2 Lakh Personal Loan Repayment Tenure Options: How to Choose the Best Term

Borrowing a ₹2 Lakh personal loan is a practical way to manage urgent expenses. Whether you are funding a wedding, handling a medical emergency, or renovating your home, this loan amount can bridge your financial gaps.

However, getting the loan is only the first step. The most critical decision you must make during the application process is selecting the right repayment period.

The 2 lakh personal loan repayment tenure options you choose will directly dictate your monthly budget and the total cost of borrowing. This detailed guide will break down your choices so you can borrow confidently and responsibly.

Direct Answer Snippets for Quick Understanding

What are the tenure options for a 2 Lakh personal loan?

Most banks and financial institutions offer 2 lakh personal loan repayment tenure options ranging from 12 months to 60 months (1 to 5 years). A few digital lenders might offer short terms starting at 3 or 6 months, while select premium banks extend options up to 72 or 84 months for eligible salaried individuals.

How does tenure affect my 2 Lakh personal loan EMI?

Your repayment tenure has an inverse relationship with your Equated Monthly Installment (EMI). Choosing a shorter tenure means you will pay higher monthly EMIs, but you will save significantly on interest costs. Conversely, a longer tenure reduces your monthly EMI burden but increases the total interest you pay over time.

Which repayment tenure should I choose for a 2 Lakh loan?

The best tenure depends entirely on your current monthly savings. If your budget allows, choose a shorter tenure of 12 to 24 months to clear the debt quickly and save on interest. If you need financial breathing room, opt for a 36 to 60-month tenure to keep EMIs manageable.

Understanding Personal Loan Repayment Tenures

A personal loan tenure is the fixed period of time given by a lender to pay back the borrowed amount along with interest. For a ₹2 Lakh loan, lenders do not use a one-size-fits-all approach. Instead, they offer flexible timelines to match your financial capacity.

Repayment is structured through EMIs, which consist of both the principal amount and the interest. Every month, a portion of your payment goes toward reducing your initial ₹2 Lakh debt, while the rest covers the lender's interest charges.

When you look at 2 lakh personal loan repayment tenure options, you are essentially choosing how many slices you want to cut your debt into. More slices mean smaller pieces, but the cake sits on the counter longer, accumulating more interest.

Breaking Down the 2 Lakh Personal Loan Repayment Tenure Options

Lenders generally categorize their repayment timelines into three main buckets. Let us look at how each bucket operates for a ₹2 Lakh loan.

1. Short-Term Tenure Options (12 to 24 Months)

Short-term options require you to repay the entire ₹2 Lakh plus interest within one to two years. This is an aggressive repayment strategy suited for individuals with a steady, high disposable income.

Pros: You get out of debt very quickly. Because the lender charges interest for a shorter duration, your total interest payout is minimal.

Cons: Your monthly EMIs will be significantly high. If an unexpected expense pops up, a high EMI can strain your monthly household budget.

2. Medium-Term Tenure Options (24 to 36 Months)

A medium-term tenure of two to three years represents the sweet spot for the average borrower. It offers a balanced approach to debt management.

Pros: The EMIs drop to a comfortable mid-range level, making it easier to manage alongside routine bills. The total interest remains reasonable.

Cons: You will remain in debt for a longer period than a short-term plan, and the interest cost will be higher than a 12-month plan.

3. Long-Term Tenure Options (48 to 60+ Months)

Long-term options stretch your repayment over four to five years. Lenders frequently market these options to make large loan amounts look highly affordable.

Pros: Your monthly financial commitment drops to its lowest possible level. This ensures you rarely risk missing a payment due to cash flow issues.

Cons: The total interest you pay can sometimes equal a massive percentage of your original ₹2 Lakh principal. You carry the mental burden of debt for years.

