What are the basic personal loan documents required? To apply for a personal loan, most lenders require three main categories of paperwork: Proof of Identity (Aadhaar, Passport), Proof of Address (Utility bills, Voter ID), and Proof of Income. Salaried employees usually need 3 months of payslips, while self-employed individuals must provide Income Tax Returns (ITR) and bank statements.

What income proof is needed for a personal loan? For salaried workers, the primary income proof includes the last three to six months of salary slips and a bank statement showing salary credits. For self-employed applicants, lenders require the last two years of ITR, a Profit and Loss statement, and a six-month business bank account statement to verify earnings.

Can I get a personal loan without a salary slip? Yes, it is possible but more difficult. If you don't have a salary slip, you can provide your ITR filings, Form 16, or a certified bank statement showing a steady flow of income. Freelancers and business owners typically use these documents instead of traditional payslips to prove their financial stability.

Understanding Why Documents Matter

When you ask a bank for money, they take a risk. They want to be 100 percent sure that you are who you say you are and that you have a steady income.

The personal loan documents required serve as your financial "resume." If your papers are organized and authentic, your loan is likely to be approved much faster.

The Role of KYC

KYC stands for "Know Your Customer." It is a mandatory process where banks verify your identity. Without KYC, no legal lender can process your application.

The Role of Credit Scores

While not a physical "document" you carry, your credit report is a digital document lenders pull. It shows your history of paying back debts on time.

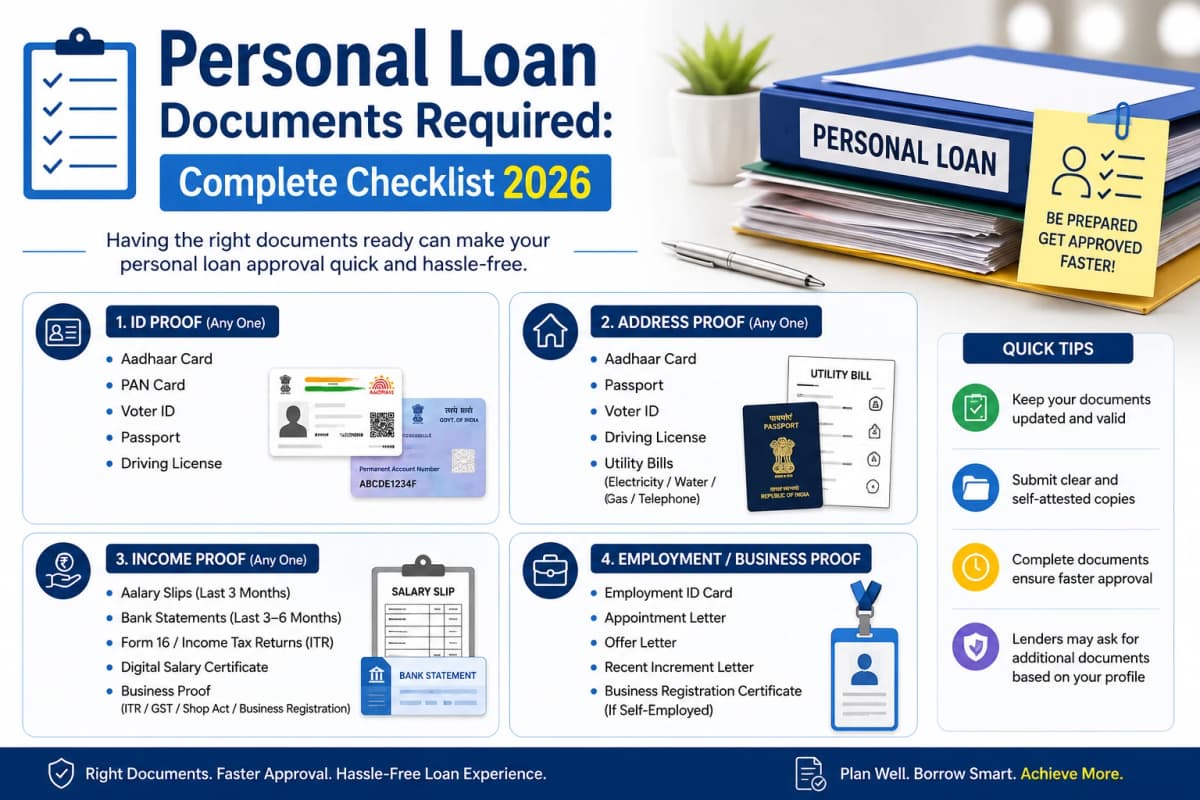

Category 1: Mandatory Identity and Address Proof

Regardless of your job, everyone must provide these basic personal loan documents required by law. These prove your existence and where you live.

Identity Proof (Choose one)

Aadhaar Card: The most preferred document in India for digital verification.

PAN Card: Mandatory for financial transactions and checking your credit score.

Passport: A strong proof of identity and nationality.

