Life often presents sudden financial situations where you need quick cash. You might face an unexpected medical bill, an urgent business requirement, or a short-term family expense. When this happens, breaking your running Fixed Deposit (FD) early is usually the first thought that comes to mind.

However, closing an FD prematurely causes a permanent loss of future interest and triggers penalty fees from the bank. Fortunately, the State Bank of India provides a much smarter financial alternative. The od facility against fixed deposit interest rate difference sbi structure allows you to keep your savings active while unlocking a flexible credit line at highly competitive rates.

In this guide, we will break down exactly how this overdraft account functions, look at the precise interest rate margin charged by the bank, and explain how you can use it to manage emergencies without hurting your long-term wealth building.

Direct Answer Snippets for Quick Understanding

What is the interest rate difference for an SBI overdraft against an FD?

The od facility against fixed deposit interest rate difference sbi rules enforce a strict and transparent one percent pricing markup. This means the interest rate charged on your overdraft account is exactly one percent higher than the original interest rate your fixed deposit is currently earning from the bank.

How does the daily interest calculation save you money?

Unlike a standard personal loan where interest accumulates on the entire sanctioned balance, an SBI FD overdraft calculates interest on a daily reducing balance method. You are charged the one percent premium strictly on the exact amount of cash you withdraw and use, and only for the specific days the balance stays negative.

What is the maximum credit limit available for an SBI FD overdraft?

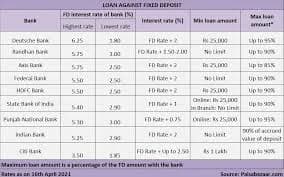

When you apply for this facility online via the SBI internet banking portal or YONO app, you can typically borrow up to ninety percent of your cumulative fixed deposit value. If you visit a physical bank branch, you can access a flexible limit framework based on the remaining maturity period of your underlying time deposit.

Understanding the Concept of an Overdraft Against an FD

An Overdraft (OD) facility is a specialized banking tool that turns your locked investment into a revolving credit line. Instead of breaking your financial asset, you give the bank permission to place a temporary legal claim, called a lien, on your fixed deposit.

Once this lien is registered, SBI creates a virtual credit pocket for you. The original deposit remains completely safe inside the bank vault and continues to generate compound market interest every single day.

The primary benefit of this system is absolute convenience. You do not have to deal with intense physical background verifications or wait days for asset checks, because the bank already holds your verified collateral security.

Decoding the One Percent Interest Rate Difference

The defining feature of this product is its transparent and highly affordable cost structure. Most unsecured personal loans carry steep interest rates that can drain your monthly savings quickly.

SBI simplifies this pricing by linking the overdraft directly to your asset's earning rate. If you have an active long-term fixed deposit that is successfully earning an annual interest rate of 6.50 percent, the math for your overdraft line works out perfectly:

$$\text{Overdraft Interest Rate} = \text{Underlying FD Rate} + 1\%$$

Applying this rule means your temporary borrowing rate will be exactly 7.50 percent per annum. This tiny interest rate gap makes an FD-backed overdraft one of the cheapest and most secure short-term borrowing methods available in the Indian banking landscape.

Practical Example of How the System Works

Let us look at a real-world scenario to see how the od facility against fixed deposit interest rate difference sbi setup protects your household budget.

Suppose you have an active SBI fixed deposit worth two Lakh INR earning a steady interest rate. You face an unexpected vehicle repair charge of twenty-five thousand INR, and you expect to receive a work bonus to cover it in twenty days.

Option A (Breaking the FD): You break the entire two Lakh deposit early. The bank cancels your long-term wealth accumulation and applies a premature closure penalty fee, reducing your lifetime earnings.

Option B (Unlocking the OD Line): You open an online overdraft account and withdraw twenty-five thousand INR. Your two Lakh FD continues earning its regular interest. After twenty days, your bonus arrives, and you deposit twenty-five thousand INR back into the account.

