Managing credit limits or securing business funding requires following precise loan rules. In the modern financial market, companies and families track a wide variety of credit channels. This includes coordinating verified corporate purchases for young tech startups, organizing large venture capital rounds, and overseeing premium commercial real estate properties leased to multinats or busy global export houses.

Historically, banks treated individual retail consumers and large corporate entities very differently when a default occurred. Large corporations could often negotiate minor penalties, while individual borrowers faced heavy, compounding interest rate adjustments. To fix this imbalance, central banking guidelines mandate a strict uniform penal charges implementation across individual and non individual product lines, completely transforming how defaults are penalized across the country.

This student-friendly guide explains the legal requirements for penalty parity, details how the non-discriminatory framework protects your accounts, and shows how uniform credit systems protect both small retail savers and massive business houses.

What is the uniform penal charges implementation across individual and non individual product lines?

It is a mandatory banking compliance rule established under fair lending guidelines. It requires commercial lenders to implement a standardized, non-discriminatory penalty scale for all accounts. The rule ensures that the penalty rates applied to individual borrowers for non-business purposes can never be higher than the penalty rates applied to corporate businesses for identical contract violations.

How does the uniform penalty rule protect retail consumers from unfair fees?

The rule creates a natural legal ceiling for individual late fees by linking retail penalties directly to business credit guidelines. Because banks cannot charge retail borrowers higher penalty rates than what they apply to commercial enterprises within the same product tier, individual consumers are protected from arbitrary, excessive fee structures.

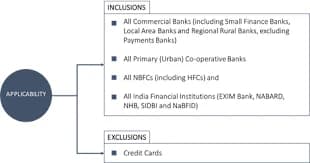

Does the uniform penal charges rule permit any product exceptions?

Yes, the central bank explicitly excludes specific debt instruments from the uniform penalty framework. The non-discriminatory guidelines do not apply to revolving credit card accounts, external commercial borrowings (ECBs), global trade finance credits, or complex corporate derivative contracts, which continue to follow separate product rules.

Technical Pillars of the Uniform Penalty Regime

Every public sector and private commercial bank must align its lending frameworks with three major legal pillars to satisfy national audit teams.

These operational rules ensure that your default statement logs display complete clarity from the second an applicant enters the banking system.

The Principle of Proportionality: The master policy document must prove that any applied fee matches the actual scale of the breach, rather than acting as an arbitrary profit-generating tool for the branch.

Absolute Ban on Capitalization: Lenders are strictly prohibited from adding outstanding late fees to your primary loan principal balance. This rule stops banks from calculating compounding interest on top of penalties.

Mandated Fee Disclosures: Lenders must detail all potential penalties explicitly inside the Key Fact Statement (KFS) and display them openly on their public digital portals under the "Interest Rates and Service Charges" tabs.

How Parity Works Across Shared Credit Products

To understand how the uniform penal charges implementation across individual and non individual product lines works in practice, let's look at how a shared credit product, such as a property-backed overdraft line, handles different borrowers.

If a commercial bank structures a specific property loan pool, the penalty rules must apply equally across all business entities and retail applicants.

Case A: The Small Retail Consumer

An individual borrower draws cash from a home overdraft account to cover a sudden medical emergency. If they miss an installment, the bank applies a standardized penalty fee—for example, a flat 2% per annum on the default amount.

Case B: The Corporate Enterprise

A major tech startup draws cash from an identical property-backed overdraft line to fund local software engineer payrolls. If their account faces a technical bounce, the system applies the exact same 2% per annum penalty calculation used for the retail consumer.

By forcing the bank to use an identical calculation grid for both profiles, the law guarantees that the individual consumer receives the exact same fair fee protections enjoyed by large, well-funded corporate entities.

Step-by-Step Guide to Verify Your Uniform Penalty Protections

Exporters, startup founders, and retail savers can verify that their bank follows these uniform penalty rules by performing a quick audit of their loan profiles.

Step 1: Request Your Detailed Product Key Fact Statement

When opening a new credit line or renewing an old business limit, ask your relationship team for a comprehensive Key Fact Statement. Verify that the penalty metrics are listed clearly as absolute amounts or simple annual percentages.

Step 2: Compare Retail and Business Penalty Tables

Log into your bank's public website and open the master service charges directory. Compare the default penalty tables listed for individual home loans with the penalty charts written for commercial business loans.

Step 3: Check for Hidden Interest Rate Premium Triggers

Ensure the bank has not snuck in hidden interest rate increases under alternative names, like "risk premium adjustments," during a minor documentation delay. Any penalty for contract non-compliance must be treated as an isolated, flat penal charge.

Step 4: Verify the GST Calculation Entries

Examine your monthly statement after a technical default occurs. Ensure any applied Goods and Services Tax (GST) is calculated strictly over the isolated penal fee, keeping your core principal pool free from extra tax loops.

Conclusion: A Progressive Milestone for Fair Lending Practices

The introduction of the uniform penal charges implementation across individual and non individual product lines framework marks a highly positive evolution in national financial consumer protection. It ensures that credit penalties are used strictly to encourage financial discipline rather than acting as a hidden revenue tool for commercial lenders.

By understanding your consumer protection rights under these guidelines, inspecting your monthly loan statements regularly, and maintaining open communication with your lender's compliance desk, you can confidently navigate short-term cash flow hurdles while keeping your capital base secure, healthy, and fair.

Frequently Asked Questions

Can a commercial bank waive a penalty for a business client while refusing a retail client?

While banks hold the legal right to waive penalties under exceptional circumstances, their master board policies must remain fair. If a bank provides systematic fee waivers to corporate accounts while enforcing rigid penalties on retail consumers for identical defaults, it represents a major compliance violation.

Does the uniform penalty rule mean that all bank loans must carry the exact same late fee?

No. The rule does not state that a small personal loan and a massive corporate machinery loan must carry identical flat fees. It requires that within a single, specific loan category (like vehicle loans or property loans), the penalty rate structure must remain non-discriminatory across all individual and corporate profiles.

What should I do if my bank statement shows a retail penalty rate that is higher than the corporate rate?

If you spot a discriminatory penalty setup on your account statement, file a formal complaint with the bank's internal grievance desk. If the branch fails to fix the software error within thirty days, you can escalate the file straight to the central RBI Banking Ombudsman portal.

Are regular overdue interest calculations covered under this uniform parity rule?

No. Regular overdue interest is the standard contracted interest rate calculated on any money you fail to pay back past a due date to cover the extra time you held the funds. This is a regular commercial cost and sits entirely outside the punitive penal charge rules.

Can a bank charge additional penalty fees if an electronic NACH transaction bounces?

A bank can apply a standard bounce fee to cover the actual network processing costs of the failed transaction. However, the policy must ensure this charge is applied only once per monthly installment run, and cannot be multiplied through quick, repeated automated retries.

Does this uniform protection continue to apply if a loan becomes a Non-Performing Asset?

Yes, absolutely. Even if a business or individual faces severe financial hurdles and the loan account drops into a Non-Performing Asset (NPA) category, the commercial bank is legally bound by fair lending rules, meaning they can never calculate compounding interest on top of accumulated penal charges.v