Fulfilling the dream of building, buying, or expanding your own home is an emotional and proud milestone for every family across India. If you are starting out with a modest budget, managing your borrowing choices carefully keeps your finances fully secure.

Choosing a highly manageable principal tier, like five lakh rupees, is the perfect way to finish property construction without straining your daily living costs. Thankfully, exploring a 5 lakh home loan SBI special scheme path provides deep financial relief.

Lenders like the State Bank of India run tailored, community-focused portfolios specifically engineered for low-income brackets, small traders, and rural households. This clear, honest guide removes confusing bank terminology to showcase SBI's most affordable credit tracks, real-life costs, and smooth approval methods.

Google Featured Snippet Answers

What is the 5 lakh home loan SBI special scheme for affordable housing? The 5 lakh home loan SBI special scheme framework operates through targeted portfolios like SBI Aashray or SBI Gram Niwas. These special packages focus heavily on financial inclusion, offering competitive repo-linked floating interest rates, relaxed income validation tracks, and complete paperwork processing fee waivers for budget-conscious borrowers.

What is the monthly EMI for an SBI five lakh housing loan? Assuming a competitive, benchmark-linked starting interest rate tier of 8.25% per annum, an SBI five lakh credit line features highly predictable costs. Choosing a standard ten-year repayment tenure sets your monthly installment bill at approximately 6,136 rupees, making it highly secure for student families.

How does SBI's affordable housing scheme support informal sector workers? Under specialized initiatives like the SBI Aashray program, individuals working in the unorganized sector can qualify without formal salary vouchers. SBI evaluates your digital transaction tracking logs, such as twenty-four months of continuous mobile UPI histories, to verify your monthly repayment power safely.

Exploring SBI's Top Affordable Housing Schemes

When researching a 5 lakh home loan SBI special scheme pathway, you will discover that India's largest public lender does not follow a one-size-fits-all model. They structure distinct loan products to match unique living environments and working backgrounds.

The SBI Aashray Home Loan Portfolio

The Aashray portfolio is a groundbreaking program designed specifically for families belonging to the Economically Weaker Section or Low Income Group in urban regions. It targets individuals who possess a steady cash flow but lack rigid corporate document footprints.

If you operate a local retail store, practice a traditional artisanal trade, or work a freelance gig position, this program is custom-made for you. It completely skips the requirement for formal salary slips, using your digital transaction trail to confirm your creditworthiness instead.

The SBI Gram Niwas Rural Initiative

If your dream property is located inside a native country village or a growing semi-urban township, the Gram Niwas framework is your ideal match. This rural-focused program aims to replace temporary mud structures with strong, permanent brick houses.

Gram Niwas Program = Wave Off Processing Fees + Tailored Village Plot Financing

A primary benefit of selecting this rural portfolio is the absolute exclusion of standard administrative handling charges. SBI completely waives your upfront processing paperwork fees, ensuring your initial out-of-pocket setup costs stay at absolute zero.

Amortization Matrix: Visualizing Your Future Payments

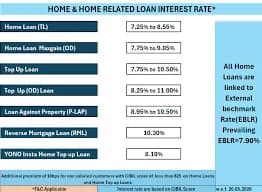

To organize your household cash flow accurately before stepping into a local bank branch, check how an SBI five lakh loan balance operates across standard tenures at a baseline interest rate of 8.25% per annum:

Principal Amount | Annual Interest Tier | Selected Tenure | Estimated Monthly EMI | Total Interest Costs | Absolute Final Repayment |

|---|---|---|---|---|---|

5 Lakhs | 8.25% | 5 Years | 10,199 Rupees | 1,11,957 Rupees | 6,11,957 Rupees |

5 Lakhs | 8.25% | 10 Years | 6,136 Rupees | 2,36,376 Rupees | 7,36,376 Rupees |

5 Lakhs | 8.25% | 15 Years | 4,850 Rupees | 3,73,115 Rupees | 8,73,115 Rupees |

5 Lakhs | 8.25% | 20 Years | 4,258 Rupees | 5,22,118 Rupees | 10,22,118 Rupees |

Core Eligibility Filters for Special Bank Concessions

Even though a 5 lakh home loan SBI special scheme is built to maximize public welfare, applicants must still satisfy a few simple baseline banking safety checks to gain approval.

