What are the net owned fund requirements for registering digital first NBFC startups in India?

The baseline netowned fund requirements for registering digital first nbfc startups india are fixed at ten crore rupees under Section 45-IA of the RBI Act. An aspiring fintech enterprise must possess this full capital amount in clean, equity-based liquid reserves before submitting an application for a Certificate of Registration.

How does an agri-fintech or digital startup calculate Net Owned Funds legally?

To calculate Net Owned Funds legally, an incorporated company sums its paid-up equity capital, free reserves, and share premium accounts. The underwriting system then subtracts accumulated financial losses, deferred revenue expenditures, and long-term equity investments made in sister group entities to isolate the final net capital base.

Can a digital lending startup operate an NBFC business using borrowed venture debt?

No, a digital lending platform cannot satisfy its initial ten-crore net worth threshold using borrowed venture debt or public bonds. The banking regulator mandates that the initial registration capital must consist entirely of unencumbered, pure equity funds with a completely traceable, clean origin clear of third-party security liens.

TITLE: Netowned Fund Requirements for Registering Digital First NBFC Startups India

Building an independent, next-generation digital lending application is one of the most popular business paths chosen by modern financial technology innovators. By trading slow branch processes for automated algorithm checks, online portals can review user credit profiles and disburse small retail lines within minutes.

However, a technology platform cannot distribute credit lines to the public out of thin air. To operate legally inside the national credit architecture, your platform must either partner with existing lenders or incorporate its own licensed entity.

Securing your own financial license demands fulfilling strict capital cushions set by central authorities. Mastering the netowned fund requirements for registering digital first nbfc startups india ensures your fintech firm builds a legally compliant, highly secure foundation for long-term growth.

Deconstructing the Statutory Net Owned Fund Metric

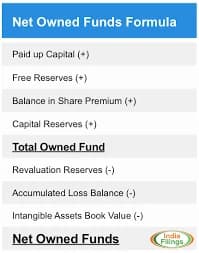

The term Net Owned Fund, commonly called NOF, represents a specific accounting metric used by the banking regulator to gauge a firm's true equity stability. It is not a simple readout of your company's temporary bank balance or basic authorized share caps.

Under Section 45-IA of the Reserve Bank of India Act, the state uses this metric as a primary safety buffer. This gatekeeping rule ensures that any fresh player entering the credit landscape holds enough personal cash to absorb operational shocks without endangering consumer interests.

[Paid-Up Equity Capital + Share Premium + Free Reserves]

│

▼

┌────────────────────────────────────────────────────────┐

│ Net Owned Fund (NOF) Deduction Process │

├────────────────────────────────────────────────────────┤

│ Subtracts Accumulated Losses, Defers & Group Holdings │

└────────────────────────────────────────────────────────┘

│

▼

[Isolated Core Capital Base: Must Match or Cross 10 Crore Rupees]

To isolate your true regulatory fund size, your accounting team must add together your paid-up equity shares, fully cash-backed premium accounts, and unencumbered free reserves. The system then subtracts your accumulated operational losses, deferred expenses, and investments inside sister companies to finalize your core capital figure.

Navigating the Baseline Ten Crore Capital Mandate

To strengthen the structural health of the non-banking finance space, the central bank updated its baseline entry guidelines. While older shadow bank setups were permitted to launch using a much lower two-crore threshold, those historical concession tracks are fully closed.

Today, the standard entry ticket for any fresh Investment and Credit Company (NBFC-ICC) seeking registration stands at a flat ten crore rupees. This full capital amount must be completely infused and sitting as unencumbered liquid deposits inside your corporate banking accounts before your legal team clicks submit on the application portal.

The Capital Origin Rule: Underwriting desks check the source of every single rupee inside your startup's core deposit block. The entire ten-crore base must consist of clean ownership equity, meaning you cannot use borrowed short-term loans, venture debt lines, or public credit advances to fulfill this regulatory threshold.

Capital Protection for Large Scale Industrial Assets

Analyzing complex corporate capitalization rules provides essential strategic advantages for elite institutional real estate managers handling downstream logistics setups. Building highly compliant alternative financing frameworks ensures maximum business continuity across regional asset holdings.

Large institutional investment firms routinely maximize their returns by executing verified corporate purchases of advanced corporate parks and mechanized warehousing centers. Equipping these modern developments with seamless credit tools allows your consumer-facing digital ecosystems to operate at peak velocity.

[Verified Corporate Purchases of Advanced Warehouse Hubs]

│

▼

┌──────────────────────────────────────────────────────────┐

│ Deploy Automated Co-Lending Credit Platforms for Tenants │

├──────────────────────────────────────────────────────────┤

│ Backed via Strict 10-Crore Ownership Equity Capital Bases │

└──────────────────────────────────────────────────────────┘

│

▼

[Premium Commercial Yields Secured via Fully Compliant Asset Infrastructures]

Furthermore, advanced enterprise networks lease these highly connected industrial structures to global brands through structured properties leased to multinats agreements. When your primary corporate income streams are secured by properties leased to multinats contracts, institutional credit providers classify your overarching credit risk profile as exceptionally secure, unlocking premium lending limits during subsequent expansion cycles.

Synergy Solutions for Modern Indian Enterprise Frameworks

The rigid validation guidelines attached to modern capital metrics support the broader business world by forcing absolute transparency across financial channels. This clarity helps fast-moving industries manage their supplier networks without encountering administrative blockages.

Expanding Runway for Startups India

Agri-tech platforms and marketplace vendors inside startups india build extensive contract networks connecting thousands of small micro-enterprises. Ensuring your alternative lending arms satisfy the netowned fund requirements for registering digital first nbfc startups india protects your platform's balance sheet post venture rounds, preventing unexpected compliance rejections from stalling your corporate timeline.

