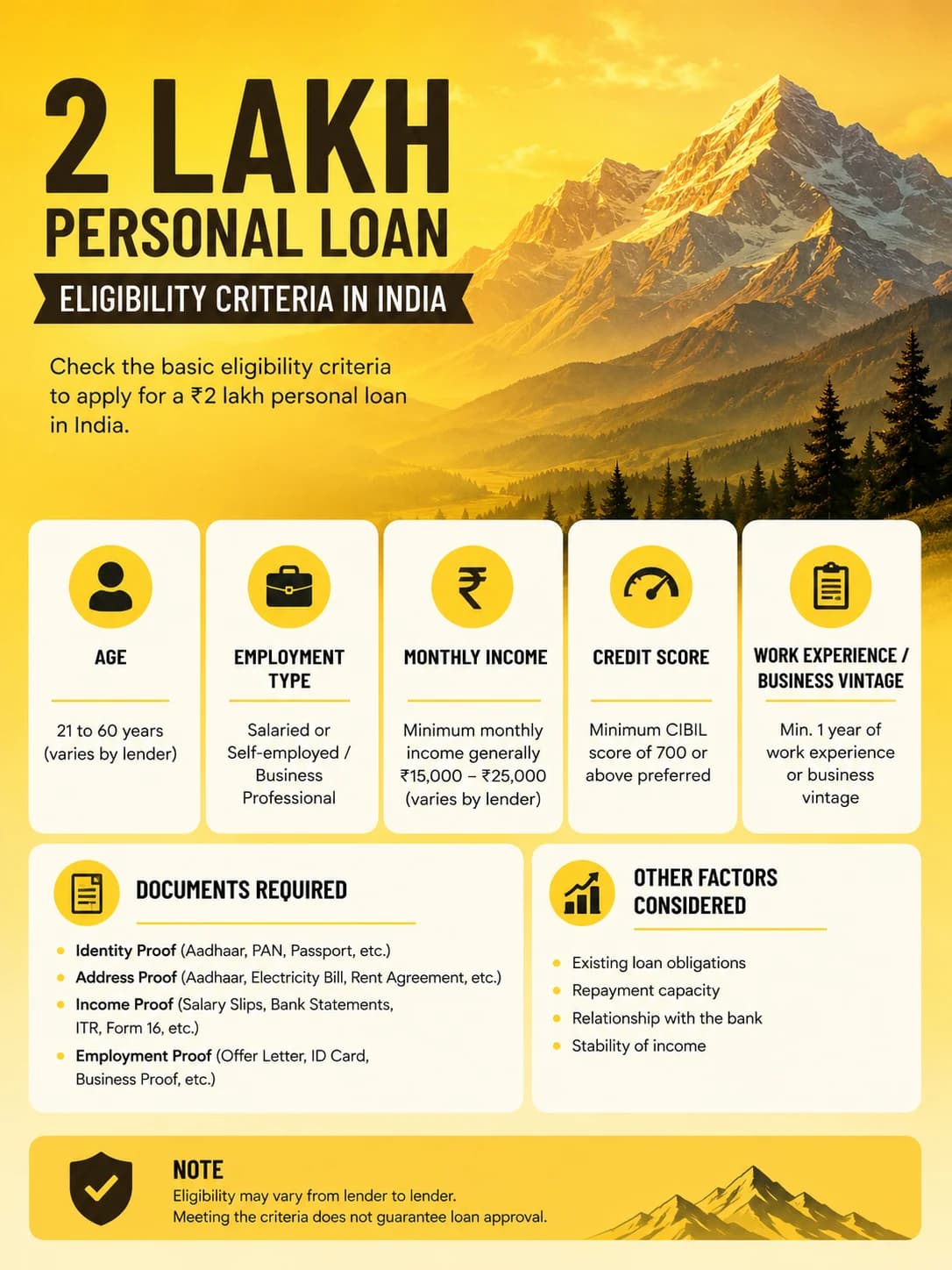

What is the basic eligibility for a 2 Lakh personal loan in India?

