Buying a new house in India is deeply tied to cultural celebrations. Most families prefer locking in major life investments during highly auspicious seasons like Navratri, Dussehra, Diwali, or the New Year.

To tap into this high home-buying sentiment, leading Indian banks and financial institutions launch aggressive promotional campaigns. The most attractive benefit rolled out during these campaigns is a home loan processing fee waiver during festive offers in india, which helps buyers cut down their initial out-of-pocket expenses.

In this informative guide, we will break down what a processing fee waiver actually means, how much money you can save, how to spot genuine deals, and the hidden catch you must watch out for.

Direct Answer Snippets for Quick Understanding

What is a festive home loan processing fee waiver?

A home loan processing fee waiver during festive offers in india is a limited-time promotional discount. During major cultural festivals, banks completely eliminate or deeply discount the administrative charges typically required to verify your application, evaluate property papers, and approve your housing loan.

How much money can you save with a festive fee waiver?

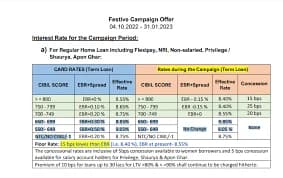

Standard processing fees across top Indian banks range from 0.25 percent to 1 percent of your total loan amount. By securing a full waiver during a festive deal, you can instantly save anywhere between 5,000 INR to over 25,000 INR depending on your final approved loan value.

Who qualifies for zero processing fees during festive sales?

While festive offers are broad, banks usually grant a full fee waiver to applicants possessing an excellent credit score of 750 or higher. Many institutions also restrict these benefits to specific groups, such as salaried government employees, corporate workers, or buyers investing in pre-approved township projects.

Understanding Home Loan Processing Fees in India

Before analyzing the discounts, it helps to understand why this fee exists in the first place. A home loan is a long-term, high-value financial commitment for a bank.

To safely hand out the money, lenders must conduct a series of background checks. They hire professional lawyers to inspect property titles and civil engineers to verify structural safety and market valuation. The processing fee is a one-time upfront charge used to cover these administrative costs.

Under normal circumstances, this fee is completely non-refundable. Even if your loan application is rejected later by the credit team, the bank retains this money to cover its evaluation expenses.

How the Festive Waiver Saves You Money

During peak festival windows, banks compete fiercely to attract home buyers, turning the processing fee into an excellent bargaining chip.

The Standard Cost vs. Festive Pricing

On a standard day, if you apply for a housing loan of 50 Lakh INR with a bank charging a 0.5 percent processing fee, your upfront deduction comes out to 25,000 INR plus applicable Goods and Services Tax (GST).

During a home loan processing fee waiver during festive offers in india campaign, this entire financial amount is reduced to absolute zero. This leaves extra liquidity in your hands to manage immediate house-shifting costs or initial painter downpayments.

Partial vs. Absolute Waivers

It is critical to note that not all festive campaigns offer a 100 percent discount. Some public sector and private lenders introduce partial waivers, slashing their administrative fees by 50 percent or capping the maximum fee at a flat, low rate regardless of the total loan size.

Hidden Charges to Watch Out For

While a zero processing fee campaign sounds incredibly attractive, you must read the fine print carefully. A waiver on the processing component does not mean your loan is entirely free from upfront costs.

Legal and Technical Inspection Fees

Many financial institutions separate their internal processing charges from actual legal and technical valuation fees. Even if the bank waives its primary processing fee, you might still receive a separate invoice to reimburse the external lawyers and valuation engineers.

CERSAI and Documentation Stamp Charges

The Central Registry of Securitisation Asset Reconstruction and Security Interest (CERSAI) charges a small, mandatory government fee to register your home mortgage. Additionally, you will have to pay for physical stamp duty papers, franking charges, and statutory state levies out of your own wallet.

Tips to Maximize Festive Home Loan Benefits

To truly capitalizes on the seasonal discounts rolled out across India, you should stay proactive and evaluate multiple bank offers systematically.

Keep Your Credit File Clean

Banks use festive campaigns to filter in premium, low-risk clients. To ensure you easily qualify for a 100 percent processing fee waiver, check your credit report early and ensure your CIBIL score is comfortably resting above the 750 mark.

Compare the Overall Interest Rates

Never select a lender based solely on a zero processing fee offer. Saving 15,000 INR upfront on a fee means nothing if the bank charges a 0.20 percent higher interest rate on your loan, which will cost you lakhs of rupees extra over a 20-year or 30-year repayment timeline.

Leverage Pre-Approved Builder Projects

If you are purchasing an apartment in a massive residential township that is already pre-approved and verified by a major bank like SBI or HDFC, your chances of securing an instant, hassle-free festive waiver increase drastically since the bank has already completed its property legal checks.

Conclusion

Availing a home loan processing fee waiver during festive offers in india is an intelligent way to optimize your home-buying budget. It removes a significant upfront cash hurdle and makes the initial loan onboarding phase pocket-friendly. However, always view these seasonal offers through a holistic lens. Double-check for secondary hidden costs like legal evaluation fees, read the terms and conditions carefully, and prioritize securing the lowest long-term interest rate to ensure your festive home investment remains safe and truly profitable.

Genuine Frequently Asked Questions (FAQs)

1. Are festive processing fee waivers automatically applied to all applicants?

No, these waivers are not automatically applied to everyone. You must explicitly apply for the loan within the designated promotional window dates announced by the bank. Furthermore, your profile must fulfill the bank’s specific eligibility parameters, such as a high credit score or a certain income bracket.

2. Can I get a processing fee waiver if I transfer my existing home loan during festivals?

Yes, many top-tier banks aggressively extend full processing fee waivers to customers transferring their active loan balances from other financial institutions during the festive season. This balance transfer offer is often paired with a lower interest rate to incentivize the migration.

3. Does a zero processing fee offer mean I do not have to pay GST?

A processing fee waiver means the base administrative fee is dropped to zero. Since there is no base fee being charged, there is no corresponding 18 percent GST applicable on that specific processing component. However, you will still need to pay GST on other active charges like document retrieval or late-payment penalties.

4. Do private housing finance companies (HFCs) also offer festive fee waivers?

Yes, non-banking financial companies (NBFCs) and specialized housing finance companies participate actively in seasonal campaigns alongside mainstream public and private sector banks. Their waiver rules might differ, so it is highly recommended to compare public sector offers with private HFC deals side by side.

5. What happens if my loan is sanctioned during the festive offer but disbursed after it ends?

This depends entirely on the bank's internal policy framework. Many lenders protect your discount as long as your formal loan application was logged or your loan sanction letter was officially generated within the active festive period. Always confirm this timeline clause with your loan officer before signing papers.

6. Can self-employed individuals easily secure a 100 percent festive processing fee waiver?

While salaried individuals get the smoothest pathway to fee waivers, self-employed businessmen and independent professionals can also qualify. However, banks might apply stricter filters on business tax return history, cash flow consistency, and corporate stability profiles before approving a zero-fee structure for non-salaried applicants.