments go mostly toward clearing the interest rather than reducing the actual principal amount.

Smart Strategies to Reduce Your Repayment Burden

You do not have to remain trapped in a 30-year loop just because your loan book says so. You can use smart banking rules to break free early.

Make Regular Part-Payments

Whenever you receive a yearly bonus, a festival gift, or extra business profits, use that money to make a principal part-payment.

Even paying one extra EMI amount every year can reduce your total tenure by several years and save thousands in interest.

Opt for an EMI Step-Up Plan

As your career grows, your salary naturally increases over time. You can ask your bank to increase your EMI amount by 5% or 10% every year.

This gradual increase matches your financial growth and aggressively cuts down your total outstanding years without hurting your lifestyle.

Refinance to a Lower Interest Rate

Keep an eye on the financial market trends. If another bank offers a significantly lower interest rate, consider transferring your balance.

A lower interest rate can help you reduce either your monthly EMI load or your total remaining tenure.

Step-by-Step Process to Apply for a 5 Lakh Home Loan

Securing a small home loan requires systematic planning and proper documentation to ensure quick approval.

Step 1: Check Your Credit Score

Before visiting any bank, check your credit report. A credit score above 750 helps you secure the best interest rates and flexible tenures.

Step 2: Gather Essential Documents

Keep your identity proof, address proof, past six months' bank statements, and income tax returns ready for verification.

Step 3: Compare Bank Offers

Do not settle for the first bank you visit. Compare interest rates, processing fees, and tenure limits across at least three different lenders.

Conclusion: Making the Right Choice for Your Future

The 5 lakh home loan repayment tenure maximum gives you a safety net of up to 30 years to clear your dues comfortably. It keeps your monthly installments low and protects your family from unexpected financial crunches. However, this comfort comes at the cost of high interest payments over the decades.

The smartest approach is to select a comfortable medium tenure or opt for the maximum tenure but make regular part-payments whenever possible. Plan your home budget wisely, read the loan documents carefully, and build your dream home with total peace of mind.

Frequently Asked Questions (FAQs)

One: Can a senior citizen get a 30-year maximum tenure for a 5 lakh home loan?

No, senior citizens cannot get a 30-year tenure. Banks require the entire loan amount to be fully paid back by the time the borrower reaches 60 to 65 years of age. Therefore, an older applicant will get a much shorter, restricted repayment window.

Two: Does a short tenure reduce the processing fee of a 5 lakh home loan?

No, the processing fee does not depend on your loan timeline. It is usually a fixed percentage of the total loan amount, which is 5 lakh in this case, or a flat standard fee charged by the bank during application.

Three: Is it possible to change the repayment tenure after the loan is approved?

Yes, you can request your bank to modify your tenure later. If you want to reduce it, you can increase your monthly EMI. If you want to increase it up to the maximum limit, the bank will reassess your age and current income status.

Four: Are there any penalties for paying off a 5 lakh home loan early?

According to regulatory guidelines, banks cannot charge prepayment penalties on floating interest rate home loans. If you have a fixed-rate loan, minor charges might apply depending on the terms and conditions of your specific bank.

Five: Can I get a 5 lakh home loan for house renovation with a 30-year tenure?

Home renovation loans are often treated slightly differently than fresh home construction loans. While some banks extend the timeline up to 15 or 20 years for renovations, getting the absolute 30-year maximum limit is rare for minor repair works.

Six: How does a pre-EMI system work if I choose the maximum tenure?

If you buy an under-construction property, you pay only the interest on the disbursed loan amount, which is called pre-EMI. The actual maximum repayment tenure clock starts ticking only after the physical construction is complete and you take full possession of the house.