What is the monthly EMI for a 2 lakh personal loan for 2 years?

The monthly EMI for a 2 lakh personal loan for 2 years generally ranges between INR 9,200 and INR 10,200. The exact amount depends entirely on the interest rate levied by your bank. Lower interest rates result in smaller EMIs, while higher interest rates increase your monthly payout.

How does the interest rate impact a 2 lakh loan for 2 years?

The interest rate determines the total cost of your borrowing. For a 2 lakh loan over 2 years, a 10.5% interest rate results in an EMI of about INR 9,281. If the rate jumps to 15%, your monthly EMI increases to approximately INR 9,697, raising your total interest paid.

Can I get a 2 lakh personal loan for 2 years with a low salary?

Yes, you can get a 2 lakh loan if you meet the minimum salary criteria of the lender, which usually starts around INR 15,000 to INR 25,000 per month. Lenders will also evaluate your credit score and existing debts to ensure you can comfortably manage the EMI.

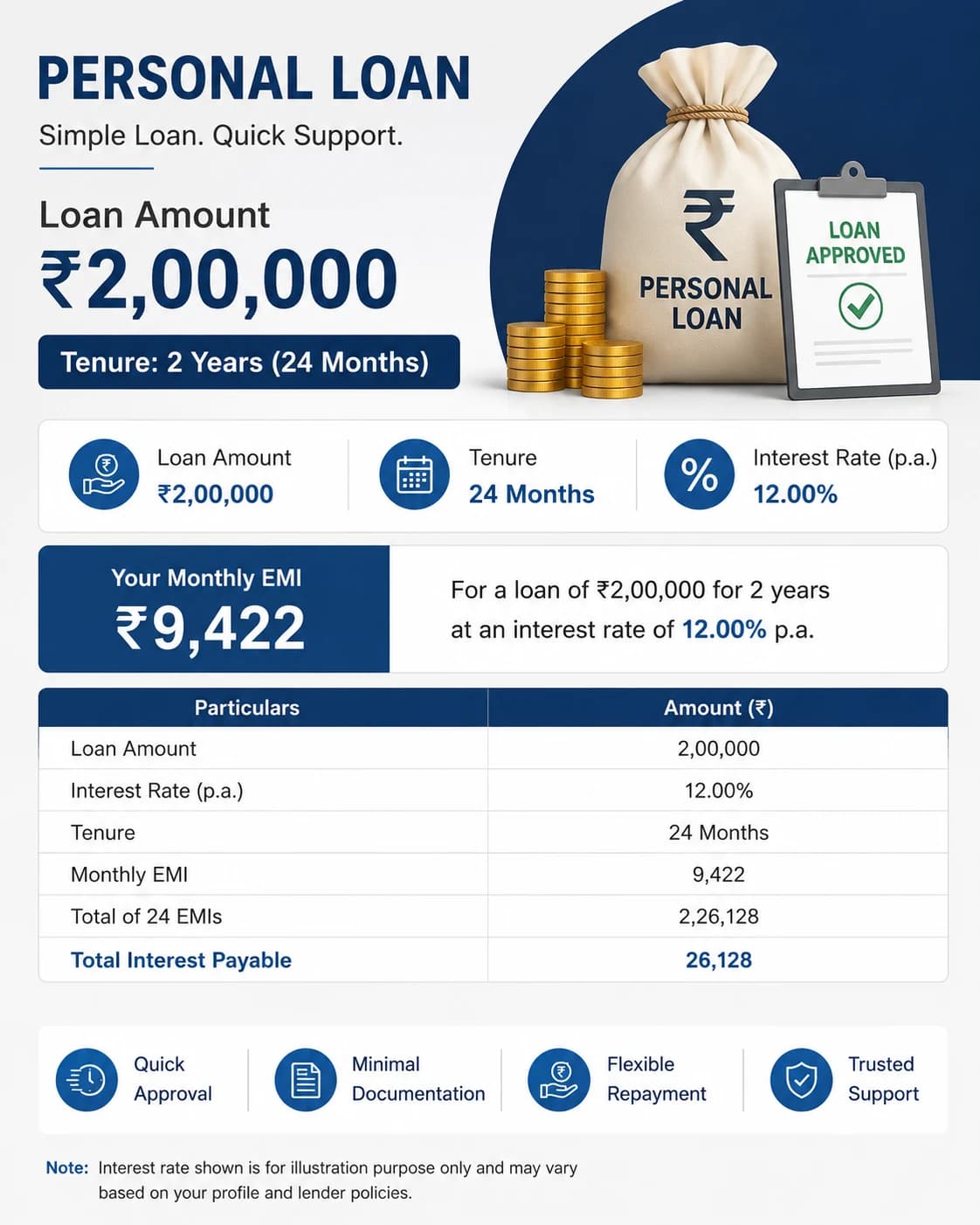

Understanding a 2 Lakh Personal Loan EMI for 2 Years

When you borrow a personal loan of 2 lakhs for a tenure of 2 years (24 months), you agree to pay it back in equal monthly installments. This installment is called an Equated Monthly Installment, or EMI.

Every single EMI you pay consists of two parts. The first part goes toward paying off the actual principal amount you borrowed. The second part covers the interest charged by the bank or financial institution.

In the initial months of your loan, a larger portion of your EMI goes toward covering the interest. As time passes and the principal reduces, more of your money goes toward clearing the actual loan amount.

How is Personal Loan EMI Calculated?

To understand how your 2 lakh personal loan EMI for 2 years is calculated, you can look at the standard mathematical formula used by banks.

The formula used for calculating EMIs is:

EMI=(1+r)n−1P×r×(1+r)n

Where:

P stands for the Principal loan amount (which is 2,00,000).

r stands for the monthly interest rate (annual interest rate divided by 12, then divided by 100).

n stands for the total number of monthly installments (which is 24 months for 2 years).

While you can calculate this manually, it is much easier and faster to use an online personal loan EMI calculator. You simply input the amount, tenure, and rate to see your monthly budget instantly.

