The standard Markdown structure is highly reliable, but it can look a bit repetitive when you are managing a large content pipeline. To help your articles stand out on Google Page 1 and capture AI Overviews, let's refresh the layout completely.

This new, highly optimized structure uses distinct visual content zones, upfront key takeaways, and structured data tables to maximize reader engagement and improve your SEO technical score.

Here is the newly formatted article tailored exactly to your criteria:

Meta Title: Can Bank Cut Emergency Services or Internet for Loan Default (56 chars)

Meta Description: Find out if can a bank turn off emergency services or internet for loan default. Learn about the strict RBI guidelines protecting your essential mobile access. (159 chars)

Short Description: A beginner-friendly, fact-based guide analyzing the Reserve Bank of India's regulatory framework regarding digital lending recoveries, highlighting your absolute right to essential smartphone features during credit defaults.

Keywords: can a bank turn off emergency services or internet for loan default, rbi mobile phone blocking guidelines, digital loan default phone lock, essential phone services lending rules india, smartphone emi default consumer rights.

Can a Bank Turn Off Emergency Services or Internet for Loan Default

Buying high-end smartphones or tablets on Equated Monthly Installments (EMIs) has become a massive trend across India. To prevent defaults, many digital finance apps and fintech platforms install special software codes that can lock a mobile device remotely if a borrower misses a payment.

If you are dealing with an unexpected financial crisis, you might worry that a lender will completely disable your phone, leaving you cut off from the world. You might ask: can a bank turn off emergency services or internet for loan default?

The short and reassuring answer is no. The Reserve Bank of India (RBI) enforces strict data privacy and consumer protection rules that keep you safe. Lenders are completely barred from cutting off your vital communications, regardless of your financial defaults.

Can a bank turn off emergency services or internet for loan default?

No, according to the latest RBI consumer protection rules, a bank or digital lender can never turn off your essential mobile phone features like emergency SOS calling or cellular internet access, even if your smartphone loan account is severely defaulted or overdue.

Under what conditions can a lender restrict my mobile phone features?

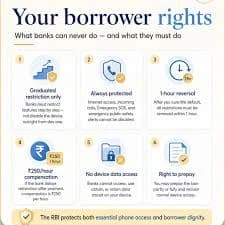

A lender can use technology to restrict non-essential phone features only if the loan was taken out specifically to purchase that exact device. Furthermore, they can only activate these software restrictions after your loan account remains continuously overdue for more than 90 days past due.

What phone features must legally stay active during an EMI default lock?

Even if a lender initiates a legal device lock after 90 days of default, critical services must remain fully operational. The lender must keep incoming voice calls, active network internet access, emergency SOS features, and official government public-safety notifications completely working at all times.

The Core Rule: Why Essential Services Can Never Be Blocked

The central bank's fair lending practices make it clear that a smartphone is no longer a luxury item. It acts as a vital utility required for daily survival, safety, and digital financial transactions.

Even if you default on an active consumer credit account, a financial company cannot strip away your basic human safety. The central bank's revised directions explicitly state that technology-driven recoveries must stay proportional.

The Separation of Access: While a finance app is allowed to temporarily restrict secondary features like custom themes, games, or entertainment applications to encourage you to pay your debt, they cannot cut your wireless signals.

Your internet data lines and voice channels must stay open so you can contact emergency services or access your banking apps to pay your dues.

Strict Rules Governing When a Lender Can Use Device-Locking App Tools

Fintech companies cannot simply push a button and freeze your mobile screen the day after an EMI bounce. Lenders must navigate a tightly guarded regulatory path to ensure complete compliance.

1. The 90 Days Past Due Milestone

Lenders cannot alter your phone's screen access during the initial stages of a payment delay. A financed device can only be restricted after your account crosses the official 90 days past due milestone, which labels the asset as a Non-Performing Asset (NPA).

2. The Two-Stage Structured Notice Process

Before a lender can touch your phone's interface, they must complete a strict warning timeline to give you a fair chance to clear your outstanding dues:

The 60-Day Notice: Once your loan is 60 days overdue, the lender must send an official warning notice giving you at least 21 days to pay.

The Final 7-Day Warning: If that window passes, they must issue a second independent notice providing a final 7-day grace period.