To meet the 2 lakh personal loan eligibility criteria India, you must be an Indian citizen aged between 21 and 60 years. You need a regular monthly income of at least ₹15,000 to ₹25,000, a stable job, and a healthy CIBIL score above 700.

What is the minimum salary required for a 2 Lakh personal loan?

The minimum salary required for a ₹2,00,000 personal loan generally ranges between ₹15,000 and ₹25,000 per month. Lenders in metro cities like Mumbai or Delhi often require a higher minimum income compared to non-metro cities due to the higher cost of living.

Can I get a 2 Lakh personal loan with a low CIBIL score?

Getting a ₹2,00,000 personal loan with a CIBIL score below 650 is difficult. Most top lenders require a score of 700 or higher. If your score is low, you may face rejection or be charged a much higher interest rate by non-banking financial companies (NBFCs).

Understanding the 2 Lakh Personal Loan Eligibility Criteria India

Lenders use eligibility criteria to calculate the risk of lending money. Because personal loans do not require security, banks want to be 100% sure you can pay them back.

Meeting these criteria keeps your application safe from rejection. Every rejection drops your credit score, making it harder to borrow money in the future.

Let us look closely at the main pillars that decide your eligibility for a ₹2,00,000 loan.

1. Age Restrictions

Your age tells the bank how many working years you have left to repay the debt.

Minimum Age: You must be at least 21 years old when applying.

Maximum Age: You should not be older than 60 to 65 years at the time of loan completion.

2. Employment Status and Stability

Lenders want to see a steady source of income. Erratic income streams increase the chance of missed payments.

Salaried Individuals: You should work with a registered private company, public sector undertaking (PSU), or government body.

Self-Employed Individuals: You must own a registered business, shop, or work as a certified professional like a doctor or CA.

Job Continuity: Most banks ask for at least 1 year of total work experience, with at least 6 months spent at your current employer.

3. Minimum Monthly Income

Your income is the most important factor for an unsecured loan. It determines if you can comfortably afford the monthly EMIs.

For salaried individuals, the absolute minimum income is usually ₹15,000 per month.

If you live in major tier-1 cities, banks like HDFC, ICICI, or SBI might ask for a minimum of ₹20,000 or ₹25,000.

For business owners, your annual net income reflected in your Income Tax Returns (ITR) should be at least ₹2.5 lakhs to ₹3 lakhs.

4. Credit Score (CIBIL Score)

Your CIBIL score is a three-digit summary of your past credit behavior. It shows how responsibly you have handled credit cards and previous loans.

A score of 750 or above is considered excellent. It gets you fast approval and lower interest rates.

A score between 700 and 749 is good and easily meets the 2 lakh personal loan eligibility criteria India.

Scores below 650 make you a high-risk borrower, leading to direct rejections.

Income vs Loan Multiplier: How Banks Decide the Amount

Banks do not just look at your flat salary; they look at your Fixed Obligation to Income Ratio (FOIR). This ratio shows how much of your monthly income already goes into paying existing rents or EMIs.

Ideally, your total monthly debt payments—including the new loan EMI—should not cross 45% to 50% of your take-home pay.

For a ₹2,00,000 loan with a 3-year tenure at a 12% interest rate, your monthly EMI will be roughly ₹6,643. If your monthly income is ₹20,000 and you have no other loans, you can easily afford this EMI.

Documents Required to Prove Eligibility

Meeting the criteria is only half the battle. You must prove it to the lender using valid, government-approved documents. Keep these files scanned and ready before applying online.

For Salaried Employees

Identity Proof: PAN Card, Aadhaar Card, Passport, or Voter ID.

Address Proof: Utility bills (electricity/water), Aadhaar Card, or Rent Agreement.

Income Proof: Salary slips for the last 3 months.

Bank Statements: Bank account statements for the past 6 months showing your salary credits.

Tax Proof: Form 16 or Income Tax Returns for the last 1 to 2 years.

For Self-Employed Individuals

Identity and Address Proof: PAN Card, Aadhaar Card, and Passport.

Business Proof: GST registration certificate, shop establishment license, or trade license.

Income Proof: Income Tax Returns (ITR) for the last 2 years along with computation of income.