Impact of Different Interest Rates on a 2 Lakh Loan

Interest rates vary wildly across different banks, non-banking financial companies (NBFCs), and digital lending platforms. Your credit history usually determines the rate you receive.

Let us look at a breakdown of how different interest rates change your 2 lakh personal loan EMI for 2 years and the total interest you will end up paying.

Interest Rate (p.a.) | Monthly EMI (INR) | Total Interest Payable (INR) | Total Repayment Amount (INR) |

|---|---|---|---|

10.50% | 9,281 | 22,744 | 2,22,744 |

12.00% | 9,415 | 25,953 | 2,25,953 |

13.50% | 9,551 | 29,216 | 2,29,216 |

15.00% | 9,697 | 32,728 | 2,32,728 |

18.00% | 9,964 | 39,143 | 2,39,143 |

As you can see from the data, even a small percentage change in the interest rate can alter your monthly budget and increase the total cost of the loan over 24 months.

Key Factors That Influence Your Personal Loan EMI

Lenders do not offer the same interest rate to every borrower. Several critical factors determine the exact interest rate and final EMI you will receive for your loan.

1. Your Credit Score

Your credit score is a reflection of your past financial discipline. Lenders view a score above 750 as excellent, which helps you qualify for the lowest possible interest rates.

2. Monthly Income Levels

Lenders want to make sure you earn enough money to afford the monthly repayments. Higher income levels give banks confidence that you will not default on your 2 lakh personal loan EMI for 2 years.

3. Employment Stability

Having a steady job with a reputable private company or a government organization works heavily in your favor. Lenders prefer applicants who have a secure, predictable source of monthly income.

4. Existing Debt Obligations

If you are already paying off multiple credit card bills or other loans, lenders might hesitate to give you more credit. They look at your Debt-to-Income ratio to ensure you are not over-leveraged.

Eligibility Criteria for a 2 Lakh Personal Loan

Before applying for a 2 lakh personal loan, you need to check if you satisfy the basic eligibility benchmarks set by top Indian lenders.

Age Limits: You should generally be between 21 years and 60 years old at the time of loan application.

Employment Profile: You must be a salaried employee or a self-employed individual with a steady business turnover.