Clean Credit History Foundations

SBI assesses your financial honesty by scanning your electronic credit bureau history. Holding a CIBIL profile score safely above 725 shows that you clear your past micro-advances or utility balances on time, allowing you to secure the absolute lowest interest rate tiers.

The First-Time Homeowner Condition

For specialized affordable housing initiatives tied directly with central programs like PMAY Urban 2.0, the beneficiary household must be entering the property market for the first time. The applicant and their immediate dependent family must not own a separate permanent pucca house anywhere in India.

Digital Banking Footprint Requirements

If you are applying through informal income channels without standard corporate tax paperwork, your transaction track record is critical. Lenders require that you show a satisfactorily maintained, active running savings bank account or a consistent UPI payment history for a minimum period of twenty-four months.

Step-by-Step Guide to Activating Your SBI Loan File

Do not feel overwhelmed by the thought of interacting with bank officers. Following a structured roadmap ensures your application flows through the system smoothly.

Step 1: Fix Identity Documentation Errors

Three months before visiting a branch, verify that your name spelling, parental initials, and permanent address match perfectly across your Aadhaar card, PAN card, and voter card. Even a tiny spelling mismatch can stall your automated validation checks.

Step 2: Leverage the JanSamarth Online Portal

For programs like the Aashray package, you can initiate your application digitally via the unified government JanSamarth portal. The digital system runs a fast initial scan of your credentials, granting an instant in-principle approval tracker that speeds up your local branch processing times.

JanSamarth Digital Application = Fast Tracking + Automated System Clearances

Step 3: Complete Technical Asset Audits

Once your initial financial checks pass, SBI routes your property blueprints to their internal panel of engineers and legal title lawyers. If the property deeds show a clean history free of boundary disputes, the branch releases the five lakh funds straight to your construction manager or vendor.

Conclusion

Securing a 5 lakh home loan SBI special scheme package is a highly secure, smart, and affordable strategy to bring your permanent housing goals to life. Portfolios like SBI Aashray and Gram Niwas prove that you do not need an expensive corporate salary or complicated paperwork to partner with India's largest bank.

Focus your initial energy on keeping your mobile transaction histories completely clean, updating your KYC identity cards early, and choosing a balanced repayment tenure that preserves your daily savings. With transparent planning and disciplined budget habits, you can confidently build your family home while keeping your long-term financial freedom perfectly intact.

Frequently Asked Questions

Does SBI charge extra penalty fees if I clear my five lakh loan ahead of schedule? No, if your home loan contract relies on a standardized floating interest rate benchmarked to central policy rates, SBI charges absolute zero prepayment or foreclosure penalties. You can pay extra cash into your account whenever you have it to wipe out your debt early.

Can a homemaker or student apply as a primary borrower under these schemes? A student or housewife can easily apply for the loan, but they must include a working family member, such as a parent, sibling, or spouse, as an active income-earning co-applicant to guarantee regular monthly repayments to the bank safely.

Are there special interest rate concessions for women borrowers at SBI? Yes, SBI is a strong champion of women's financial independence. They offer a direct, permanent interest rate concession for women applicants, provided the female member acts as the primary sole property owner or joins the file as the first co-applicant.

What happens to my affordable loan if market interest rates rise unexpectedly? Since affordable portfolios use benchmark-linked floating rates, your terms will adjust naturally alongside central policy movements. When rates climb, SBI typically extends your remaining loan tenure months first to protect your current monthly payment from rising sharply.

Can I use a 5 lakh home loan SBI special scheme option to buy an open land plot? Standard affordable housing variants are strictly restricted to the purchase of ready-to-move flats, self-construction on owned land, or structural renovation of an existing kutcha structure. If you only want to buy an open plot without immediate construction, you must ask for an SBI Realty loan.

Do I need a high corporate income tax return record to qualify for SBI Aashray? No, the core design of the Aashray product line completely removes the need for formal corporate income tax filings. The bank relies entirely on checking your electronic banking history and digital wallet footprints over twenty-four months to confirm your eligibility.