5 Lakh Home Loan for EWS Category Applicant: A Complete Beginner's Guide

Owning a permanent concrete house is a proud asset and a safety shield for every family in India. For people working in the unorganized sector or managing household expenses with limited wages, large financial steps can feel intimidating.

Fortunately, the Government of India and various financial bodies offer special pathways to support your construction dreams. Securing a 5 lakh home loan for EWS category applicant is highly simple today, thanks to low-budget micro-finance options and dedicated central interest subsidies designed to deliver housing for everyone.

Direct Answer Snippets for Quick Reference

Can an EWS category applicant get a 5 lakh home loan?

Yes, securing a 5 lakh home loan for EWS category applicant is completely possible through regular commercial banks, small finance banks, and micro housing finance companies. These institutions have special relaxed approval windows tailored specifically to assist households earning lower annual incomes.

What government subsidy helps EWS home loan applicants?

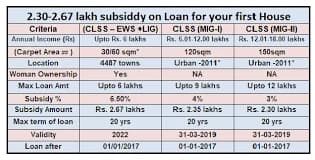

Under the current Pradhan Mantri Awas Yojana Urban 2.0 (PMAY-U 2.0) scheme, an eligible EWS applicant can receive a massive 4% interest subsidy on housing loans up to 8 lakh. This financial support reduces your regular interest rates and lowers your monthly installment amounts significantly.

What is the maximum income limit for an EWS applicant?

To qualify legally as an EWS category applicant for affordable housing schemes in India, your total annual household income must not cross the 3 lakh limit. This total income figure combines the earnings of the applicant, their spouse, and any unmarried earning children.

Defining the EWS Category in Indian Housing Finance

Before submitting a loan application, you must understand who exactly qualifies under the Economically Weaker Section framework. Lenders follow standardized national rules to verify your social and economic standing.

The fundamental rule is that your global household income must stay at or below 3 lakh per year. Additionally, to protect the targeted objective of the welfare policy, the applicant or any member of their immediate family must not own a permanent brick house anywhere across India.

Furthermore, state housing policies and central initiatives place a major focus on women's empowerment. Because of this structural focus, the newly purchased plot or house must be registered under a female family member's name or held under active joint ownership with her.

Incredible Benefits of a 5 Lakh Home Loan for EWS Category Applicant

Opting for a small budget loan within this dedicated economic window unlocks multiple consumer benefits that standard borrowers cannot access.

1. Massive PMAY-U 2.0 Interest Subsidies

When you apply for a 5 lakh home loan for EWS category applicant, your bank forwards your details to the Ministry of Housing and Urban Affairs. You become eligible for a 4% interest subsidy balance.

This benefit amounts to a total savings of up to 1.80 lakh over the loan duration. The government releases this subsidy to your account over five years, reducing your principal burden and dropping your regular EMIs to highly affordable rates.

2. Zero Processing Fee Exemptions

Major financial institutions like the State Bank of India (SBI) and regional housing boards offer complete processing fee waivers for lower-income categories. For loan amounts up to 8 lakh, you do not have to pay any upfront administrative or application handling fees.

3. High Loan-to-Value (LTV) Allowances

Standard luxury loans require buyers to pay 20% to 30% of the property cost upfront from their savings. However, for affordable EWS housing, specialist lenders can fund up to 90% of the total property valuation, meaning you only need to arrange a tiny down payment.

Monthly EMI Projections for a 5 Lakh EWS Loan

Let us look at how much money you need to set aside each month for a 5 lakh loan. While the normal interest rate might sit around 9.5%, a 4% PMAY subsidy drops your effective interest burden drastically.

10-Year Repayment Timeline

If you choose a 10-year period to clear your debt quickly, your monthly EMI installment will sit around 6,470 before the subsidy kickback adjustments.

This plan is brilliant if you have an active youth working window left and want to make your land free from bank liabilities within a short decade.

15-Year Repayment Timeline

A 15-year timeline is the most popular choice for small families. Your monthly commitment drops down significantly to roughly 5,221.

