What are the main hidden costs when transferring a loan from an HFC to a bank?

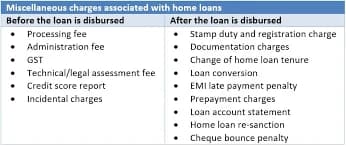

The major costs in a hidden charges checklist when switching home loans from housing finance companies to hfc banks include processing fees with Goods and Services Tax, legal appraisal costs, property technical valuation fees, and Memorandum of Deposit of Title Deed charges. Existing lenders might also levy high document retrieval or account statement processing fees.

Do housing finance companies charge foreclosure fees for home loan transfers?

Housing finance companies cannot charge foreclosure or prepayment penalties on floating-rate home loans held by individual borrowers. However, if the mortgage is locked under a fixed interest rate or borrowed under a non-individual entity structure, the existing housing finance company can legally levy foreclosure fees up to two and a half percent.

How does state-level stamp duty affect a home loan balance transfer?

State-level stamp duty affects a transfer through the mandatory registration of a new Memorandum of Deposit of Title Deed. When switching your debt to a commercial bank, the new banking institution requires a fresh mortgage registration, which incurs local statutory stamp fees and Central Registry of Securitisation Asset Reconstruction and Security Interest filing costs.

TITLE: Hidden Charges Checklist When Switching Home Loans from Housing Finance Companies to HFC Banks

Moving your active mortgage from a non-banking housing finance company to a major commercial retail bank is a popular way to grab lower interest rates. Traditional banks often look cheaper because their loan pricing links directly to the central bank's repo rate benchmarks.

However, a lower advertised interest rate does not automatically guarantee massive savings from day one. Shifting your structural debt setup involves closing out an old banking arrangement and initializing a fresh mortgage file from scratch with a new financial institution.

Reviewing a thorough hidden charges checklist when switching home loans from housing finance companies to hfc banks protects you from surprise financial blows. Uncovering these background transaction costs allows you to calculate the precise break-even timeline for your home loan refinancing venture.

The Upfront Expenses Levied by New Commercial Banks

When you approach a commercial bank to take over your home loan, they treat your application like a brand-new credit request. Even if you have a spotless repayment track record with your old lender, the incoming bank conducts independent validation checks.

The first major item on your hidden charges checklist when switching home loans from housing finance companies to hfc banks is the non-refundable processing fee. While some commercial banks run zero-processing-fee campaigns during festive months, standard fees typically range from a flat amount to half a percent of your total outstanding principal.

[Total Transfer Outlay]

│

├─► Processing & Administrative Fees (+18% GST)

├─► Legal Title Search & Technical Appraisal Costs

├─► State Stamp Duty & Local MODT Registration Fees

└─► Old Lender Document Retrieval & Statement Fees

Furthermore, banks hire independent third-party professionals to evaluate your home's physical structure and legal ownership papers. You must pay separate legal verification fees and technical appraisal charges to confirm the market value and clear title of the mortgaged property asset.

Understanding Background Costs from Existing Lenders

Your current housing finance company will not simply hand over your original property papers without collecting specific administrative dues. Refinancing professionals must prepare for exit costs that are often hidden deep within initial loan agreement fine print.

While regulatory laws prohibit exit penalties on standard floating-rate consumer loans, housing finance firms often charge high document retrieval fees. They also charge specialized fees for printing official lists of documents or issuing updated outstanding balance statements.

Tax Alert Note: Every administrative fee, conversion charge, and processing cost levied by both banks and housing finance corporations attracts a mandatory eighteen percent Goods and Services Tax that increases your total cash outgo.

Capital Protection Strategies for Premium Commercial Assets

Evaluating real transaction friction is highly important for investors managing high-value real estate assets. Refinancing properties leased to multinats requires matching upfront transfer friction against long-term operational cash inflows.

When handling properties leased to multinats, saving even a small fraction on interest rates yields massive compound savings across multi-lakh balances. However, if the property ownership is registered under a corporate shell structure, look out for heavy corporate foreclosure penalties that housing finance companies legally apply to non-individual accounts.

Financing Refinements for Fast-Growing Indian Enterprises

Indian entrepreneurs and corporate founders frequently refinance personal property assets to stream optimized capital into their main business operations. Analyzing your switching fee framework protects your working capital lines from accidental administrative depletion.

Preserving Runway for Startups India

Managing early-stage operational capital means founders at startups india must avoid sudden out-of-pocket cash requirements. Ensuring that the upfront fees on your hidden charges checklist when switching home loans from housing finance companies to hfc banks do not consume too much immediate cash flow preserves vital runway post venture rounds.

Optimizing Cash Management for Export Houses

Trading houses and export houses use home loan overdraft accounts to park fluctuating global revenues temporarily. Refinancing your underlying loan structure to a commercial bank opens up smoother international trade processing channels, provided the initial entry stamp duties do not neutralize your first-year interest savings.