Income Minimums: Most banks require a minimum monthly net take-home salary of INR 15,000 to INR 25,000, depending on the city you live in.

Work Experience: Salaried individuals typically need at least 1 to 2 years of total work experience, with at least 6 months at their current employer.

Documentation Required for Loan Approval

To speed up the processing of your personal loan, keep your KYC and income documents ready. Most lenders offer digital verification for faster approvals.

Proof of Identity: PAN Card, Aadhaar Card, Passport, or Voter ID.

Proof of Address: Aadhaar Card, utility bills, or rent agreement.

Income Verification: Salary slips for the last 3 months and bank statements for the last 6 months showing salary credits.

Business Proof: For self-employed individuals, IT returns for the last 2 years and business registration certificates.

Hidden Charges to Watch Out For

The interest rate is not the only cost associated with a personal loan. You must read the fine print to understand the additional fees that can affect your total out-of-pocket expenses.

Processing Fees

Lenders charge a one-time fee to process your loan application. This fee usually ranges from 1% to 3% of the total loan amount and is deducted directly from the disbursed amount.

Preclosure and Foreclosure Charges

If you receive a bonus or extra money, you might want to pay off your 2 lakh personal loan before the 2 years are up. Many banks charge a penalty fee of 2% to 5% on the remaining principal for early closure.

Late Payment Charges

Missing your EMI due date can cost you dearly. Lenders charge flat penal interest or a fixed fee for delayed payments, which can also severely damage your credit score.

Tips to Reduce Your Monthly Personal Loan EMI

If you want to keep your 2 lakh personal loan EMI for 2 years as low as possible, apply these practical financial strategies before submitting your application.

Improve Your Credit Profile: Take a few months to clear outstanding credit card dues and rectify any errors on your credit report before applying.

Compare Lenders Online: Do not accept the very first offer you receive. Use online comparison portals to evaluate interest rates and processing fees across different banks.

Negotiate with Your Existing Bank: If you have a long-standing savings account or a salary account with a specific bank, ask them for a special concessional rate.

Avoid Multiple Applications: Applying to several lenders at the same time can make you look credit-hungry, which drops your credit score and pushes interest rates higher.

Conclusion

Securing a 2 lakh personal loan EMI for 2 years is an effective way to meet immediate financial shortfalls without stretching your liabilities over many years. A 24-month tenure gives you the perfect middle ground: the EMIs remain affordable, and you become completely debt-free relatively quickly.

Always use an online personal loan EMI calculator to map out your monthly expenses before committing to a loan. By maintaining a clean credit score and comparing multiple lenders, you can secure an interest rate that keeps your finances stress-free.

Frequently Asked Questions

1. What will be the exact EMI for a 2 lakh personal loan for 2 years?

The exact EMI depends entirely on the interest rate your lender charges you. For instance, at a competitive rate of 10.5%, your monthly EMI will be INR 9,281. If your interest rate is higher, say 15%, the EMI will increase to INR 9,697 per month.

2. Can I repay my 2 lakh personal loan before the 2-year tenure ends?

Yes, most banks and financial institutions allow you to foreclosure or pre-close your loan before the 24 months are up. However, many lenders charge a foreclosure fee ranging between 2% and 5% of your remaining principal amount, so check the terms beforehand.

3. What happens if I miss my 2 lakh personal loan monthly EMI?

Missing an EMI results in late payment charges and additional penal interest added to your account. More importantly, a missed payment is reported to credit bureaus like CIBIL, which will drop your credit score and make borrowing harder in the future.

4. Is a 2-year tenure better than a 5-year tenure for a 2 lakh loan?

A 2-year tenure is generally better if you can afford the higher monthly payments because you will pay significantly less total interest. A 5-year tenure reduces your monthly EMI amount, but it extends your debt timeline and costs you much more in interest.

5. Does a processing fee get added to my monthly EMI?

No, the processing fee is usually a one-time charge that is deducted upfront from your total loan amount during disbursement. For example, if your processing fee is INR 2,000, the bank will transfer INR 1,98,000 to your account, but your EMI will still be calculated on the full 2 lakhs.