6. 5 Lakh Home Loan under PM Awas Yojana: A Beginner's Guide

Building or buying a permanent home is a major dream for families across India. If your household savings are limited, the central government provides powerful credit options to help you complete construction safely.

The most successful program supporting first-time homebuyers is the Pradhan Mantri Awas Yojana, also known as PMAY. Securing a 6. 5 lakh home loan under PM Awas Yojana allows you to leverage massive interest discounts that make your monthly bills incredibly affordable.

This honest, clear guide cuts out all confusing government jargon. We explain how the Interest Subsidy Scheme operates, who qualifies for benefits, and how to submit a flawless application to your lender.

Google Featured Snippet Answers

What is a 6. 5 lakh home loan under PM Awas Yojana? A 6. 5 lakh home loan under PM Awas Yojana is an affordable housing credit option backed by the Indian government's interest subvention programs. Eligible first-time buyers receive a direct four percent to 6.5% discount on their loan interest rate, lowering the overall principal burden and reducing monthly installment bills significantly.

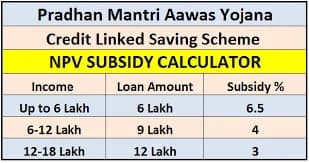

How does the PMAY interest subsidy benefit lower-income groups? The interest subsidy program acts as an upfront credit applied directly to your home loan balance. For a five to six lakh loan tier, the central government releases an upfront subsidy benefit cap of up to 1.80 lakh rupees, meaning you only pay regular bank interest on the remaining remainder.

Who can apply for a small housing loan under the PM Awas program? Any resident Indian family belonging to the Economically Weaker Section or Low Income Group can apply, provided their annual household income stays below six lakh rupees. The primary condition is that the applicant and their immediate family members must not own any other permanent brick house anywhere in India.

The Basics of the Interest Subsidy Scheme (ISS)

The primary reason why a 6. 5 lakh home loan under PM Awas Yojana is so cheap is the central Interest Subsidy Scheme. Instead of forcing you to pay standard market bank interest rates, the government steps in to pay a major chunk of your interest bill.

Under the updated PMAY Urban 2.0 guidelines, eligible families receive a steady interest subvention rate of 4.0% per annum on loan amounts up to eight lakh rupees. This direct financial aid translates to an actual total cash saving of up to 1.80 lakh rupees over your tenure.

When your application is approved, the central nodal agencies credit this entire subsidy sum directly into your loan account upfront. This instant credit reduces your active loan principal, allowing the bank to recalculate a much smaller monthly instalment bill for your household.

Realistic Payment Comparison Chart

To understand how a 6. 5 lakh home loan under PM Awas Yojana alters your cash outlays, review this realistic comparison assuming a standard bank base rate of 8.50% versus your effective subsidized rate:

Financial Scenario | Loan Principal | Applied Interest Rate | Typical Loan Tenure | Estimated Monthly Payment | Total Interest Paid Over Timeline |

|---|---|---|---|---|---|

Standard Bank Loan | 6.5 Lakhs | 8.50% (Standard) | 15 Years | 6,401 Rupees | 5,02,085 Rupees |

PMAY Subsidized Loan | 6.5 Lakhs | 4.50% (Subsidized Effective) | 15 Years | 4,973 Rupees | 2,45,152 Rupees |

Mandatory Eligibility Rules for PMAY Housing Loans

Even though a five to six lakh credit line is a small, safe principal amount, you must meet strict national guidelines to qualify for government credit benefits.

1. Household Property Ownership Restrictions

The core rule of the "Housing for All" mission is that the beneficiary family must be a first-time homebuyer. If you, your spouse, or your unmarried children own a permanent concrete house anywhere in India, your application will be automatically rejected.

2. Annual Family Income Categories

Your eligibility tier is determined by adding up the annual earnings of all working family members residing under the same roof:

Economically Weaker Section (EWS): Total household income up to three lakh rupees per year.

Low Income Group (LIG): Total household income ranging from three lakh rupees to six lakh rupees per year.

