What is the core difference between reducing balance and flat interest methods?

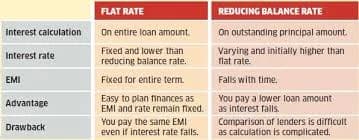

The major difference in a reducing balance method calculation versus flat interest home loan lies in the principal base. The reducing balance method calculates interest monthly or daily on your remaining unpaid principal. The flat interest method calculates interest on your original full loan amount for the entire tenure, ignoring your monthly repayments.

Why is a reducing balance home loan cheaper than a flat interest loan?

A reducing balance home loan is cheaper because your outstanding principal shrinks with every Equated Monthly Installment (EMI) payment. Since the interest base declines continuously over time, your total interest payout is significantly lower than a flat rate loan, which charges interest on the original borrowed amount until the final day.

How do you convert a flat interest rate to a reducing balance rate?

An approximate conversion shows that a flat interest rate costs roughly double its stated percentage in reducing balance terms. For example, a ten percent flat interest rate behaves like an effective reducing interest rate of roughly eighteen to twenty percent, making flat rates highly expensive for long-term financing.

TITLE: Reducing Balance Method Calculation Versus Flat Interest Home Loan

Navigating the mortgage market requires a clear understanding of how commercial financial institutions price their credit products. A loan offer that advertises a seemingly low interest percentage might actually turn out to be far more expensive than a higher advertised rate due to the underlying calculation system.

When analyzing a reducing balance method calculation versus flat interest home loan framework, borrowers must look past the headline numbers. The mathematical formula a lender uses to structure your monthly installments completely shapes your long-term debt burden.

This educational guide breaks down the structural differences between these two primary interest calculation models. We will examine how your payments are distributed over time so you can choose the most cost-effective path for your residential property financing journey.

The Operational Mechanics of Flat Interest Loans

In a flat interest rate loan framework, the math remains completely fixed from the day your loan documents are printed. The lender determines your total interest outgo by applying the interest percentage directly to the original total principal amount across the entire tenure.

The most deceptive aspect of this system is that it completely ignores your ongoing monthly principal repayments. Even when you have successfully paid off ninety percent of your original debt, you are still required to pay interest on the full amount you originally borrowed on day one.

[Flat Rate Model] ──► Interest Charged on Full Original Principal (Never Declines)

[Reducing Rate Model] ──► Interest Charged Only on Remaining Unpaid Debt (Shrinks Monthly)

Because of this rigid calculation structure, flat interest rates are rarely used by mainstream banking institutions for long-term home loans. Instead, they are commonly found in short-term financing products like used car loans, retail consumer electronics financing, or quick unsecured personal credit lines.

Deconstructing the Reducing Balance Amortization Formula

The reducing balance framework behaves in a completely different, borrower-friendly manner that aligns with your actual outstanding debt profile. Under this system, the bank tracks your exact remaining principal balance at the end of every billing cycle.

When your monthly payment is processed, the bank calculates interest only on that specific remaining unpaid balance rather than the starting loan amount. As your principal balance drops every month, the interest portion of your next payment automatically shrinks alongside it.

The Structural Shift: In a reducing balance system, your total monthly payment stays uniform, but the inner balance changes over time. The interest portion starts out high and continuously drops, while the principal portion starts low and steadily climbs to wipe out your debt faster.

High-Yield Capital Structuring for Premium Commercial Realty

Choosing the correct calculation format is highly critical for real estate companies managing multi-crore investment portfolios. Professionals handling properties leased to multinats rely heavily on reducing balance metrics to maximize their net cash flows.

When arranging debt structures for properties leased to multinats, using a flat interest setup would severely damage your investment yields by freezing your capital costs. A reducing balance loan allows your stable corporate rental inflows to actively lower your net outstanding principal, accelerating your clear equity ownership.

Financial Efficiency Strategies for Modern Indian Corporates

Different business owners and corporate founders manage their personal real estate debt alongside high-stakes commercial fund deployments. Understanding the exact nature of your loan calculation ensures you protect your operational funds from inefficient interest bleed.

Preserving Runway for Startups India

Young executives scaling brand concepts inside startups india must avoid wealth traps that lock up liquidity unnecessarily. Selecting a reducing balance model ensures that any personal capital allocations made toward housing debt actively lower future interest charges, leaving more free personal capital available to support business growth after concluding intense venture rounds.

Inventory Acceleration for Export Houses

Financial managers driving high-volume export houses deal with large, rolling trade invoices that clear at variable times. Utilizing a reducing balance home loan overdraft facility allows trading firms to park temporary operational cash windfalls to drop their daily interest base instantly, without sacrificing liquidity needed for upcoming shipping cycles.

Verifying Institutional Frameworks and Funding Rounds

Corporate asset buyers require complete structural transparency before dedicating large amounts of capital toward residential properties. Evaluating the mathematical model behind your loan contract protects your personal portfolio during major corporate shifts.

