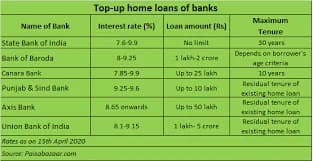

What is the top up home loan interest rate premium for non salaried profile applicants?

The top up home loan interest rate premium for non salaried profile applicants is an extra interest charge added to a self-employed borrower's base loan rate. Because business income fluctuates more than a fixed monthly salary, banking institutions apply this premium to offset perceived credit risks.

Why do banks charge a higher interest premium on top-up loans for business owners?

Banks charge a higher interest premium for business profiles because self-employed income lacks the predictable monthly consistency of a corporate salary. If a business faces a sudden downturn, loan repayment risk increases, leading banks to apply a safety buffer via a risk premium.

How can self-employed individuals lower their top-up home loan premium?

Non-salaried applicants can lower their premium by maintaining a high credit score, keeping clean audited financial statements, and showing steady cash flow. Providing proof of stable long-term revenue or high-quality asset ownership also helps convince lenders to reduce risk premiums.

TITLE: Top Up Home Loan Interest Rate Premium for Non Salaried Profile Applicants

Getting extra funds through a top-up loan against an active mortgage is an excellent way to secure affordable capital. These loans are highly popular because their interest rates are generally much lower than personal loans or credit cards.

However, securing a top-up loan is not always identical for every single borrower. Banking institutions categorize applicants based on their income stability, which directly affects the final pricing of the loan product.

Understanding the top up home loan interest rate premium for non salaried profile applicants is essential if you are self-employed. Lenders view business owners through a different risk lens, which alters your final borrowing costs.

Why Lenders Charge a Premium to Non-Salaried Borrowers

When a salaried employee applies for a loan, they provide regular monthly payslips and tax forms that show a predictable income flow. This consistent income stream makes it very easy for the bank to assess repayment capability.

For self-employed individuals, business revenues naturally rise and fall depending on the economic climate and market demand. Because of this unpredictability, banks face a slightly higher risk of payment delays if the borrower's industry enters a slow cycle.

To balance out this additional credit risk, financial institutions add an extra percentage to the base interest rate. This additional charge is known as a risk premium, and it directly shapes the total cost of your top-up loan.

Evaluating Risk Profiles and Premium Calculations

The exact top up home loan interest rate premium for non salaried profile applicants varies from one banking institution to another. Generally, the premium can add anywhere from a small fraction to a full percentage point above standard salaried rates.

Lenders determine your specific premium by evaluating your credit score, banking history, and the overall health of your industry. A clean track record with zero bounced checks helps keep this additional premium as low as possible.

[Base Home Loan Interest Rate]

│

▼

[Add: Top-Up Product Premium]

│

▼

[Add: Non-Salaried Risk Premium]

│

▼

[Final Applicable Top-Up Interest Rate]

It is important to remember that this premium applies to the entire duration of your top-up loan tenure. Calculating this added cost ahead of time ensures you can plan your business or personal cash flows accurately.

Strategic Funding Management for Premium Real Estate

High-net-worth investors often use top-up loans to unlock equity from their existing real estate holdings. When handling premium commercial assets, aligning your borrowing costs with stable income sources is a smart way to maximize returns.

Entrepreneurs who own valuable properties leased to multinats are in an excellent position to negotiate lower interest premiums. The steady, predictable rental inflows generated by multinational tenants provide banks with a strong safety guarantee.

When managing properties leased to multinats, showing these secure lease agreements can convince underwriting officers to reduce your risk profile. This direct proof of steady cash flow can successfully wipe out a large portion of the non-salaried premium.

Navigating Capital Cycles for Modern Indian Enterprises

Self-employed individuals run diverse business structures that experience unique financial phases throughout the year. Understanding how your specific corporate layout impacts the bank's assessment helps you position your application favorably.

Capital Optimization for Startups India

Founders and executive leaders driving innovative concepts within startups india frequently need quick injections of personal capital. If you are applying for a top-up loan after concluding major venture rounds, presenting your clear equity backing can help reduce the bank's risk concerns.

Balancing Cash Flow for Export Houses

Operational managers at international trade firms and busy export houses deal with large invoice amounts that clear at different times. Demonstrating a consistent history of global trade volumes helps prove to loan officers that your business can easily manage the top-up debt.

Documenting Business Strength to Minimize Premiums

To secure the lowest possible top up home loan interest rate premium for non salaried profile applicants, complete transparency is key. Providing thorough, well-organized financial records proves to the bank that your enterprise is highly stable.