Voter ID: A valid government-issued photo ID.

Driving License: Must be valid and not expired.

Address Proof (Choose one)

Aadhaar Card: Works for both identity and address.

Utility Bills: Electricity, water, or gas bills (not older than 3 months).

Rent Agreement: Must be registered if you are living in a rented house.

Bank Passbook: The front page showing your current home address.

Category 2: Personal Loan Documents Required for Salaried Individuals

If you work for a company and receive a monthly salary, your documentation is usually the simplest. Lenders love salaried employees because of the predictable income.

Income Proof for Salaried

Salary Slips: Most banks ask for the last 3 to 6 months of payslips.

Bank Statements: You need to show the last 6 months of the account where your salary is deposited.

Form 16: This is a certificate issued by your employer showing the tax deducted from your salary.

Employment Certificate: Sometimes a letter from your HR or a copy of your employee ID card is needed.

Eligibility Criteria

Minimum age: Usually 21 years old.

Work experience: At least 1 to 2 years of total work history.

Minimum Salary: Often starts at 15,000 to 25,000 per month depending on the city.

Category 3: Personal Loan Documents Required for Self-Employed

If you run a shop, a clinic, or a startup, the bank needs to see that your business is healthy. The personal loan documents required for business owners focus on "stability."

Business and Income Proof

ITR Filings: You must show Income Tax Returns for the last 2 years.

Audit Reports: Balance sheets and Profit & Loss accounts certified by a CA.

Business Bank Statements: The last 6 to 12 months of your primary business account.

Business Proof: This includes your Trade License, GST Registration, or Shop Act License.

Office Address Proof

If your office is in a different location than your home, you must provide a separate address proof for the business premises, such as a lease or utility bill.

Category 4: Documents for Pensioners and Students

For Pensioners

Retired individuals can still get loans. They need to provide a Pension Payment Order (PPO) and bank statements showing the pension credit.

For Students

Students usually cannot get a personal loan alone because they lack income. They need a "co-applicant" (like a parent). The personal loan documents required would then focus on the parent's income.

Step-by-Step Process to Submit Your Documents

Knowing what is needed is only half the battle. You must also know how to present them to avoid rejection.

Step 1: Scan High-Quality Copies

If you are applying online, ensure your scans are clear. Blur or cut-off edges are the number one reason for technical rejection.

Step 2: Self-Attestation

If applying offline, you must sign every photocopy. This is called self-attestation and confirms that the copy is genuine.

Step 3: Check Expiry Dates

Ensure your Passport or Driving License hasn't expired. Banks will not accept documents that are past their valid date.

Common Mistakes to Avoid

Many people fail to get a loan not because they are poor, but because their paperwork is messy.

Mismatch in Names: If your name is spelled differently on your PAN and Aadhaar, fix it before applying.

Insufficient Bank Balance: If your bank statement shows many "bounced" payments or a zero balance, lenders will be scared.

Incomplete ITR: Ensure your ITR is fully processed and not just "submitted."

Tips to Speed Up Your Loan Approval

Apply Online: Digital applications using e-KYC (Aadhaar OTP) are processed much faster than physical ones.

Keep Originals Ready: Even if you submit copies, the bank officer might visit you to see the original documents.

Check Your Credit Score: Before applying, download your credit report. If there are errors, fix them first.

Consolidate Statements: If you use multiple bank accounts, provide statements for the one with the most activity and the highest balance.

Conclusion

Gathering the personal loan documents required is the most important step in your borrowing journey. By keeping your PAN, Aadhaar, salary slips, and bank statements ready, you reduce the stress of the application process.

Remember, honesty is the best policy. Never submit fake documents, as this can lead to permanent blacklisting by all banks. If your paperwork is honest and organized, you are well on your way to getting the funds you need.

Frequently Asked Questions (FAQs)

1. Is a PAN card mandatory for a personal loan?

Yes, a PAN card is mandatory for almost all personal loans in India. Lenders use it to track your financial history and pull your credit score from bureaus like CIBIL.

2. Can I use my Aadhaar card as both ID and address proof?

Yes, the Aadhaar card is a "dual-purpose" document. It contains your photo and your registered address, making it the most versatile personal loan document required.

3. What if my current address is different from the one on my ID?

If you have moved, you can provide a registered rent agreement or a recent utility bill (electricity/gas) in your name as valid proof of your current residence.

4. Do I need to provide a "Purpose of Loan" document?

Generally, no. Personal loans are "multi-purpose." Unlike a car loan, you don't usually need to provide a bill or invoice showing how you will spend the money.

5. How many months of bank statements are usually needed?

Most lenders ask for the last 6 months of bank statements. This helps them see your average balance and whether you have any existing EMI payments.

6. Can I get a loan with just an Aadhaar card?

While some "instant loan apps" claim to offer loans on Aadhaar alone, most reputable banks will still require a PAN card and some form of income proof to verify your repayment capacity.