By choosing the overdraft track, you pay the minor one percent interest premium only on the twenty-five thousand INR you used for those twenty days. The rest of your two Lakh investment remains untouched, allowing your primary savings goal to grow safely without disruption.

Core Features and Rules of SBI FD Overdraft Accounts

Before activating this credit line from your smartphone, you should memorize the primary operational limits set by the bank.

Flexible Transaction Limits

SBI allows a high degree of transactional freedom for individual users. The minimum loan amount required to open an online overdraft against a fixed deposit is twenty-five thousand INR, while the upper ceiling for digital applications is capped at a generous five crore INR.

Absolute Processing Cost Freedom

Because you are borrowing against your own money, SBI takes an incredibly friendly approach toward administrative fees. There are zero processing fees required to set up the overdraft, and you will never face early prepayment or foreclosure penalties if you close the account ahead of schedule.

Timeline Mapping Constraints

The maximum operational tenure of your overdraft line is strictly mapped to the remaining lifespan of your underlying deposit. The account must be fully settled and closed before or on the exact day your core fixed deposit reaches its official maturity date.

Step-by-Step Guide to Apply Online

You do not need to waste hours standing in long branch queues to access this emergency money. You can execute the entire process digitally via SBI NetBanking.

Step 1: Log In to Your Portal

Visit the official SBI online banking website and log in securely using your private user ID and password credentials. Navigate to the primary dashboard tabs.

Step 2: Select the Overdraft Option

Click on the 'e-Fixed Deposit' tab located on the top menu bar. From the dropdown list of automated financial services, select the 'Overdraft Against Fixed Deposit' link.

Step 3: Choose Your Account and Verify

The system will instantly display your eligible single-name fixed deposits. Select the specific deposit you want to link, verify the displayed credit limit and interest rate details, and authorize the digital request by entering a secure One-Time Password (OTP) sent to your phone. The extra funds will be ready for use instantly.

Conclusion

Utilizing the od facility against fixed deposit interest rate difference sbi program is one of the most efficient ways to address short-term cash flow gaps without hurting your core financial plans. By taking advantage of the minor one percent interest rate gap and utilizing the flexible daily reducing balance system, you can handle unexpected bills easily while keeping your investment intact. Ensure you keep track of your core deposit's maturity timeline, clear your utilized balances promptly, and use this secure overdraft track to keep your long-term household wealth building completely safe and successful.

Genuine Frequently Asked Questions (FAQs)

1. Do I need a high CIBIL credit score to qualify for an SBI FD overdraft?

No, your traditional CIBIL credit score does not act as a strict barrier for an SBI fixed deposit overdraft. Because the loan is fully secured by your own money held inside the bank vault, SBI waives regular credit score checks and income proof submissions, making it an excellent path for students or freelancers.

2. Can I get an online overdraft facility against a joint fixed deposit account?

No, the instant online overdraft service via SBI NetBanking or the YONO app is strictly restricted to fixed deposits held in a single name. If your fixed deposit is held jointly by two or more individuals, all members must physically visit their local SBI home branch together to sign the manual mortgage deeds.

3. Can I use the overdraft facility against an SBI Tax Saving Fixed Deposit?

No, under current Indian tax regulations, you cannot pledge or avail of an overdraft facility against an SBI Tax Saving Scheme deposit. These specialized tax-saving instruments carry a mandatory five-year lock-in period during which the funds cannot be touched, linked, or used as collateral for any loan.

4. What happens if I fail to repay the overdraft balance before my FD matures?

If a borrower fails to clear the outstanding negative balance of their overdraft account before the final deadline, SBI will automatically adjust the dues during the FD maturity processing phase. The bank will subtract your pending principal and interest from your total deposit pool and credit the remaining balance to your savings account.

5. Do I receive a physical checkbook and debit card for my SBI Maxgain or FD OD account?

Yes, when you open an overdraft facility against your fixed deposit at an SBI branch, the account functions similarly to a traditional current account. You can request a dedicated checkbook and link it to your active banking channels, allowing you to use net banking or transfer funds easily during household emergencies.