Financial Statements: Audited Balance Sheet and Profit & Loss statement.

Bank Statements: Current account statements for the last 6 months.

Step-by-Step Guide to Apply for a 2 Lakh Personal Loan

If you satisfy all the eligibility terms, the application process is quick and simple. Follow these steps to ensure smooth processing:

Step 1: Calculate Your EMI

Use an online personal loan EMI calculator. Input ₹2,00,000 as the principal amount, pick a comfortable tenure (1 to 5 years), and check the expected monthly payout.

Step 2: Compare Lenders Online

Do not apply at the very first bank you see. Compare interest rates, processing fees, and pre-closure charges across major banks and fintech lenders.

Step 3: Check Eligibility Digitally

Visit the chosen bank's portal. Most lenders have a quick pre-eligibility tool where you enter your mobile number, PAN, and monthly income to see if you qualify instantly.

Step 4: Fill the Application and Upload Papers

Complete the online application form with accurate personal and professional details. Upload clean, readable copies of your KYC papers, salary slips, and bank statements.

Step 5: Verification and Disbursal

The bank will verify your documents. They might call you or your employer for confirmation. Once verified, the loan agreement is signed digitally, and the money enters your bank account within a few hours.

Tips to Improve Your Eligibility for a 2 Lakh Loan

If you find your current profile falling slightly short of the required benchmarks, do not lose hope. You can take active steps to boost your eligibility before applying.

Clear Existing Debts: Pay off small outstanding debts or credit card dues. Lowering your current debt burden immediately improves your FOIR.

Check Your Credit Report for Errors: Sometimes, banks make mistakes and report paid loans as active. Check your free annual CIBIL report and dispute any errors immediately.

Avoid Multiple Simultaneous Applications: Applying to four banks at the same time signals financial distress. Lenders view this as "credit hungry" behavior and may reject you.

Add a Co-applicant: If your income is low or your credit score is weak, consider adding a family member with a stable income and a high CIBIL score as a co-applicant.

Conclusion

Securing a ₹2,00,000 loan is stress-free if you understand and match the 2 lakh personal loan eligibility criteria India. Focus on keeping your credit score above 700, maintain job stability, and ensure your income can easily absorb the new monthly EMI.

Borrow responsibly and only take what you truly need. A personal loan can be an excellent financial tool when managed with discipline.

Frequently Asked Questions (FAQs)

Q1. Can a college student apply for a 2 Lakh personal loan in India?

No, regular college students usually do not qualify for a personal loan because they lack a steady, regular monthly income source. To meet the eligibility criteria, you must be earning a regular salary or running a registered business. Students looking for funds should explore specialized education loans instead.

Q2. What happens to my loan eligibility if I switch jobs frequently?

Frequent job changes can hurt your loan eligibility. Lenders view frequent shifts as a sign of employment instability. Most top banks require you to have at least 6 continuous months of employment with your current employer and 1 full year of total work experience before approving a loan.

Q3. Does a higher processing fee mean easier loan approval?

No, a higher processing fee does not guarantee loan approval. Processing fees cover the administrative costs of evaluating your application. Your approval depends entirely on your credit score, income levels, job stability, and your ability to meet the primary eligibility terms set by the bank.

Q4. Can I get a 2 Lakh personal loan if I receive my salary in cash?

It is highly difficult to get an unsecured personal loan if your salary is paid in cash. Lenders require official proof of income via bank transfers or cheques to verify your earnings. Without direct salary credits reflecting in a 6-month bank statement, traditional banks will likely reject your request.

Q5. How long does it take for a 2 Lakh personal loan to hit my account?

If you satisfy all the eligibility terms and submit valid online documents, many modern lenders can approve and disburse the money within a few hours. Traditional banks taking manual physical documents may take anywhere between 2 to 7 working days to complete the background checks.

Q6. Will checking my eligibility on multiple websites lower my CIBIL score?

Checking your basic eligibility through soft searches on online comparison portals does not hurt your score. However, filling out official, complete loan applications on multiple bank websites triggers "hard inquiries." Multiple hard inquiries within a short period will lower your credit score.