Navigating Statutory Fees and Regulatory Clearances

Statutory levies are set by state governments and central authorities, meaning they cannot be waived or negotiated down by your banking officers. These government costs constitute a large chunk of the total expense incurred during a balance transfer.

Safeguarding Capital Across Verified Corporate Purchases

Refinancing residential real estate bought through verified corporate purchases demands absolute legal clarity. The incoming bank will order a fresh search of local sub-registrar records to verify that the property has no secondary claims, charging you legal fee outlays at actual market costs.

Maintaining Capital Stability Post Venture Rounds

Corporate executives scaling businesses through sequential venture rounds must ensure personal properties remain free of legal compliance bottlenecks. Registering a fresh mortgage deed with a commercial bank requires paying local stamp duty along with standard Central Registry of Securitisation Asset Reconstruction and Security Interest upload fees.

Checklist Cost Component | Type of Charge | Typical Cost Range / Pricing Rule | Impact on Refinancing Strategy |

New Processing Fee | Administrative Bank Fee | Flat fee of several thousand or up to 0.50% of loan | Out-of-pocket expense paid during submission |

Legal & Technical Fee | Third-Party Appraisal | Flat valuation cost per property asset | Paid to external inspectors for verification |

Stamp Duty & MODT | State Government Levy | Varies by state law (often 0.1% to 0.5% of loan) | Non-negotiable tax to validate the new mortgage |

Document List Fee | Old Lender Exit Charge | Flat fee per informational request packet | Paid to the HFC to secure your paper list |

CERSAI Registry Fee | Central Government Cost | Nominal statutory fee under a few hundred | Paid to register the new asset lien online |

Step-by-Step Action Plan to Verify Switching Costs

To ensure your balance transfer makes complete financial sense, execute this sequence to identify every fee before signing final takeover contracts.

1.Request Official Closing Documents:Phase 1.

Apply for a formal outstanding loan balance statement and an official list of documents held from your current housing finance company.

2.Collect the Bank's MITC Sheet:Phase 2.

Obtain the Most Important Terms and Conditions document from the incoming bank to isolate their specific legal, technical, and administrative processing fees.

3.Calculate State-Level Mortgage Taxes:Phase 3.

Check your local state government registration web portal to find the exact stamp duty rates required to execute a fresh Memorandum of Deposit of Title Deed.

4.Perform a True Break-Even Analysis:Phase 4.

Divide your total calculated switching expenses by your projected monthly EMI savings to see exactly how many months it takes to recover your upfront transfer outlays.

Conclusion

Working through a comprehensive hidden charges checklist when switching home loans from housing finance companies to hfc banks turns a guessing game into a predictable financial process. Refinancing can certainly lower your interest outgo, but only if your total switching expenses do not wipe out your short-term gains.

Whether you are a budget-conscious salaried professional or an elite investor managing high-value properties leased to multinats, monitoring small fee leaks protects your net worth. Isolating hidden processing fees, local stamp taxes, and old lender exit costs ensures you make an educated, highly profitable financial transition.

Frequently Asked Questions (FAQs)

1. Why do commercial banks charge legal and technical fees if my property was already approved by an HFC?

Commercial banks are strictly regulated institutions that must follow independent internal risk management guidelines. They cannot legally rely on the property valuation or legal title clearances performed by an outside housing finance company years ago. The incoming bank must send their own empanelled lawyers and technical engineers to verify that the property layout matches approved building plans and that no local land disputes have occurred since your original purchase.

2. Can the incoming commercial bank add my processing and stamp duty costs directly into my new home loan balance?

In many situations, if your current property valuation leaves a safe cushion relative to the total loan-to-value ratio, commercial banks can bundle these upfront refinancing charges directly into your main loan principal. This means you do not have to pay large amounts of out-of-pocket cash on day one. However, remember that funding your switching costs this way means you will pay compound interest on those administrative fees across your entire remaining loan tenure.

3. What is an MODT charge, and why must I pay it again during a home loan balance transfer?

MODT stands for Memorandum of Deposit of Title Deeds. This is a mandatory legal document that proves you willingly handed over your original property ownership papers to a financial institution as security for your loan balance. Because this document creates a legal link to a specific lender, your old housing finance company's MODT must be canceled upon closure, and a brand-new MODT must be drawn up and registered to validate your new commercial bank's legal claim on the property.

4. How can I protect my personal capital from hidden insurance cross-selling during a loan transfer?

Many commercial banks try to make home loan insurance or separate property insurance a mandatory condition for approving a balance transfer takeover. While protecting your family asset is a smart move, you are not legally required to buy insurance products directly from the lending bank. You have full freedom to compare options from independent insurance providers online, which can save you significant amounts of money compared to the bundled premium plans offered by branch managers.

5. What happens if my current housing finance company delays releasing my original property papers after the bank pays them?

According to central banking fair practices codes, lenders must release all original property title deeds and cancel active mortgage links within thirty days of receiving full final settlement clearance. If your housing finance company delays releasing your original files beyond this mandatory period without providing a valid legal explanation, they are required to pay you financial compensation for each day of administrative delay.