Closing a personal loan ahead of schedule is a fantastic way to achieve financial freedom. Whether you received a workplace bonus, a family inheritance, or accumulated extra household savings, clearing your debt early lifts a major monthly money burden from your shoulders.

However, when you walk into a bank to pay off your balance, you might be surprised to hear about "foreclosure charges" or "prepayment penalties." Lenders historically charged these fees to make up for the interest income they lose when a borrower pays off a loan early. To protect consumers from unfair penalties, the Reserve Bank of India has established very strict, pro-borrower rules. Understanding the foreclosure charges for personal loan rbi guidelines latest updates will ensure you do not pay a single rupee in illegal or hidden fees.

In this comprehensive guide, we will break down how the current RBI rules protect individual borrowers, explain the difference between fixed and floating interest rates, and show you how to close your loan cleanly.

Direct Answer Snippets for Quick Understanding

What are the latest RBI guidelines on personal loan foreclosure charges?

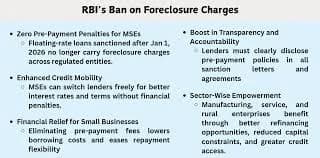

Under the current foreclosure charges for personal loan rbi guidelines latest framework, banks and Non-Banking Financial Companies (NBFCs) are strictly banned from charging foreclosure or prepayment penalties on all floating-rate personal loans extended to individual borrowers for non-business purposes. Lenders must permit complete early repayment for absolute zero extra cost.

Can banks charge foreclosure fees on fixed-rate personal loans?

Yes, the RBI permits lenders to levy foreclosure charges on fixed-rate personal loans. However, these penalties cannot be hidden or arbitrary. Lenders must clearly disclose the exact percentage rate and the exact mathematical calculation method upfront inside your primary loan agreement and Key Fact Statement (KFS).

Is there a mandatory lock-in period for loan foreclosure under RBI rules?

The RBI does not mandate a minimum lock-in period for closing a loan. However, for fixed-rate personal loans, individual banks are allowed to design their own internal board-approved lock-in policies (typically six to twelve months). For eligible floating-rate individual loans, lenders cannot use lock-in clauses to deny you a zero-fee foreclosure.

The Core Reset: Floating Rate Loans Are 100% Penalty-Free

To protect individual consumers and encourage healthy competition in the banking sector, the RBI implemented a major regulatory directive. Lenders are completely barred from penalizing individual borrowers who wish to clear their floating-rate debt early.

A floating interest rate means your loan's interest percentage shifts up or down over time based on external market benchmarks set by the central bank. The RBI emphasizes that because lenders already hold the right to revise interest rates periodically based on market conditions, adding an early closure penalty creates an unfair financial double-burden on the common citizen.

This zero-fee rule applies universally across all regulated financial entities in India. Whether your loan is held with a massive public sector unit like the State Bank of India, a private giant like HDFC Bank, or a digital lending NBFC, they must apply a flat zero percent foreclosure fee if your loan operates on a floating rate scale.

The Structural Reality for Fixed Interest Rate Loans

If your personal loan operates on a fixed interest rate structure, your monthly installment remains completely identical from the first day to the final month of your tenure. For this specific category, the regulatory environment is slightly different.

The RBI allows individual banks and NBFCs to formulate their own board-approved credit policies regarding fixed-rate closures. Lenders typically charge a foreclosure fee ranging from two percent to six percent of your remaining outstanding principal balance.

However, the RBI enforces a strict transparency rule to prevent consumer exploitation. Lenders are legally prohibited from introducing retrospective or surprise charges at the time of your foreclosure. Every single applicable fee must be explicitly printed in bold font inside your Key Fact Statement (KFS) at the time of your initial loan onboarding.

The Hybrid and Dual-Rate Loan Protection Rule

Many modern financial institutions market unique hybrid loan products. These special contracts operate on a fixed interest rate for the initial one to two years and then automatically transition into a standard floating rate framework for the remaining tenure.

The foreclosure charges for personal loan rbi guidelines latest directive provides clear instructions for these hybrid setups. The applicability of foreclosure penalties depends entirely on the active interest phase at the exact moment you execute your prepayment.

