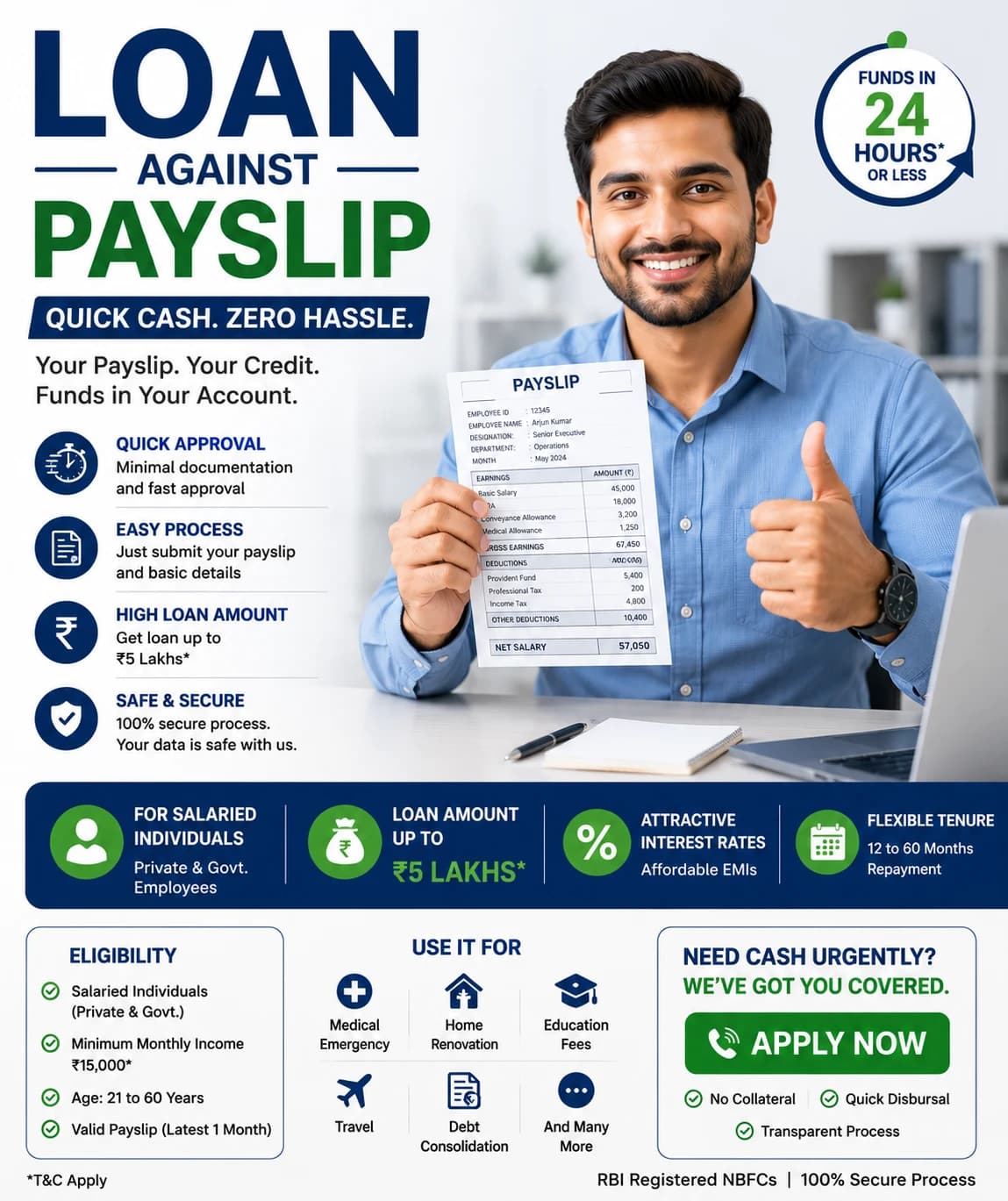

What is a loan against a payslip?

A loan against a payslip is a type of personal loan specifically designed for salaried individuals. Lenders use your monthly salary slip as primary evidence of your repayment capacity. It allows employees to access quick funds for emergencies, medical bills, or major purchases based on their consistent monthly income.

How much can I borrow with my salary slip?

The amount you can borrow usually depends on your net take-home pay. Most banks and digital lenders offer between 10 to 20 times your monthly salary. However, lenders also look at your existing debts to ensure your total monthly repayments do not exceed 50% of your total income.

Is it possible to get a loan with only one payslip?

While some fintech apps may offer small, short-term "nano loans" with one payslip, traditional banks usually require at least three to six months of salary history. This helps lenders verify that your employment is stable and that you have a consistent track record of receiving a regular income.

Introduction

Managing finances can be challenging, especially when unexpected expenses arise before your next payday. If you are a salaried employee, your payslip is more than just a record of your earnings; it is a powerful financial tool.

A loan against a payslip is one of the most common ways for professionals to access credit. Because you have a steady income, lenders view you as a lower-risk borrower compared to those without fixed earnings.

This guide will explain how these loans work, what you need to apply, and how to ensure you get the best interest rates without falling into a debt trap.

H2: Understanding the Concept of a Salary Slip Loan

A salary slip loan is essentially a personal loan where your employment status is the main collateral. Since you are not pledging a house or a car, it is considered an "unsecured loan."

Lenders focus on your "disposable income." This is the money left over after you pay your rent, bills, and other existing EMI commitments. If your payslip shows a healthy balance, your chances of approval are high.

H3: Why the Payslip is Important

The payslip provides three critical pieces of information to the lender. First, it confirms your employer’s identity and your job stability. Second, it shows your gross and net salary.

Third, and most importantly, it shows "deductions." If your payslip already shows many loan deductions, a new lender might be hesitant to give you more credit.

