Buying a new vehicle is an exciting milestone for any individual or family. However, figuring out how to finance that vehicle can quickly become confusing with all the banking terms used by lenders.

When shopping for an auto loan, you will frequently hear about different ways to calculate interest. Choosing the right calculation system can save you a massive amount of cash over the life of your vehicle loan.

Using a car loan emi calculator with reducing balance method helps you see exactly how your monthly payments are split. It reveals the honest truth about how your debt shrinks with every single payment you make.

Direct Answer Snippets for Quick Understanding

1. What is the reducing balance method for car loans?

The reducing balance method calculates your monthly loan interest only on the remaining principal you still owe, rather than the initial amount you borrowed. As you pay off your main loan balance each month, the interest amount drops, making this a highly cost-effective option.

2. How does a reducing balance car loan calculator work?

A car loan emi calculator with reducing balance method takes your total vehicle loan amount, the annual interest rate, and the timeline. It uses an amortization formula to show how your interest drops and your principal repayment grows larger with each monthly payment.

3. Why is the reducing balance method better than a flat rate?

The reducing balance method is vastly superior to a flat-rate system because it saves you money. Flat rates charge interest on your original loan amount for the whole timeline, while the reducing method drops your interest fees as you pay down your debt.

Understanding the Core Concepts of Vehicle Financing

Before jumping into calculations, it helps to understand what an Equated Monthly Installment, or EMI, actually represents. Your EMI is a fixed sum of money you pay the lender every month until the vehicle is fully paid off.

Every monthly payment you make is split into two distinct parts. One piece goes toward paying down the actual cost of the vehicle, while the other piece covers the interest fee.

Lenders use different calculation math to decide how large that interest fee should be each month. The two main systems are the flat-rate method and the reducing balance method.

What is the Reducing Balance Method?

The reducing balance method is a highly fair system where interest is computed solely on your outstanding principal amount. As you pay down your loan, the base number used to calculate interest gets smaller.

For example, if you borrow money for a vehicle and pay off a portion in your first month, the bank will not charge interest on that paid portion again. They only look at what is left.

This means that even though your total monthly EMI stays exactly the same, the internal split shifts. The interest fee drops every month, and the amount going toward your vehicle ownership grows.

How it Differs from the Flat-Rate System

To truly appreciate a car loan emi calculator with reducing balance method, you must contrast it with a flat-rate loan system. The difference can impact your personal savings.

In a flat-rate loan, the bank calculates your interest fee on your original borrowing amount for the entire duration. They completely ignore the fact that you are paying them back month by month.

Even when you are in your very last year of payments and owe a tiny fraction of the debt, a flat rate still charges you interest as if you just drove the vehicle off the dealership lot today.

Step-by-Step Guide to Using a Reducing Balance Tool

Using an online financial tool is incredibly simple if you have the right details ready. Follow these steps to map out your auto financing.

Step 1: Input Your Desired Vehicle Loan Amount

Type in the exact amount of money you need to borrow after making your initial down payment at the vehicle dealership.

Step 2: Enter the Annual Interest Percentage

Input the exact rate the bank is offering you. Make sure the calculator is set to the reducing system rather than a flat scheme.

Step 3: Select Your Repayment Timeline

Choose how many months or years you want to take to return the money. Most vehicle financing ranges from 36 months to 84 months.

Step 4: Analyze Your Monthly Schedule

Press calculate to view your estimated EMI. Review the monthly breakdown table to watch your interest fee drop toward zero over time.

Why You Should Use a Digital Calculator Before Buying

Walking into a vehicle dealership without running the numbers first can put you at a massive disadvantage. Sales agents use complex terms to make loans sound cheaper than they are.

By using a car loan emi calculator with reducing balance method at home, you know your budget limits in advance. You will instantly spot if a lender is trying to overcharge you.

It also allows you to test out different down payment sizes. You can see exactly how much cash you save on monthly interest by paying a bit more upfront.

