Owning a permanent concrete home is a major dream for households across urban India. When you plan a modern, budget-friendly house construction, managing your interest overhead is the most important step.

The Government of India provides a massive financial relief window to lower and middle-income families through its flagship welfare program. Securing a 10 lakh home loan under PMAY subsidy allows first-time buyers to slash their borrowing costs drastically and achieve homeownership with total peace of mind.

Direct Answer Snippets for Quick Reference

Can I get a PMAY subsidy on a 10 lakh home loan?

Yes, you can secure a 10 lakh home loan under PMAY subsidy under the active PMAY Urban 2.0 framework. Eligible applicants receive a 4% interest subsidy on the first 8 lakh of their housing loan, which provides substantial savings on daily reducing loan balances.

What is the maximum subsidy amount for a 10 lakh loan?

The maximum interest subsidy benefit under the current scheme rules is 1.80 lakh. The central government releases this financial benefit to your bank account over five equal annual installments of 36,000 each, which directly reduces your outstanding loan principal.

Who is eligible for the PMAY Urban 2.0 subsidy?

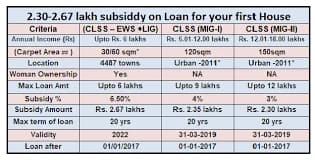

To qualify, the applicant's household must not own a permanent brick house anywhere in India. The family's annual income must fall within the designated categories: up to 3 lakh for EWS, 3 to 6 lakh for LIG, or 6 to 9 lakh for MIG segments.

Understanding the New PMAY Urban 2.0 Framework

The updated phase of the Pradhan Mantri Awas Yojana, known officially as PMAY-U 2.0, acts as an upgraded housing mission. It targets helping one crore urban poor and middle-class families build or purchase structural homes.

The central component of this initiative is the Interest Subsidy Scheme (ISS). Instead of receiving a single upfront bulk discount, the government provides a systematic 4% annual interest reduction on home loans up to a maximum threshold of 8 lakh.

Since your total required loan budget is 10 lakh, the PMAY subsidy rules will apply completely to the first 8 lakh portion of your debt. The remaining 2 lakh balance will simply attract the standard market interest rate charged by your primary lending bank.

Step-by-Step PMAY Subsidy Calculations for 10 Lakh

Let us look closely at how this government welfare scheme alters your actual monthly bank outgoings. We will assume a standard market bank lending rate of 8.5% per annum for a 12-year standard subsidy tenure.

Regular Bank Repayment (Without Government Subsidy)

If you borrow a normal 10 lakh home loan without participating in any government welfare scheme, your monthly bank installment sits around 11,120.

Over a 12-year cycle, the total interest accumulated by the bank adds up to roughly 6.01 lakh, creating a total repayment footprint of 16.01 lakh.

Repayment Structure (With Active PMAY-U 2.0 Subsidy)

When your profile is approved under the 10 lakh home loan under PMAY subsidy track, the government begins injecting 36,000 directly into your loan account every single year.

Because this cash reduces your core principal balance, the bank re-calculates your interest on a smaller outstanding amount. Your effective interest rate drops, saving you up to 1.80 lakh in total interest over the scheme period and dropping your monthly liability significantly.

Core Eligibility Parameters for First-Time Buyers

The housing ministry enforces strict structural check lines to ensure that these subsidized interest benefits reach genuine, hardworking families.

1. The Homeownership Rule

The most fundamental requirement is that the primary applicant, their spouse, and any unmarried children must not own a permanent pucca house anywhere across India. This scheme is strictly designed to support first-time property buyers.

2. Income Category Brackets

Lenders verify your family's global annual income using standardized tax brackets. Your total income decides your qualifying bracket.

Economically Weaker Section (EWS): Total annual household income up to 3 lakh.

Low-Income Group (LIG): Total annual household income ranging from 3 lakh to 6 lakh.

Middle-Income Group (MIG): Total annual household income ranging between 6 lakh and 9 lakh.