Verifying Growth via Verified Corporate Purchases

When business owners expand their operations through verified corporate purchases, keeping clean balance sheets is essential. Presenting audited profit and loss statements over multiple years shows lenders that your business is growing reliably.

Maintaining Asset Profiles Across Venture Rounds

Entrepreneurs navigating consecutive venture rounds must keep their personal and corporate finances clearly separated. Showing a strong personal asset profile with zero debt defaults encourages banks to offer competitive terms on your residential top-up application.

Profile Attribute | Salaried Applicant Profile | Non-Salaried Applicant Profile |

Income Consistency | Fixed, predictable monthly deposits | Variable, fluctuating business revenues |

Primary Documents | Salary slips and formal tax forms | Audited balance sheets and bank statements |

Base Interest Pricing | Standard baseline rates with zero risk markup | Baseline rate plus non-salaried risk premium |

Approval Timeline | Fast (Standardized verification paths) | Comprehensive (Requires detailed business review) |

Maximum Tenure Option | Long-term options up to thirty years | Medium to long-term based on business age |

Step-by-Step Plan to Lower Your Top-Up Interest Premium

To ensure you secure the most affordable terms on your upcoming top-up application, follow this strategic sequence before submitting your paperwork to the bank.

1.Optimize Personal Credit Scores:Phase 1.

Check your official credit report and clear away any small outstanding credit card debts to ensure your score sits well above standard thresholds.

2.Organize Audited Financials:Phase 2.

Gather three consecutive years of fully audited balance sheets, income tax returns, and comprehensive primary business banking statements.

3.Highlight Secure Revenue Flows:Phase 3.

Isolate steady income streams, such as long-term customer contracts or corporate rentals, to show clear proof of predictable monthly cash flow.

4.Compare Multiple Lender Offers:Phase 4.

Apply to multiple banking institutions to compare their specific risk premium markups, choosing the lender that offers the most favorable terms.

Conclusion

Navigating the top up home loan interest rate premium for non salaried profile applicants requires a clear, practical understanding of how banking systems evaluate business risk. While a self-employed profile does introduce a risk markup, it should not prevent you from accessing affordable equity lines.

Whether you are running a local retail shop or managing high-value properties leased to multinats, the presentation of your financial strength makes a massive difference. Providing clean records and showing steady revenue lines keeps your borrowing costs down.

By managing your credit profile carefully and choosing the right lending partner, you can secure the funding you need without overpaying. Turning your property equity into an affordable business tool becomes a smooth, highly profitable financial move.

Frequently Asked Questions (FAQs)

1. Is the top-up loan interest rate premium permanent, or can it be reduced later?

The risk premium applied to your top-up loan is generally locked in for the initial phase of your credit agreement based on your risk profile at that time. However, if your business shows massive growth, or if your personal credit score improves significantly over the next few years, you can formally request a rate review. You can present your updated audited financials to the bank and ask for a reduction in the premium, or consider transferring the remaining balance to another bank.

2. Can a co-applicant with a salaried job help eliminate the non-salaried interest premium?

Yes, adding a close family member who holds a stable, high-earning salaried job as a primary co-applicant can significantly improve your loan terms. Lenders evaluate the collective creditworthiness of all individuals listed on the loan application file. The presence of a predictable monthly salary reduces the bank's overall risk concerns, which frequently encourages underwriting teams to lower or completely waive the non-salaried profile premium.

3. How do banks calculate the maximum top-up loan amount for self-employed individuals?

Banking institutions determine your maximum top-up loan eligibility by evaluating two main factors: your property's current market value and your net business income. Lenders calculate the current loan-to-value ratio to ensure the combined total of your primary loan and new top-up line stays within safe margins. They also analyze your net profit margins after taxes to confirm you have plenty of cash flow to cover the new monthly payments comfortably.

4. Are there any specific business sectors that face higher top-up interest premiums?

Yes, financial institutions categorize different business industries into separate risk tiers based on historical default data and market volatility. Sectors that experience sharp cyclical shifts, such as luxury retail, seasonal tourism, speculative trading, or speculative real estate construction, are often placed in higher risk brackets. Business owners operating within these volatile industries may face slightly higher interest premiums compared to those running steady, non-cyclical enterprises.

5. Does the age of my business enterprise affect the top-up loan interest premium?

The length of time your business has been continuously operating plays a major role in the bank's risk assessment process. Most commercial banks require non-salaried applicants to show a minimum of three to five years of continuous, profitable operation in the exact same line of work. A young business that has only been active for a year or two represents a higher credit risk, which can result in a higher premium or require additional asset collateral.