8. 5 Lakh Home Loan Documents Required List: A Beginner's Complete Checklist

Stepping into your own home or starting a fresh home extension project is a wonderful milestone. When you apply for a manageable financing amount, like eight and a half lakh rupees, your application journey depends entirely on how clean your paperwork looks.

Even for a smaller borrowing pool, Indian lenders must stick to strict national verification laws. Knowing the 8. 5 lakh home loan documents required list beforehand helps you bypass unexpected delays and secures a fast bank approval.

This clear, honest guide removes confusing banking terms to give you a straightforward checklist. We break down the exact identity proofs, income verifications, and property papers required for both salaried and self-employed applicants.

Google Featured Snippet Answers

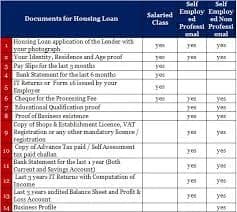

What is the basic 8. 5 lakh home loan documents required list in India? The basic 8. 5 lakh home loan documents required list includes standard Know Your Customer (KYC) identity proofs like an Aadhaar card and PAN card. Alongside personal ID, you must present your past six months of official bank account statements and the legal ownership deeds of the property being financed.

What financial documents do salaried workers need for a small home loan? Salaried employees must provide their official salary slips from the past three consecutive months, their latest Form 16 tax certificates, and two years of filed Income Tax Returns. Lenders use these documents to verify your job stability and calculate your net monthly take-home pay.

What paperwork must a self-employed individual submit for a housing loan? Self-employed business owners must present two to three years of officially filed Income Tax Returns alongside detailed business profit and loss statements. Lenders also require verified business address certificates, such as local trade licenses, shop establishment registrations, or active GST certificates.

The Core KYC Pillar: Proving Your True Identity

Before a bank analyzes your monthly earnings, they must legally verify your citizenship and permanent residential track record under national Know Your Customer rules.

Every single document you hand over must be fully legible, officially valid, and free of spelling mismatches. Even a tiny typing difference in your middle name across different cards can cause a bank's system to halt your file.

Master KYC Checklist for All Borrowers

To make your initial application visit smooth, gather at least one primary document from each of these standard regulatory categories:

Document Category | Accepted Verification Options (Choose One) |

|---|---|

Official Photo Identity Proof | Aadhaar Card, Valid Passport, PAN Card, Voter ID Card, or Driving License |

Permanent Residential Address Proof | Aadhaar Card, Recent Electricity Bill, Water Tax Receipt, or Gas Pipeline Bill |

Official Date of Birth Verification | PAN Card, Birth Certificate, or 10th Class School Leaving Marksheet |

Additional Personal Essentials | 3 to 4 Recent Passport-Sized Photographs (Signed Across the Front Surface) |

Income Proofs for Salaried Corporate Employees

Your stable job profile is a powerful asset when applying for a housing loan. Lenders prefer salaried positions because they offer a highly predictable timeline for monthly loan repayments.

To pass the financial review phase easily, you must prove your active job continuity by providing structured employment records.

Clean Monthly Bank Credits + Timely Tax Filings = Instant Income Verification

1. Recent Pay Invoices

You must provide your official salary slips for the past three consecutive months. If your workplace includes variable bonus incentives or seasonal overtime pay, ensure these extra details show up clearly on the printed slips.

2. Tax Track Records

Lenders require a copy of your latest Form 16 certificates alongside your filed Income Tax Returns for the past two fiscal years. These tax summaries act as official verification of your career honesty and steady earning power.

3. Active Bank Statements

Provide a full, unedited statement of your primary salary bank account covering the past six months. The bank verification system will match this log to ensure your stated salary credits match the electronic transfers perfectly.

Income Proofs for Self-Employed Business Owners

Acquiring a home loan when you run your own local shop, trading firm, or independent freelance practice follows a slightly different review path. Because your monthly cash flow fluctuates naturally, banks look closely at your long-term business performance instead of a fixed monthly paycheck.

1. Multi-Year Income Tax Returns

Self-employed individuals must present their officially filed Income Tax Returns for the past two to three consecutive years, complete with full income computation charts.

2. Certified Financial Statements

You must submit your business balance sheets and formal profit and loss statements covering the past three years. If your annual business turnover crosses legal tax audit thresholds, these financial pages must bear the formal seal and signature of a certified Chartered Accountant.

3. Proof of Business Legitimacy and Location

To prove your business is fully active and legally registered, add these operational certificates to your 8. 5 lakh home loan documents required list:

An active GST Registration Certificate alongside your latest tax return filings.

A local municipal Trade License or a state-level Shop and Establishment Act registration.

A professional practice license if you operate as a certified doctor, lawyer, or consultant.

Mandatory Property Documents for Bank Verification

Meeting the income standards is only half the puzzle. The property you intend to buy, construct, or renovate must also pass strict legal checks before a lender releases any funds.

Legal Title Deeds and Sales Agreements

The bank's legal panel must review the original registered sale deed or a stamped agreement for sale between you and the property vendor. This paperwork ensures that the chain of ownership is completely clear, clean, and free of existing legal disputes.

Approved Building Blueprints and Local Clearances

If you are building an independent house or extending a room, you must submit the official construction cost estimates drafted by an approved architect. Alongside these estimates, you must provide the approved structural floor plans and construction permissions signed by your local municipal authorities.

No-Objection Certificates (NOC)

If you are purchasing a flat inside a managed residential complex, you must provide an official No-Objection Certificate issued directly by the registered housing society or builder. This document confirms that the community has zero objections to you creating a bank mortgage on the property.

Conclusion

Compiling your 8. 5 lakh home loan documents required list carefully is the ultimate secret to a fast, stress-free property loan approval. When your identity documents are uniform, your income certificates are tidy, and your property deeds are legally clear, lenders can process your application with absolute confidence.

Take your time to organize your records in a secure folder, double-check that your credit files contain zero errors, and clear up any small lingering credit card bills before applying. With solid preparation, you can cruise through the bank's checklist and bring your dream home project to life seamlessly.

Frequently Asked Questions

Can I submit scanned photocopies instead of original documents? During your initial consultation and digital upload phase, clean scanned photocopies are perfectly fine. However, before the bank formally approves your loan and releases the funds, their verification officers must physically check your original identity cards and property deeds to protect against financial fraud.

Is a PAN card mandatory for an 8.5 lakh housing loan application? Yes, a valid PAN card is mandatory for all formal home loan applications across India. If your PAN card contains an outdated home address or a misspelled family name, you should update your information online before submitting your final loan file to the bank.

What happens if I do not possess Form 16 certificates? If your employer does not issue standard Form 16 certificates, you can easily substitute them by providing your officially filed Income Tax Returns alongside your formal job appointment letter, your regular work identity card, and clear bank statements showing your salary credits.

Do I need to arrange an independent guarantor's paperwork for this loan size? For a highly manageable amount like eight and a half lakh rupees, a separate third-party loan guarantor is rarely required if your individual credit score sits safely above 725. Lenders usually only ask for a guarantor's files if your personal income falls close to their minimum entry limits.

How far back do lenders look into my bank account statements? Lenders universally require a full, uninterrupted tracking statement of your primary operational savings and business current accounts for the past six consecutive months. This window lets them check your daily balance habits and ensure you have zero bounced checks on your record.

Can I use a rent agreement as a valid address proof for a home loan? Yes, a formally registered rental agreement printed on official stamp paper is widely accepted as a valid proof of current residence by major Indian banks. You can use it alongside your permanent hometown address listed on your Aadhaar card to establish your residency track record.