3. Property Size and Value Boundaries

To keep the focus on affordable housing, the property value must not cross a maximum cap of 35 lakh, and the total home loan must stay under 25 lakh. Additionally, the maximum carpet area of the house layout must remain within 120 square meters.

Document Checklist for a Subsidized Home Loan

To ensure your application flows through the electronic screening verification portals without receiving error flags, compile these clean files in advance.

Aadhaar and PAN Profiling: Clear copies of your PAN card and your Aadhaar card. Ensure your Aadhaar is linked to your active mobile number for biometric OTP authentication.

Family Identity Mapping: Aadhaar details of all individual immediate family members living inside your household.

Income Validation Records: Official salary slips, past six months' bank account statements, or a verified income certificate issued by a local government officer like a Tehsildar.

Property Title Papers: The registered sale agreement, plot allotment letter, and verified blueprint maps proving the land falls inside a certified urban town boundary.

Self-Declaration Affidavit: A legally stamped declaration form confirming that your family owns zero permanent brick houses across the country.

Step-by-Step Application Process Online

Securing a subsidized micro-housing loan requires a systematic approach across digital banking channels.

Step 1: Register Demand on the Unified Portal

Visit the official Ministry of Housing and Urban Affairs prescribed site. Select the dedicated button labeled "Apply for PMAY-U 2.0" and enter your validated Aadhaar credentials to initiate your interest subsidy demand profile.

Step 2: Choose a Partner Lending Institution

Approach an approved Primary Lending Institution (PLI), such as the State Bank of India, top private sector banks, or certified micro housing finance companies. Submit your 10 lakh loan file while referencing your online PMAY application number.

Step 3: Complete Geo-Tagging and Disbursal

Once the bank approves your structural documentation, they will send a surveyor to geo-tag your property plot using satellite location apps. The bank then releases the 10 lakh to start construction, and your subsidy installments begin rolling in annually.

Conclusion: Claim Your Right to Affordable Housing

Utilizing a 10 lakh home loan under PMAY subsidy pathway is an incredibly smart, financially secure strategy for lower and middle-income families in India. The 4% annual interest drop on your core principal shields your household from high interest rates and reduces the long-term debt burden on your children.

Make sure your chosen residential property lies within official municipal borders, maintain a completely clean financial record, and coordinate with a registered lender to construct your dream home safely and economically.

Frequently Asked Questions (FAQs)

One: Is female co-ownership mandatory to get the PMAY Urban 2.0 subsidy?

Yes, the PMAY-U 2.0 scheme focuses heavily on women's empowerment. The house must be registered in the name of an adult female head of the household, or held under active joint ownership between spouses, except in rare cases where the family has no adult female member.

Two: What happens to my annual subsidy if I close my 10 lakh loan early?

The government releases the 1.80 lakh interest subsidy benefit in five equal annual chunks of 36,000, provided your loan account remains active. If you fully prepay and close your home loan account in the third year, any future pending subsidy installments will automatically stop.

Three: Are there any processing fees for a 10 lakh loan under the PMAY subsidy?

Under the current banking guidelines for PMAY-U 2.0, primary lending institutions are restricted from charging any upfront processing fees for loan amounts up to 8 lakh. For a 10 lakh loan, regular processing fees may apply only to the remaining 2 lakh balance portion.

Four: Can I claim this interest subsidy to buy an old resale house?

Yes, the current Interest Subsidy Scheme vertical explicitly covers the purchase of brand-new houses, the repurchase of existing old resale properties, and the self-construction of fresh residential units on an empty plot of land located within urban limits.

Five: What happens if my loan account turns into an NPA?

To receive the annual 36,000 credit, your home loan account must stay fully active and healthy. If you miss multiple EMIs and your bank flags your profile as a Non-Performing Asset (NPA), the government will instantly pause or cancel your remaining subsidy releases.

Six: Can I apply for the PMAY subsidy if I live in a rural village area?

The PMAY Urban 2.0 scheme applies strictly to properties located inside statutory towns, municipal boundaries, and notified urban development centers as per census guidelines. For rural village locations, you must apply under the separate PMAY-Gramin housing portal.