If you initiate a complete loan foreclosure while the hybrid loan is traveling through its initial fixed-rate phase, the bank can legally apply their standard disclosed penalty fee. However, the moment your loan clock enters the floating-rate phase, the zero-penalty protection activates instantly, making your closure entirely free.

Step-by-Step Action Plan to Foreclose Your Loan Cleanly

Closing your retail credit account requires executing a systematic, well-documented approach at your bank branch.

Step 1: Request an Official Foreclosure Statement

Do not guess your outstanding balance based on your mobile app dashboard. Contact your lender's customer desk and request a formal, typed Foreclosure Statement. This document calculates your precise principal debt and interest down to the exact daily reducing balance scale for that specific date.

Step 2: Arrange Funds and Execute Payment

Clear the exact final amount printed on your statement using verified electronic banking channels, such as a NetBanking pool, a real-time RTGS transfer, or an official bank check. Always save your digital transaction receipt or collect a stamped physical counter-slip from the branch teller.

Step 3: Secure Your No Objection Certificate (NOC)

Once your payment is verified inside the server, the lender must close your account profile. Ensure you demand an official No Objection Certificate (NOC) or No Dues Certificate (NDC). This vital document serves as your ultimate legal proof that your contract is permanently terminated and all liabilities are at zero.

Conclusion

Navigating the foreclosure charges for personal loan rbi guidelines latest landscape highlights that the central bank has built an exceptionally transparent, safe, and consumer-friendly ecosystem for Indian borrowers. If you hold a floating-rate personal loan, you possess the absolute legal freedom to pay off your debt early without facing a single paisa in penalties. If your loan is on a fixed-rate scale, your liability is safely limited to the upfront terms printed inside your Key Fact Statement. Keep your financial paperwork organized, verify that your bank updates your status to "Closed" on your CIBIL report within forty-five days, and utilize your surplus cash strategically to build a healthy, debt-free future.

Genuine Frequently Asked Questions (FAQs)

1. What is the difference between part-prepayment and full foreclosure under RBI rules?

Part-prepayment occurs when you pay a lump-sum amount (such as fifty thousand INR) to lower your core principal balance, but you continue your regular monthly EMIs with a shorter tenure or lower installment size. Full foreclosure means you pay off the entire remaining loan amount in a single shot, which permanently deactivates your credit account.

2. Can a bank charge me a foreclosure penalty if they are the ones who initiate the loan closure?

No, according to explicit RBI directions, lenders are strictly prohibited from imposing any prepayment or foreclosure charges if the loan closure is triggered at the instance of the bank itself. This includes scenarios where the bank executes account restructuring or chooses not to renew a running credit facility.

3. Does the zero-foreclosure charge rule apply to personal loans taken for business purposes?

The standard zero-charge rule covers all floating-rate personal loans taken by individuals for non-business use. For business-use loans, the RBI extended the zero-penalty waiver to individual borrowers and Micro & Small Enterprises (MSEs) for floating-rate options, provided the aggregate corporate credit limit stays within specified board caps.

4. What should I do if a lender illegally demands a foreclosure fee on my floating-rate loan?

If a local bank manager or digital lender ignores the latest guidelines and demands a foreclosure fee on a floating-rate loan, do not pay it. File a formal written complaint with the bank’s internal grievance redressal desk. If they fail to provide a satisfactory resolution within thirty days, escalate the file straight to the RBI Banking Ombudsman online.

5. Are goods and services tax (GST) applicable on personal loan foreclosure charges?

Yes, if your personal loan is a fixed-rate asset that attracts a legal foreclosure charge (e.g., three percent of your outstanding balance), that specific penalty fee is classified as a financial service. Consequently, the government applies a standard eighteen percent GST rate strictly on top of the calculated penalty fee amount.

6. Will foreclosing my personal loan early cause a drop in my CIBIL credit score?

No, successfully closing an active personal loan ahead of schedule will not damage your credit history. Paying off your debt in full proves to credit bureaus that you are a highly disciplined and reliable borrower. It lowers your overall debt-to-income ratio, which ultimately helps improve your credit profile for your long-term financial life.