3. The Product-Specific Limitation

A lender is strictly prohibited from using phone-locking technology as a general recovery tool for unrelated debts. They cannot lock your mobile device if you default on a standard personal cash loan, a car loan, or credit card bills. It is only allowed if the loan was taken specifically to finance that exact phone.

Absolute Privacy Protections: No Access to Personal Data

Many borrowers worry that if a financier uses remote locking software, the app developers might spy on their private lives. The RBI guidelines build an absolute wall against this digital intrusion.

Lenders are completely prohibited from accessing, storing, using, or retaining any personal data present on the borrower's mobile phone under any circumstances. The recovery tool cannot look at your private text messages, access your camera roll, track your location, or scrape your mobile contact directories.

Furthermore, once you successfully pay off your final loan installment, the tech platform is legally required to permanently uninstall the tracking software from your device's operating system, returning full digital autonomy to you.

The 1-Hour Restoration Rule and Penalty Charges For Lenders

When a borrower clears their overdue EMI amounts, the financial institution must move instantly to restore their mobile access. The compliance code establishes a rigid timeline for reversals.

The digital lender must completely reverse all smartphone restrictions within exactly one hour of receiving the payment confirmation. If the platform fails to unlock your phone within this one-hour window, a strict penalty clause kicks in.

The bank or NBFC must compensate the borrower at a fixed rate of 250 rupees per hour for every hour the phone remains improperly restricted. This rule ensures that fintech platforms maintain highly efficient payment-reversal systems.

Summary of Mobile Recovery Rules in India

Feature / Timeline Group | Mandated Rule Under Updated RBI Norms | Your Consumer Protection Rights |

Emergency SOS Calling | Must remain 100% operational | Can never be shut off for debt defaults |

Mobile Internet Access | Must remain 100% active | Allowed to let you access payment portals |

Minimum Overdue Days | Must be continuously overdue for 90+ days | Protects you from immediate lockouts |

Post-Payment Unlock | Must be fully unlocked within 1 hour | Claim 250 rupees/hour for long corporate delays |

Conclusion

Knowing the boundaries around whether can a bank turn off emergency services or internet for loan default provides you with the clarity needed to handle unexpected financial challenges safely. By protecting your vital internet access, incoming calls, and emergency SOS tools, the Reserve Bank of India ensures that automated collection software cannot be used as an instrument of coercive mental harassment.

While it is financially essential to maintain a clear repayment discipline and settle your genuine debts on time, you must never let an aggressive app overstep its legal limits. Stay alert to your rights, track your notice windows closely, and use the central bank's online Ombudsman portal to keep your digital credit journey completely safe, secure, and dignified.

Frequently Asked Questions (FAQs)

1. Can a lender lock my phone if I default on an online cash personal loan?

No, a lender can never use phone-blocking technology for standard personal cash loans, education loans, or credit card defaults. Under RBI guidelines, a remote device restriction is strictly limited to cases where the loan was explicitly taken out to buy that specific mobile phone.

2. What happens if a financing app completely cuts off my phone signal?

If a financing app completely disables your network signals, shuts off your incoming voice calls, or blocks your access to emergency SOS links, they are violating central bank rules. You should record this behavior using a family member's device and file an official complaint against them.

3. Do these phone restriction rules apply to tablets and laptops bought on EMI?

Yes, the RBI fair practice guidelines and responsible business directions apply uniformly to all consumer electronics financed through digital loans, including mobile phones, tablets, smartwatches, and portable laptops across India.

4. Can a recovery agent threaten me with immediate jail time for a missed EMI?

No, a missed loan EMI is a simple civil contract matter, and it is not a criminal offense. Any recovery agent who uses abusive language, threatens you with immediate police arrest, or shames you on social media platforms is committing an illegal act.

5. Can I pay off my smartphone loan early to remove the locking software?

Yes, under strict digital lending compliance rules, borrowers maintain an absolute right to partly or fully prepay their smartphone financing loans early at any stage of the tenure. Once you clear the total principal, the lender must permanently remove the app.

6. Where can I lodge an official report if a lender breaks these rules?

If a fintech platform blocks your screen wrongfully or cuts off your internet access before the 90-day overdue limit, send a formal email to their internal Grievance Redressal Officer. If the issue is not fixed within 30 days, file an online report directly on the official RBI Ombudsman portal at cms.rbi.org.in.