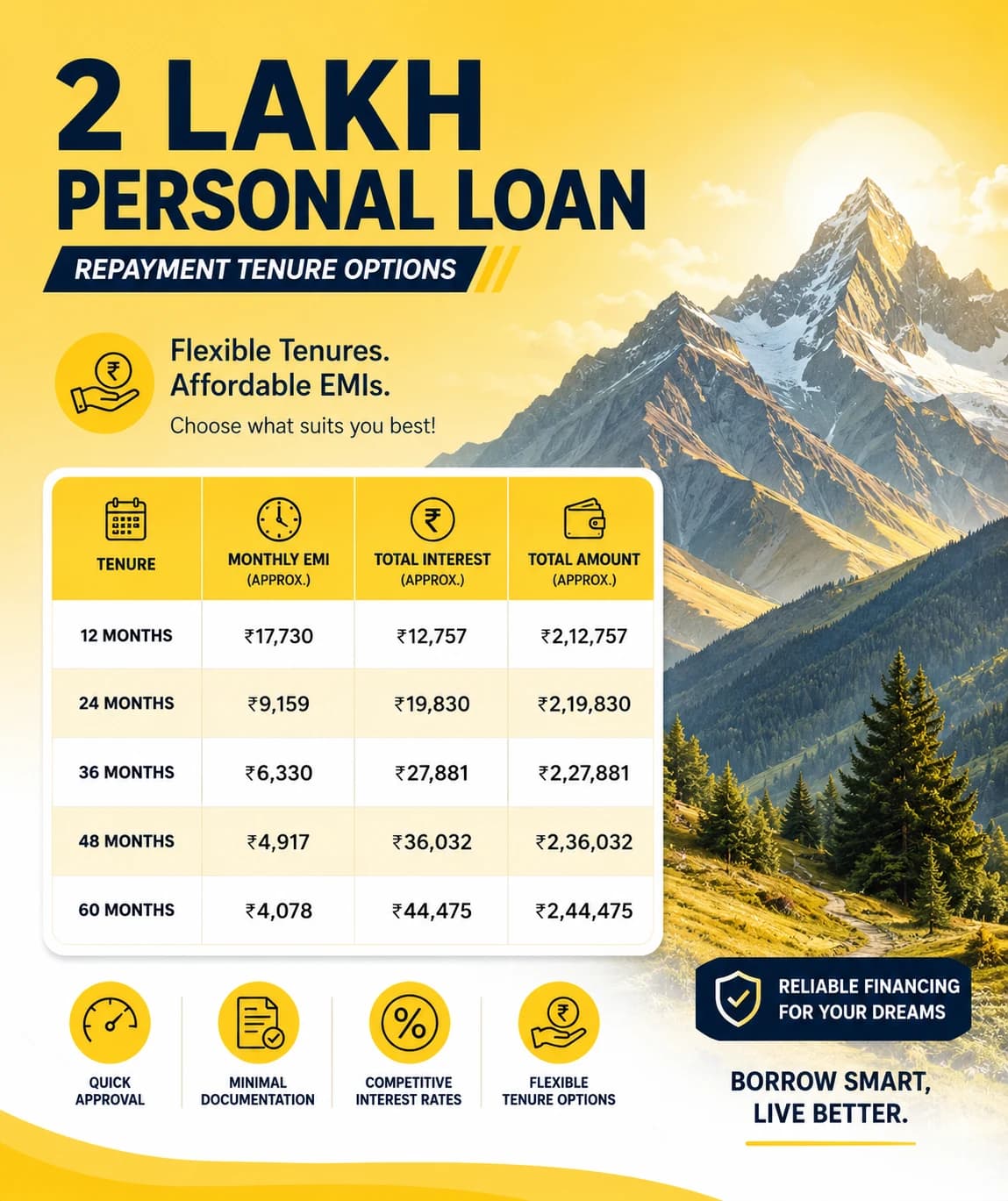

How Tenure Impacts Your EMI and Total Interest Cost

To truly understand how 2 lakh personal loan repayment tenure options work, we must look at the math. Let us assume a standard, competitive interest rate of 12% per annum on a ₹2 Lakh personal loan using a reducing balance method.

Tenure (Months) | Approximate Monthly EMI | Total Interest Payable | Total Repayment Amount |

|---|---|---|---|

12 Months | 17,770 | 13,240 | 2,13,240 |

24 Months | 9,415 | 25,955 | 2,25,955 |

36 Months | 6,643 | 39,145 | 2,39,145 |

48 Months | 5,267 | 52,810 | 2,52,810 |

60 Months | 4,449 | 66,930 | 2,66,930 |

Analyzing the Data

Look closely at the jump between 12 months and 60 months. By stretching the loan to 5 years, your monthly EMI drops from 17,770 to just 4,449. This looks incredibly attractive on paper.