H2: Eligibility Criteria for a Loan Against Payslip

Every bank has its own rules, but the general requirements remain the same across the industry. Being prepared with these facts will help you avoid rejection.

Age Limit: Most lenders require you to be between 21 and 60 years old.

Employment Type: You should be a permanent employee at a registered private or public company.

Minimum Salary: Lenders usually set a minimum income floor, often starting from 15,000 to 25,000 per month depending on your city.

Work Experience: You typically need at least 6 months with your current employer and 1 year of total work experience.

Credit Score: A score of 750 or above is ideal, though some apps cater to those with lower scores at higher interest rates.

H2: Required Documents for a Fast Application

To get a loan against payslip approved quickly, you should keep digital and physical copies of your documents ready. Missing paperwork is the number one cause of processing delays.

H3: Primary Documents

Identity Proof: Passport, Voter ID, or National ID card.

Address Proof: Utility bills, rent agreement, or bank statements.

Income Proof: Your salary slips for the last 3 to 6 months.

H3: Financial Documents

Bank Statements: Most lenders ask for the last 6 months of the bank account where your salary is credited.

Tax Returns: In some cases, Form 16 or Income Tax Returns (ITR) for the last two years are required for higher loan amounts.

H2: Benefits of Choosing a Salary-Based Loan

Why should you choose a loan against your payslip instead of other types of credit? There are several practical advantages for the average worker.

No Collateral Needed: You don’t have to risk your assets like jewelry or property to get the money.

Quick Processing: Since income verification is straightforward, many digital lenders can approve these loans within hours.

Flexible Use: Unlike a car loan or a home loan, you can use a personal salary loan for anything—from a wedding to a laptop.

Builds Credit Score: Paying off a salary loan on time is an excellent way to improve your credit history for larger future loans.

H2: How to Apply for a Loan Against Payslip

The application process has become much easier thanks to online banking and mobile apps. Here is a step-by-step guide to doing it right.

Step 1: Research and Compare

Do not take the first offer you see. Use comparison websites to check interest rates, processing fees, and "pre-payment" penalties. Even a 1% difference in interest can save you a lot over two years.

Step 2: Check Your Credit Score

Before applying, check your credit report. If there are errors, fix them first. Frequent loan rejections can actually lower your score further, so only apply when you are confident.

Step 3: Online Application

Fill out the form on the bank's website. You will need to upload your loan against payslip documents. Many modern lenders use "e-KYC" which uses your ID number to verify your details instantly.

Step 4: Verification and Approval

The bank will verify your employment. They might call your HR department or send a representative to your office. Once verified, the loan agreement is signed digitally, and the funds are sent to your account.

H2: Things to Watch Out For (The Honest Truth)

While getting a loan is easy, managing it requires discipline. We want you to be a smart borrower, not a stressed one.

Interest Rates can be High: Because there is no collateral, interest rates for salary loans are higher than home or gold loans. Always check the "Annual Percentage Rate" (APR) to see the true cost.

Hidden Fees: Look out for processing fees, documentation charges, and "insurance" that some lenders force you to buy. Read the fine print before signing.

Debt Traps: It is tempting to take a loan just because you are eligible. However, taking multiple small loans against your payslip can lead to a cycle where your entire salary goes toward EMIs.

H2: Tips for Getting the Best Interest Rates

To get a low-interest loan against payslip, follow these insider tips:

Apply at Your Salary Bank: The bank where your salary is credited already knows your history. They often offer "pre-approved" loans with lower rates.

Maintain a Good Credit Score: Avoid late payments on credit cards to keep your score high.

Avoid Multiple Applications: Applying to five banks at once makes you look "credit hungry" and risky.

Negotiate: If you have worked at a reputable company for many years, don't be afraid to ask the bank manager for a rate discount.

H2: Conclusion

A loan against payslip is a reliable financial safety net for salaried professionals. It offers a path to quick funds without the need for collateral. By keeping your documents ready, maintaining a clean credit history, and borrowing only what you truly need, you can use these loans to improve your life rather than complicate it.

Always remember to read the loan agreement carefully and ensure the monthly repayments fit comfortably within your budget. Being an informed borrower is the first step toward true financial freedom.

H2: Frequently Asked Questions (FAQs)

1. Can I get a loan if my salary is paid in cash?

Most formal lenders (banks and major NBFCs) require salary to be credited directly to a bank account. If you receive cash, you will need to provide alternative proof like a heavy tax return history or apply through smaller, local micro-finance institutions which may charge higher interest.

2. What is the minimum salary required for a payslip loan?

While it varies by location, most lenders in urban areas look for a minimum net monthly income of 20,000. In smaller towns, some lenders may accept a salary of 10,000 to 15,000.

3. Will taking a loan against my payslip affect my job?

No, taking a personal loan does not affect your employment status. However, lenders will verify your employment with your HR department. As long as you are a legitimate employee, this is a standard procedure and is kept confidential.

4. What happens if I lose my job while repaying the loan?

If you lose your job, you are still legally obligated to pay the EMIs. It is highly recommended to have an "emergency fund" to cover at least 3 months of loan payments. You should also contact your bank immediately to discuss a temporary "moratorium" or restructuring of the loan.

5. Can I pay off my salary loan earlier than the fixed tenure?

Yes, most lenders allow "foreclosure" or "pre-payment." However, some may charge a small penalty fee (usually 2% to 5% of the remaining balance). Always check the pre-payment policy before signing the contract.

6. Does my company need to be on a "listed" category for me to get a loan?

Many large banks have a list of "Category A" or "Category B" companies. If your employer is a well-known MNC or a large government body, you will likely get lower interest rates and faster approval compared to working for a very small, unknown startup.