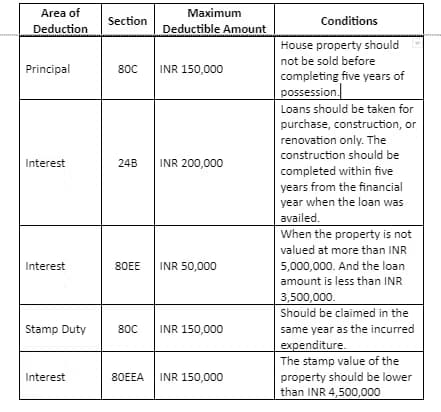

Introduction

Many people take a personal loan for different needs like education, home renovation, or business.

But one common question is: Can you get a personal loan income tax deduction?

The answer is not simple. Personal loans do not always give tax benefits. However, in certain cases, you can claim deductions if the loan is used for specific purposes.

This guide will help you understand everything in a clear and honest way.

What is Personal Loan Income Tax Deduction?

A personal loan income tax deduction means reducing your taxable income based on the interest paid on your loan.

Unlike home loans, personal loans do not automatically qualify for tax benefits.

You only get deductions if the loan is used for a valid purpose allowed under tax laws.

When Can You Claim Personal Loan Income Tax Deduction?

1. Loan Used for Home Renovation

If you use a personal loan to repair or renovate your house, you can claim a deduction on the interest paid.

This comes under the same rules as home loan interest benefits.

But you must keep proper bills and proof of expenses.

2. Loan Used for Business

If you take a personal loan for business purposes, the interest paid can be treated as a business expense.

This means you can reduce your taxable profit.

It is useful for small business owners and freelancers.

3. Loan Used for Education

If the personal loan is used for higher education, you may claim a deduction on the interest.

This works similar to education loan benefits.

However, proper documentation is very important.

4. Loan Used for Investment

If you use the loan to invest in assets like property, shares, or other income-generating investments, the interest may be deducted from the income earned.

This helps reduce your overall tax burden.

When You Cannot Claim Tax Deduction

There are many cases where personal loan income tax deduction is not allowed.

You cannot claim tax benefits if the loan is used for:

Personal expenses like shopping or travel

Buying gadgets or electronics

Wedding or lifestyle expenses

In simple words, if the loan is used for non-productive purposes, no tax benefit is given.

Documents Required for Claiming Deduction

To claim personal loan income tax deduction, you must keep proper records.

These include:

Loan agreement

Bank statements

Interest certificate from lender

Bills showing how the money was used

Without proof, your claim may be rejected.

Important Rules to Remember

Use of Loan Matters

Tax benefit depends on how you use the loan, not the loan type itself.

Always ensure your usage fits allowed categories.

Only Interest is Deductible

You can claim deduction only on the interest paid, not the principal amount.

This is an important difference from some other loans.

Proper Records Are Must

If you cannot prove how the loan was used, you cannot claim the deduction.

Keep all documents safe and organized.

Advantages of Personal Loan Income Tax Deduction

Even though personal loans don’t always give tax benefits, they still have some advantages:

Flexible usage for different needs

Quick approval process

Possible tax savings in specific cases

No collateral required

When used smartly, they can help reduce financial burden.

Common Mistakes to Avoid

Many people lose tax benefits due to simple mistakes.

Here are some things to avoid:

Not keeping proof of expenses

Using loan for mixed purposes

Claiming deduction without eligibility

Ignoring tax rules

Being careful can save you from penalties.

Tips to Maximize Tax Benefits

If you want to make the most of personal loan income tax deduction, follow these tips:

Use the loan for eligible purposes only

Maintain clear records and bills

Separate personal and business expenses

Consult a tax expert if needed

Smart planning can help you save more money.

Direct Answer Snippets

1. Can you get tax deduction on personal loan?

Yes, you can get a personal loan income tax deduction, but only in specific cases. The loan must be used for valid purposes like home renovation, business, or education. If used for personal expenses like shopping or travel, no tax benefit is allowed under Indian tax laws.

2. What part of personal loan is tax deductible?

Only the interest paid on a personal loan is eligible for tax deduction. The principal amount is not deductible. The deduction depends on how the loan is used, such as for business expenses or property renovation, and proper documents are required for claiming it.

3. Is personal loan tax-free in India?

A personal loan is not tax-free, but it is also not treated as taxable income. However, you may get tax benefits on the interest paid if the loan is used for approved purposes like education, business, or home improvement under income tax rules.

Conclusion

Personal loan income tax deduction is not automatic, but it is possible.

The key factor is how you use the loan amount.

If used wisely for approved purposes like business, education, or home renovation, you can reduce your tax burden.

Always keep proper documents and follow the rules carefully.

With the right approach, a personal loan can be more than just financial support—it can also help you save on taxes.

FAQs

1. Can I claim tax deduction on a personal loan for travel?

No, personal loans used for travel or personal expenses do not qualify for tax deduction. Only specific uses like business or education are eligible.

2. Is principal repayment of personal loan tax deductible?

No, only the interest paid is eligible for deduction. The principal repayment does not provide any tax benefit.

3. Can salaried employees claim personal loan tax benefits?

Yes, salaried individuals can claim deductions if the loan is used for eligible purposes like home renovation or education and proper proof is available.

4. Do I need proof to claim deduction?

Yes, you must provide documents like bills, loan statements, and interest certificates to support your claim.

5. Can I claim deduction for mixed-use personal loan?

No, if the loan is used for both personal and eligible purposes, it becomes difficult to claim deductions. It is better to keep usage separate.

6. Is personal loan better than home loan for tax saving?

No, home loans offer more direct and higher tax benefits. Personal loans only provide limited deductions based on usage.