When you get your first home loan, making that initial monthly payment feels like a huge milestone. You assume that each payment is steadily wiping out a good chunk of your actual house debt.

However, the inner mechanics of a home loan might surprise you. In the initial years, your monthly check does not split evenly between what you borrowed and what the bank charges you.

Understanding the balance between the principal vs interest component in early home loan emi repayment is vital. It changes how you view your debt and helps you make smarter choices to save money.

3 Direct Answer Snippets for Quick Understanding

1. What is the split between principal and interest in early EMIs?

During the initial years of a home loan, your EMI consists mostly of the interest component, while the principal component is very small. This happens because the bank calculates interest based on your massive total outstanding loan balance at the beginning.

2. Why does the principal component grow over time?

As you make monthly payments, your total outstanding loan balance slowly shrinks. Because the interest is always calculated on this remaining balance, the interest portion drops each month, allowing a larger share of your EMI to go toward the principal component.

3. How does extra repayment help in the early stages?

Making extra repayments early in your home loan timeline goes directly toward reducing your principal component. Dropping the principal early stops the compounding interest chain, which slashes your total loan tenure and saves you massive amounts of money.

Breaking Down the Anatomy of a Home Loan EMI

To grasp how your money is divided, you need to understand the two parts that make up an Equated Monthly Installment, or EMI.

The first part is the principal component, which is the actual cash the bank handed you to buy your property. This is the core debt you must return.

The second part is the interest component, which is the fee the bank charges you for letting you use their money. Together, these two parts form your fixed monthly payment.

The Mathematics of an Amortization Schedule

Banks use a specific process called amortization to structure your loan payments over 15, 20, or 30 years. This creates an amortization schedule.

An amortization schedule is a complete table showing every monthly payment, detailing exactly how much goes to interest and how much goes to principal.

The math dictates that interest is always calculated on the outstanding balance. Since your debt is highest on day one, your initial interest charge is also at its peak.

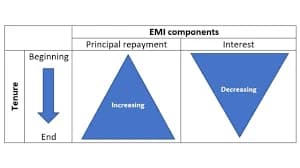

Visualizing the Principal vs Interest Component in Early Home Loan EMI Repayment

Let us look closely at what happens during the first few years of a long-term property loan. The distribution of your money is highly uneven.

In a standard 20-year home loan, up to 70 percent or even 80 percent of your early monthly payments goes purely toward paying off the interest component.

Only the tiny remaining fraction actually reduces the principal amount. This means after making 36 straight payments, your overall loan balance may have barely dropped.

Why the Initial Split Favors the Bank

This front-loaded interest structure is not a scam or a trick; it is just how compound interest math operates under standard banking rules.

Because the bank is taking a big risk by lending you a large sum of money for decades, they collect their earnings upfront. They calculate interest on the full amount owed.

As the years pass and you chip away at the mountain of debt, the ratio slowly flips. But in the early phase, the interest component completely dominates.

The Turning Point in Your Repayment Journey

If you look at a full loan schedule, you will notice a specific month where the principal component finally becomes larger than the interest component.

In a classic 20-year loan, this turning point usually does not happen until you are around year 10 or 12. It takes a long time to cross that line.

Once you pass this crossover point, your principal balance begins to tumble down much faster, accelerating your path toward full home ownership.

The Magic of Making Early Extra Repayments

Knowing that your early payments are mostly wasted on interest gives you a hidden advantage if you act early. You can change the math yourself.

When you make an extra payment on top of your regular EMI during the early years, banks do not split that extra money. It does not go toward interest.

Instead, 100 percent of your extra repayment goes directly into reducing the principal component. This shrinks the base number the bank uses to calculate next month's interest.

Real-World Example of an Early Repayment Impact

Let us see how an early intervention changes things using a straightforward scenario. Imagine a borrower with a fresh home loan.

Total Outstanding Loan: 100,000 credits

Loan Timeline: 20 Years

Current Status: Year 2 of repayment

If this borrower contributes a single extra lump-sum payment equal to just four monthly EMIs right now, the results are incredible.

Because this happens early, it knocks off a chunk of the core principal component. This single move can shorten the entire loan timeline by over a year and wipe out thousands in future interest.

Comparing Early vs Late Extra Repayments

Timing is everything when managing a home loan. Making an extra payment in year 2 has a totally different impact than making one in year 18.

Making Payments in the Early Years

An extra repayment in the first five years gives your money more time to compound in reverse. It stops decades of future interest from ever growing.

Making Payments in the Later Years

An extra payment in the final years saves very little money. By then, your interest component is already tiny, and your regular EMIs are already mostly principal.

How to Check Your Split on a Loan Statement

You do not need to guess where your money is going. Your lender is required to give you a clear breakdown of your account.

Log into your online banking portal and download your annual home loan statement. Look for the breakdown columns usually labeled "Principal Paid" and "Interest Paid."

Reviewing this statement allows you to see the exact principal vs interest component in early home loan emi repayment for your specific account.

Actionable Steps to Reduce Total Interest Costs

If you are currently in the early phase of a home loan, you can use these practical strategies to protect your wealth from heavy interest costs.

The 1-Extra EMI Rule: Try to pay just one extra full EMI every year. Doing this can slice your total 20-year loan timeline down by roughly three to four years.

Round Up Your Monthly Payment: If your EMI is a messy number, round it up to the next highest hundred or thousand. The small extra change quietly eats away at your principal.

Apply Yearly Pay Raises: Whenever you get a salary hike at work, increase your monthly home loan payment by a small percentage to speed up the repayment process.

Conclusion

Navigating the principal vs interest component in early home loan emi repayment is the ultimate cheat code for long-term financial freedom. It reveals that the true enemy in early debt management is time and a high initial principal balance.

By understanding that early EMIs are heavily weighted toward interest, you can see why waiting to pay off your loan is so expensive. Taking action today by making small, consistent extra payments directly reduces your principal component, setting you up to save a fortune and own your home free and clear much sooner.

Frequently Asked Questions (FAQs)

1. Why is my home loan principal balance barely moving after two years of regular payments?

Your balance is barely moving because standard bank amortization schedules front-load the interest charges. In the first few years, the vast majority of your monthly payment goes entirely toward covering the interest component on your large outstanding debt, leaving very little to pay down the principal.

2. If I make a partial prepayment early on, does my monthly EMI amount drop automatically?

Generally, banks will keep your monthly EMI amount exactly the same and automatically reduce your total loan tenure instead. If you specifically want your monthly payment amount to drop rather than shortening your loan timeline, you must submit a formal request to your lender.

3. Is it better to make one large lump-sum payment or small monthly extra payments?

Making extra payments as soon as you have the funds is always best because interest is calculated monthly. Small extra payments made every month during the early years will start reducing your principal component immediately, which saves more money than waiting a year to accumulate a single lump sum.

4. How can I find out the exact split of my principal and interest for next month?

You can look at the amortization schedule provided by your bank at the start of your loan, or use an online amortization calculator. By entering your current remaining balance and interest rate, you can generate a monthly chart showing the exact split for your next payment.

5. Should I prioritize early home loan repayment if my interest rate is very low?

If your home loan interest rate is exceptionally low, you should compare it to what you could earn by investing your extra cash elsewhere. If safe market investments yield a higher return than the interest rate you pay on your home, it might make more financial sense to invest rather than rushing to repay the loan.

6. Do banks charge extra fees if I want to pay down my principal early?

For floating rate home loans, regulatory bodies in most regions prohibit banks from charging any prepayment fees or foreclosure penalties to individual borrowers. However, if you have a fixed-rate loan, you must check your contract because lenders often charge a fee for early repayments.