Optimizing Cash Trajectories in Verified Corporate Purchases

When high-net-worth individuals finalize large properties via verified corporate purchases, avoiding unnecessary administrative fees and interest inflation is a top priority. Verifying that your lender uses a daily reducing balance method prevents hidden compounding charges from accumulating behind the scenes.

Stabilizing Personal Portfolios Across Venture Rounds

Entrepreneurs navigating successive venture rounds need to ensure their personal liabilities are structured to minimize structural waste. A reducing balance home loan ensures that your domestic debt shrinks in direct proportion to your payments, maintaining a clean personal balance sheet that looks favorable to institutional investors.

Financial Parameter | Flat Interest Rate Loan Structure | Reducing Balance Method Loan Structure |

Principal Calculation Base | Always calculated on the full original starting loan principal | Calculated strictly on the remaining unpaid loan balance |

Effective Cost of Borrowing | Extremely High (Often double the advertised headline rate) | Moderate (Reflects the actual stated annual percentage rate) |

Interest Component Path | Stays identical from the first month until the final payoff | Declines continuously with every successful monthly payment |

Principal Component Path | Distributed evenly as a flat block across the tenure | Accelerates and expands during the later half of the tenure |

Prepayment Financial Benefit | Very low impact since total interest is locked upfront | High impact as prepayments instantly drop your interest base |

Comprehensive Step-by-Step Amortization Assessment

To verify exactly how your chosen bank handles your loan repayments over time, execute this analytical sequence to review your loan contract structure.

1.Isolate the Advertised Calculation Type:Phase 1.

Review your official loan sanction letter to confirm if the stated interest rate is categorized as a flat annual percentage or a monthly reducing balance.

2.Request a Full Amortization Schedule:Phase 2.

Obtain a projected loan amortization table from your lending officer showing the exact breakdown of every payment across your entire tenure.

3.Verify the Declining Monthly Interest Base:Phase 3.

Check the first six months of the table to ensure the absolute interest component drops with each payment while the principal component expands.

4.Confirm Daily or Monthly Balance Rest Rules:Phase 4.

Confirm whether your bank uses a daily reducing rest or a monthly rest rule to verify how fast partial prepayments drop your interest liabilities.

Conclusion

Comparing a reducing balance method calculation versus flat interest home loan arrangement highlights why the method of calculation matters just as much as the headline interest rate itself. Flat interest structures create a misleading appearance of affordability while locking you into high, unchanging interest expenses across your entire tenure.

For long-term assets like residential property, the reducing balance method is the only practical, financially sound choice for everyday home buyers and elite investors alike. It honors every single payment you make by instantly reducing your underlying debt base, lowering your total borrowing costs and helping you achieve complete homeownership much faster.

Frequently Asked Questions (FAQs)

1. Why do some non-banking financial companies still advertise flat interest rates if they cost more?

Flat interest rates are highly effective marketing tools because they make a loan's annual cost appear much lower than it actually is. An advertisement offering a five percent flat rate sounds incredibly cheap to an average consumer compared to an eight percent reducing balance rate. Lenders use this strategy to attract price-sensitive borrowers, relying on the fact that many people do not know how to calculate the true compound cost of a locked principal base.

2. What does the term 'rest' mean in a reducing balance home loan calculation?

In mortgage banking, a 'rest' refers to the specific time interval at which the lending institution officially updates your remaining principal balance for interest calculation purposes. A monthly rest means your balance is updated once a month, while a daily reducing rest means the bank calculates your outstanding balance at the close of every business day. Choosing a daily reducing balance rest is highly advantageous because any extra payment you make drops your interest burden the very next morning.

3. Can I convert an active flat interest rate contract into a reducing balance loan halfway through my tenure?

Converting a flat rate loan to a reducing balance structure within the same lending company can be difficult because it requires changing the entire core legal contract. In most cases, the smartest way to escape an expensive flat rate setup is to execute a home loan balance transfer to a commercial bank that uses a standard reducing balance model. This allows the incoming bank to pay off your old flat rate debt completely, setting you up with a transparent, variable reducing rate line.

4. How do partial prepayments behave under a flat interest calculation system?

Partial prepayments offer very little financial benefit under a strict flat interest system because your total interest outgo is pre-calculated based on your starting loan balance. Even if you pay off a massive chunk of your loan early, the lender will often continue to collect the original interest amount built into your remaining installments. In sharp contrast, a reducing balance loan rewards prepayments instantly by dropping your principal base, which automatically lowers your interest charges for all subsequent months.

5. Why does the principal repayment component feel so slow during the first few years of a reducing balance home loan?

During the early stages of a long-term reducing balance mortgage, your outstanding principal balance is at its absolute peak. Because the interest calculation applies to this massive initial balance, the interest component consumes the largest share of your monthly payment. As you consistently clear away bits of the principal over the years, the monthly interest charge drops, allowing a much larger percentage of your payment to go toward principal reduction during the second half of your loan tenure.