However, look at the interest column. At 12 months, you only pay 13,240 in interest. At 60 months, that figure skyrockets to 66,930. You end up paying over an extra 53,000 to the bank just for the luxury of more time.

Key Factors to Consider When Choosing Your Tenure

Do not guess your tenure at the time of application. Evaluate these crucial parameters to pick the most efficient timeline for your life.

Your Monthly Income and Fixed Obligations

Calculate your Fixed Obligation to Income Ratio (FOIR). Lenders prefer that all your monthly debt payments (including the new loan) consume less than 40% to 50% of your net monthly take-home salary.

The Purpose of Your Loan

If you are borrowing for an investment or an asset that adds value, a medium or long term might be justified. If you are borrowing for a temporary luxury like a vacation, aim for a short-term tenure so the memories do not outlive the debt.

Prepayment and Foreclosure Rules

Check if your lender allows you to pay off the loan early. If you choose a 48-month tenure but get a work bonus, can you pay off the remaining balance without heavy penalties? Opt for lenders with flexible prepayment clauses.

Job and Income Stability

If your industry experiences seasonal layoffs or income fluctuations, picking a slightly longer tenure provides a safety cushion. You can always make part-payments later if your contract turns out to be stable.

Mistakes to Avoid When Selecting a Repayment Plan

Many borrowers fall into traps that cost them thousands of rupees. Keep these common mistakes in mind when reviewing your options.

Focusing ONLY on the Lowest EMI: Lenders love highlighting low EMIs. Always calculate the total interest cost over the life of the loan before signing the agreement.

Overestimating Your Repayment Capacity: Do not sign up for an aggressive 12-month tenure if it leaves you with zero emergency savings at the end of the month.

Ignoring the Fine Print on Processing Fees: Longer tenures sometimes carry different administrative costs or hidden charges. Always ask for the Annual Percentage Rate (APR), which shows the true cost of the loan.

Conclusion: Balancing Affordability and Savings

Choosing from the available 2 lakh personal loan repayment tenure options requires a realistic assessment of your financial health. There is no single "correct" answer; the ideal option is one that fits comfortably into your budget without causing stress, while keeping your interest costs as low as possible.

If your income is high and secure, opt for a short-term plan of 12 to 24 months to save money. If you prefer financial safety and predictability, a medium-term plan of 36 months offers a great compromise. Use an online EMI calculator, test different scenarios, and pick the timeline that keeps you in control of your financial future.

Frequently Asked Questions (FAQs)

1. Can I change my 2 Lakh personal loan repayment tenure after the loan is disbursed?

Generally, no. Once the loan agreement is signed and the money is sent to your account, the tenure is locked in. The only way to effectively shorten your tenure is by making regular part-prepayments or fully foreclosing the loan early, depending on your bank's policies.

2. Is it better to choose a 1-year or a 5-year tenure for a ₹2 Lakh loan?

If you want to save money, a 1-year tenure is vastly superior because it minimizes interest. If your primary goal is to protect your monthly cash flow from heavy bills, a 5-year tenure is better. Most financial experts recommend a middle ground of 2 to 3 years for this specific loan amount.

3. Do lenders charge a penalty if I pay off my ₹2 Lakh loan ahead of schedule?

Yes, many traditional banks charge a foreclosure fee ranging from 2% to 5% of the remaining principal balance if you close the loan early. However, many modern digital NBFCs and fintech lenders now offer zero foreclosure charges after a specific number of EMIs have been paid. Always check this before applying.

4. Will choosing a longer tenure affect my credit score?

The length of the tenure itself does not directly hurt or help your credit score. What matters is your payment history. A longer tenure provides lower EMIs, which might help you maintain a flawless record of timely payments, boosting your score over time.

5. Does the interest rate change based on the repayment tenure I select?

Sometimes, yes. Some lenders charge a slightly higher interest rate for maximum tenures (like 60 months) because keeping a loan open longer increases the risk of default. Short to medium tenures often receive the most competitive interest rate offers.

6. What happens if I fail to pay my EMI during a long repayment tenure?

Missing an EMI results in late payment fees, bounces charges from your bank, and a severe drop in your credit score. If you continue to miss payments, the lender will classify your account as a Non-Performing Asset (NPA) and initiate legal recovery procedures.