This timeline provides an amazing breathing window, ensuring you have enough money left over every month for your children's school fees and daily kitchen groceries.

20-Year Repayment Timeline

Stretching your timeline to 20 years brings your monthly outgoings to their absolute lowest point of around 4,660.

While a longer timeline accumulates slightly more interest over the decades, it keeps your immediate household budget completely safe from unexpected monthly financial shocks.

Simple Document Checklist for EWS Applicants

Since many EWS applicants work in the unorganized sector without formal company salary slips, banks accept simplified local alternative proofs.

Official EWS Income Certificate: A valid income certificate issued by a locally authorized government officer, such as a Tehsildar or a block development authority.

Identity and Residency Validation: Clean copies of your Aadhaar card and PAN card. Your Aadhaar must be updated with your active mobile number for digital OTP verifications.

Banking Footprints: Passbook photocopies or banking transaction statements covering the past 12 to 24 months to show your regular cash management patterns.

Property and Plot Clearances: The original land allocation papers, sale agreements, or village layout maps proving the land is completely free from active legal court disputes.

Self-Declaration Affidavit: A simple signed declaration form stating that you do not own any other permanent brick house across the territory of India.

Step-by-Step Application Guide for EWS Housing Loans

Getting your loan sanctioned requires a step-by-step approach to make sure you do not miss out on your eligible government subsidies.

Step 1: Secure Your Government Certificates

Visit your local district administrative office or citizen service center to secure your updated EWS income certificate. Ensure the certificate is freshly issued for the current financial year.

Step 2: Choose a Registered Affordable Lender

Do not approach high-end corporate banks. Look for regional small finance banks or housing finance corporations that are actively certified to distribute PMAY-U 2.0 benefits.

Step 3: Fill Out the Subsidized Application Form

Submit your property papers along with your identity documents to the bank. Specify clearly on the application header that you are applying under the Interest Subsidy Scheme (ISS) for the EWS category.

Conclusion: Build Your Secure Future Today

Securing a 5 lakh home loan for EWS category applicant is a practical and highly respectable way to build a permanent roof over your family's head. The combination of low principal requirements, a 4% central interest subsidy, and flexible document verification models makes homeownership highly accessible for low-income households.

Take time to compile your income certificates correctly, prioritize adding a female head of the family as a property co-owner, and choose a trusted local lender to build your dream home safely and comfortably.

Frequently Asked Questions (FAQs)

One: Can a single mother apply for a 5 lakh home loan for EWS category applicant?

Yes, single mothers, widows, and unmarried women receive absolute highest priority under the EWS housing rules. Lenders offer relaxed verification guidelines to single women applicants to ensure they can secure independent and safe housing.

Two: What happens if my household income increases beyond 3 lakh after the loan is approved?

Your eligibility is checked strictly at the time of your loan application and data submission. If your career grows and your family income increases in the future, your existing loan and approved subsidy status will remain completely valid and unaffected.

Three: Is a CIBIL score mandatory for an EWS category home loan?

While a high credit score is helpful, it is not mandatory. Many micro-housing finance groups look at alternative metrics, such as your daily UPI transactions, retail shop turnover, or savings account history, to pass your loan safely without a previous credit history.

Four: Can I get this EWS loan to repair or extend my existing village home?

Yes, the Beneficiary Led Construction (BLC) vertical of the PMAY urban framework explicitly permits EWS category applicants to utilize these funds to convert an old mud house into a concrete one or add extra rooms to an existing small house.

Five: Can I sell the house immediately after building it with an EWS loan?

No, the government enforces strict rules to prevent speculative trading of affordable houses. You cannot sell the property or transfer the land title for a minimum lock-in period of five years from the date you take physical possession of the finished house.

Six: Are agricultural workers eligible for an EWS home loan?

Yes, agricultural workers, daily wage laborers, street vendors, and artisans are fully eligible. They simply need to provide an official income certificate from their local authority to prove their annual earnings sit below the 3 lakh mark.