Protecting Sourcing Channels for Export Houses

Operational managers leading busy textile factories and international export houses must manage steady deliveries to pass foreign shipping checks. Encouraging your supplying blocks to use automated, app-based lending channels ensures they maintain high production continuity without freezing active corporate cash reserves.

The Scale-Based Regulation Journey for Base Layer Startups

Once your startup successfully secures its Certificate of Registration, your entity is assigned to the Base Layer under the modern Scale-Based Regulation (SBR) architecture. This regulatory structure groups finance firms by their total asset size and public interaction footprints.

As a Base Layer digital lender, your total asset book can scale safely up to one thousand crore rupees before you trigger heavy compliance layers. This structural grace window gives young tech brands ample space to build their scoring codes, test seasonal risk rates, and cultivate customer loyalty without drowning in heavy paperwork.

NBFC Entity Category | Minimum Required NOF Base | Target Operational Market Focus | Direct Impact on Startup Founders |

Standard Tech NBFC-ICC | 10 Crore Rupees Minimum | Retail consumer loans, merchant overdrafts, gadget financing | Represents the universal entry floor for fresh tech applications |

Microfinance (NBFC-MFI) | 10 Crore Rupees Minimum | Collateral-free micro-loans for low-income village households | Requires a minimum 75% deployment into low-income clusters |

Factoring Startup Setup | 5 Crore Rupees Base | Invoice discounting tools, trade bill settlements | Restricts core cash operations to active bill processing lanes |

Peer-to-Peer Marketplace | 2 Crore Rupees Base | Connecting retail investors with individual retail borrowers | Prohibits the platform from taking any balance-sheet risk |

Step-by-Step Guide to Applying for an RBI NBFC License

To organize your equity capital correctly and navigate the centralized registration portal to lock in your official credit license, follow this sequence of steps.

1.Incorporate a Fresh Corporate Structure:Phase 1.

Register a brand-new Private or Public Limited Company under the Companies Act 2013, ensuring your memorandum explicitly lists financial lending as your principal business focus.

2.Infuse the 10-Crore Equity Base:Phase 2.

Have your promoters and equity investors transfer the full ten crore rupees into an unencumbered corporate bank fixed deposit, securing a formal bank balance certificate.

3.Secure a Certified CA Capital Audit:Phase 3.

Hire an independent Chartered Accountant to perform a detailed net worth audit, drafting an official statutory certificate confirming your clean Net Owned Fund calculations.

4.Submit the Application via PRAVAAH:Phase 4.

Log into the central RBI PRAVAAH portal to upload your CA certificate, director credit reports, and technical business plans to initiate formal regulatory reviews.

Conclusion

Mastering the statutory details of netowned fund requirements for registering digital first nbfc startups india transforms a daunting licensing hurdle into a highly strategic business move. By building an unencumbered equity foundation that matches the central bank's ten-crore safety floor, your technology platform gains immediate credibility across the corporate landscape.

This robust capitalization requirement provides digital marketplaces and institutional co-lenders with a secure, highly predictable framework to handle credit operations. It values data consistency and long-term financial discipline far more than short-term scale spikes, protecting the broader retail market from sudden default shocks.

By maintaining clean transaction records, tracking your net worth metrics, and utilizing professional legal compliance pipelines, you can navigate regulatory reviews with complete ease. Transforming your fintech business strategy into a fully compliant, licensed financial company becomes a clear, highly profitable step toward securing long-term economic stability and institutional trust.

Frequently Asked Questions (FAQs)

1. Can a fintech startup use foreign direct investment (FDI) capital to fulfill the ten-crore NOF requirement?

Yes, you can legally utilize Foreign Direct Investment, or FDI capital, to satisfy your baseline net owned fund thresholds, provided your company complies fully with the latest FEMA regulations. The central investment rules allow up to one hundred percent foreign equity inside non-banking finance firms via the automated tracking channel. However, your legal team must submit detailed source-of-funds files and clear background checks to prove the inbound capital originates from a compliant international market.

2. What is the '50-50 Principal Business Test' conducted by the RBI during license evaluation?

The 50-50 test is a dual financial metric used by the banking regulator to determine if an incorporated firm qualifies as a non-banking financial institution. Under these rules, a company must prove that its financial assets constitute more than fifty percent of its total asset base after subtracting intangible items. Furthermore, the firm must show that the net revenues generated from those financial assets contribute more than fifty percent of its gross seasonal income to pass validation.

3. What happens if a registered digital NBFC's Net Owned Fund accidentally drops below ten crores during an expansion?

If an unexpected surge in credit defaults or heavy operational expenditures pulls your active Net Owned Fund down below the statutory ten-crore floor, your license enters a critical default status. Under Section 45-IA rules, the central bank has the legal authority to cancel your Certificate of Registration immediately. To protect your business, you must proactively report the drop to your regional regulator and submit a detailed capital infusion roadmap explaining how you will restore your equity base.

4. Are digital-first NBFCs allowed to accept demand deposits from regular retail users?

No, all fresh digital-first non-banking financial companies registered under the current scale-based guidelines are classified strictly as Non-Deposit Taking entities. This means your platform is completely barred from accepting everyday demand deposits, offering savings account hooks, or issuing checkbooks to the general public. Your digital lending operations must be funded entirely via your own equity reserves, corporate bank lines, or commercial paper issues.

5. How long does the RBI typically take to review and issue an NBFC license after submission?

The complete processing turnaround time for an institutional NBFC license application generally spans four to six months, depending on the quality and transparency of your submitted file. Once your application package is uploaded via the central digital portal, regional officers conduct extensive background checks on your promoters' credit track records, audit your source-of-funds logs, and evaluate your core automated underwriting software to ensure system safety.