Household Earnings Under 6 Lakhs + First-Time Home Buyer = Maximum PMAY Discount Eligibility

3. Property Carpet Area Limitations

The home you intend to buy or build must fit within specified size boundaries. For families in the EWS category, the maximum carpet area is restricted to 30 square meters, while LIG buyers enjoy a expanded cap of up to 60 square meters.

Crucial Preferences and Document Verification Rules

The Indian government uses this housing program to build social security and support women's financial independence across both rural and urban areas.

Women Empowerment Mandate

For families applying under the urban low-income categories, the house paperwork must feature a female family member's name as an owner or co-owner. This female registration rule is mandatory for purchasing new flats, though exceptions apply for self-construction on pre-owned ancestral land plots.

Complete Document Checklist for Applicants

To clear the vetting process for a 6. 5 lakh home loan under PM Awas Yojana, you must provide clear copies of the following records to an approved lender:

Personal Identity Trackers: Your PAN card and your Aadhaar card, which must be biometrically linked to your active mobile number.

Proof of Income Status: Official salary vouchers, employer certificates, certified bank statement records, or local income certificates issued by district authorities.

Property Clearances: An official sales agreement, verified building layouts, approved construction blueprints, and a signed self-declaration stating you do not own a permanent house.

Step-by-Step Guide to Applying for Your Subsidized Loan

Securing your subsidized housing loan does not require running around local government offices. The process is completely integrated into standard bank applications.

Step 1: Visit an Approved Primary Lending Institution

Approach a public sector bank, a registered small finance bank, or an approved housing finance company. Ask the loan department directly for their specific application forms for the PMAY Interest Subsidy Scheme vertical.

Step 2: Register on the Unified Housing Portal

Your loan officer will assist you in entering your details online via the official government web portal. This system runs an automated check across nationwide property records to confirm your first-time buyer status instantly.

Step 3: Enjoy Upfront Principal Reductions

Once the central nodal tracking agency confirms your file is clean, they route the subsidy funds directly to your bank. The bank applies this cash straight into your loan book, lowering your ongoing monthly outlays automatically.

Conclusion

Securing a 6. 5 lakh home loan under PM Awas Yojana is one of the smartest financial strategies for middle-class families to achieve affordable homeownership. By capturing an upfront interest discount of up to 1.80 lakh rupees, you keep your long-term interest costs minimal and preserve your daily household budget.

To guarantee success, ensure that your identity documents are completely free of spelling errors, confirm your property fits within the official carpet area sizes, and register your house with a female co-owner. With disciplined planning, you can move into your permanent dream home with absolute financial peace of mind.

Frequently Asked Questions

Is the PMAY interest subsidy available if I buy a resale property? Yes, the updated housing guidelines clarify that the Interest Subsidy Scheme covers the purchase of brand-new properties, the re-purchase of older resale homes, and the self-construction of rooms on your own independent land plots.

Can I get a loan for more than six lakhs under this government scheme? Yes, you can borrow a larger sum, such as ten or twelve lakh rupees, from your bank based on your salary profile. However, the special interest subsidy rate will only apply to the first subsidized loan tier limit, while the rest of your balance follows regular market interest rates.

What is the maximum time timeline allowed to pay back this subsidized loan? The interest subsidy calculation uses a maximum tenure limit of twenty years. While you can choose a longer loan timeline with your private bank if needed, the government's interest discount value is strictly capped at a twenty-year calculation limit.

Do I need to pay a separate commission to agents to get this subsidy? No, you should never pay money to external agents or third-party middlemen. The subsidy process is completely free and handled electronically between your primary lending bank and the central government via direct benefit transfers.

What happens if I decide to transfer my subsidized loan to a different bank later? If you choose to move your loan balance to a different bank via a balance transfer plan later on, you will lose any remaining future subsidy installments. The rules state that subsidy benefits cannot be transferred to a second financial institution.

Can a freelancer apply for a 6. 5 lakh home loan under PM Awas Yojana packages? Yes, self-employed freelancers, shopkeepers, and informal sector workers qualify easily. You simply need to provide alternative proofs of financial stability, such as twelve months of consistent UPI bank statements or local business registration proofs, to satisfy your bank's safety checks.