Real-World Example of a Reducing Balance Journey

Let us look at a simple example to see how this system behaves over time. Imagine you are financing a new compact vehicle with the following terms:

Total Borrowed Capital: 24,000 units

Annual Interest Rate: 6 percent

Loan Timeline: 4 Years (48 Months)

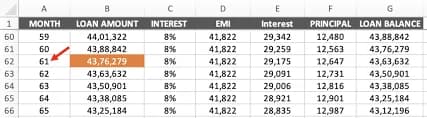

When you run these specific numbers through the reducing balance system, your fixed monthly payment comes out to exactly 563 units each month.

In your very first month, your interest fee is calculated on the full 24,000 units, costing you 120 units of interest. The remaining 443 units go toward lowering your vehicle debt.

By month 30, your outstanding debt has dropped significantly. Now, your monthly interest fee is only around 50 units, meaning a massive 513 units of your EMI goes directly toward wiping out your remaining debt.

How Your Loan Timeline Impacts Total Costs

When using a car loan emi calculator with reducing balance method, you will notice that the length of your loan plays a huge role in your total expenses.

Picking a short timeline, like three years, means your monthly payments will be quite high. However, because you pay down the main balance rapidly, your total interest cost will be tiny.

Picking a long timeline, like seven years, drops your monthly payment to a very comfortable level. The downside is that your principal balance stays large for a long time, allowing interest to accumulate.

Smart Strategies to Shorten Your Vehicle Debt

If you want to maximize the power of the reducing balance system, you can use these simple strategies to achieve financial freedom faster.

Make Periodic Extra Payments: Whenever you receive spare cash, pay down your principal balance. The reducing system will immediately lower your interest fee next month.

Pay an Honest Down Payment: Avoid zero-down financing options. Putting down solid cash at the start keeps your initial balance small and your interest costs low.

Keep Your Timeline Under Five Years: Try to avoid long auto loans. A shorter timeline ensures you do not end up owing more money than the vehicle is actually worth.

Conclusion

Mastering a car loan emi calculator with reducing balance method is one of the best ways to protect your personal finances when buying a vehicle. It ensures you know exactly how your money is being spent every month.

By choosing a loan that uses the reducing system, you ensure that your good payment habits are rewarded with lower interest fees over time. Always run the numbers yourself before signing any dealership contracts, compare multiple banking offers, and aim to pay off your debt early whenever possible to save the maximum amount of cash.

Frequently Asked Questions (FAQs)

1. How can I tell if a bank is offering me a flat rate or a reducing balance rate?

You must look at your loan agreement terms or ask the lender directly for an amortization schedule. If the interest charge is identical in month one and month forty, it is a flat-rate loan. If the interest amount drops every single month, it is a reducing balance loan.

2. Can I use a regular home loan calculator to check my reducing balance car loan?

Yes, you can use a standard home loan calculator because the underlying mathematical formula for a reducing balance system is exactly the same for both types of loans. You just need to adjust the loan amount and the timeline to match your vehicle details.

3. Does the reducing balance method apply to both used and new vehicle loans?

Yes, the reducing balance method can be applied to loans for both brand-new and pre-owned vehicles. However, lenders generally charge a slightly higher interest percentage for used vehicles because old cars carry a higher risk value for the bank.

4. What happens to my reducing balance calculation if I miss a monthly payment?

If you miss a monthly payment, your outstanding principal balance does not drop as planned. Because your balance remains high, the bank will calculate a higher interest fee for the next month, and they will likely add late payment penalties to your account.

5. Why do dealerships sometimes push flat-rate loans over reducing balance options?

Dealerships and certain finance companies sometimes promote flat-rate loans because they look cheaper on paper. A 5 percent flat rate sounds better than an 8 percent reducing rate, but because of how the math works, the flat rate can actually end up costing you more total money.

6. Can I change my car loan structure after I have already started making payments?

You cannot easily change the internal structure of your current loan once the contract is active. However, you can refinance your vehicle loan by moving it to a completely different bank that offers a reducing balance system at a better rate to pay off your old lender.