Lowest Interest Rate for Used Car Loan in India: A Practical Guide

Buying a pre-owned car is an incredibly smart financial move. It helps you dodge the steep initial depreciation that hits a brand-new vehicle the moment it rolls out of the showroom. However, once you pick your ideal second-hand hatchback or sedan, finding the right financing option becomes your next big step.

Many buyers are surprised to learn that interest rates for used vehicles are generally higher than those for new cars. Because lenders take on more risk with an older vehicle, they price that risk directly into your monthly payments.

Fortunately, with the right strategy and a strong credit background, you can still unlock highly affordable financing. This honest guide breaks down how to find the lowest interest rate for used car loan in india, compares top institutional lenders, and explains how to keep your total interest costs minimal.

3 Direct Answer Snippets for Quick Understanding

What is the lowest interest rate for a used car loan in India?

The lowest interest rate for used car loan in india typically starts from 8.65% to 10.50% per annum. Public sector banks like Punjab National Bank and top private institutions like HDFC Bank offer these premium entry-level rates exclusively to borrowers with excellent credit scores.

Why are used car loan interest rates higher than new car loans?

Used car loan interest rates are higher because pre-owned vehicles carry a greater depreciation risk and a lower resale value for the bank. If a borrower defaults, recovering the outstanding amount by selling an older, used vehicle is much harder for the lender compared to a brand-new car.

How can I get the lowest interest rate on a second-hand car loan?

To get the absolute lowest rate, maintain a CIBIL credit score above 750, make a substantial down payment of 20% to 25%, and select a younger vehicle under three years old. Applying through a bank where you already hold a salary account also unlocks preferential loyalty rates.

Understanding Used Car Loan Interest Rates

A pre-owned car loan is a secured credit facility where the second-hand vehicle you buy acts as the primary collateral. The bank holds a legal lien on your vehicle's registration certificate (RC) until you completely clear your outstanding loan principal.

Lenders in India generally fix your interest rates by combining a national market benchmark with a personalized risk premium. While public sector banks often provide lower, market-linked floating rates, private financial institutions frequently offer stable, fixed interest rates that stay identical throughout your tenure.

Because used vehicles age differently based on maintenance, lenders do not offer a single uniform rate to everyone. Your final quote is highly customized based on your financial discipline and the specific condition of the vehicle.

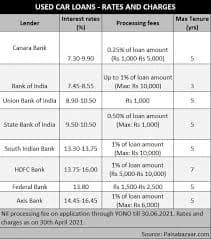

Top Banks Offering the Lowest Pre-Owned Car Loan Rates

If you want to keep your borrowing costs low, you should research multiple institutional lenders before making a final commitment. Here is a realistic look at top lenders in India and their entry-level rate brackets:

1. Punjab National Bank (PNB)

PNB stands out as a highly aggressive player in the pre-owned vehicle segment, offering starting interest rates near 8.65% to 10.45% per annum. They provide generous loan amounts but apply strict evaluation standards to the age of the car.

2. HDFC Bank and ICICI Bank

These private sector giants are famous for execution speed and smooth digital processing through frameworks like Xpress Car Loans. Their pre-owned interest rates generally start around 10.49% per annum, making them ideal for quick, hassle-free turnarounds.

3. State Bank of India (SBI)

SBI runs a specialized Certified Pre-owned Car Loan Scheme with interest rates ranging from 10.45% to 15.60% per annum. While their processing involves manual checks, they offer complete transparency with zero hidden fees and no foreclosure penalties.

Core Factors That Influence Your Used Car Loan Rate

To successfully secure the lowest interest rate for used car loan in india, your application must look highly safe to the bank's automated screening filters. Lenders evaluate these critical areas:

1. Your Personal CIBIL Score

Your credit history is the single most important factor. A robust CIBIL score of 750 or above proves to the bank that you treat your financial promises with respect, instantly qualifying you for the lowest interest rate tiers.

2. The Age and Brand of the Vehicle

Lenders prefer financing younger cars from trusted, high-resale manufacturers. A 2-year-old certified pre-owned car with a clean service history will easily secure a lower interest rate than an 8-year-old discontinued model line.

3. Your Existing Relationship with the Bank

Banks frequently extend preferential pricing and processing fee waivers to their existing customers. Checking your pre-approved loan options with your primary salary account bank is an excellent way to start your search.

Essential Eligibility Criteria for Used Car Finance

While requirements differ slightly across various public and private institutions, you must fulfill these standard baseline rules to qualify for a used vehicle loan:

Age Boundaries: The applicant must be a minimum of 21 years old when applying and should not exceed 60 to 65 years at the time of final loan maturity.

Steady Income Stream: Salaried professionals need a regular monthly income of at least 20,000, while self-employed business owners must show steady annual business revenues.

Vehicle Age Limits: Most commercial banks mandate that the total age of the vehicle should not cross 8 to 10 years by the time the loan tenure ends safely.

Step-by-Step Process to Secure Your Loan Online

Filing your car finance application through digital bank portals minimizes administrative delays. Follow this simple path to get approved quickly:

Step 1: Use a Digital Loan EMI Calculator

Before speaking to any dealer, use an online car loan calculator. Input your required capital and run different interest scenarios to find a monthly installment layout that fits your budget.

Step 2: Check Your Personal Credit History

Download your latest CIBIL report. If you spot any small errors or active outstanding disputes, clear them early to push your score into the premium lending bracket.

Step 3: Secure the Vehicle Valuation Certificate

Lenders will not fund a used car based on the dealer's verbal word. An authorized bank surveyor or a certified pre-owned platform must evaluate the vehicle to establish its true legal market price.

Step 4: Upload Documents on the Bank Portal

Submit your scanned personal KYC cards, recent bank account statements, income proofs, and the vehicle's valuation papers through the bank's secure digital application page.

Step 5: E-Sign the Agreement and Drive Home

The credit team will verify your vehicle's background and title clearance. Upon final approval, review the document to check for hidden processing charges, and sign via an Aadhaar OTP to initiate direct fund transfer to the seller.

Conclusion

Securing the lowest interest rate for used car loan in india requires a mix of good personal credit discipline and smart vehicle selection. By keeping your CIBIL score high, opting for a younger certified vehicle, and building a solid down payment fund, you can successfully bypass expensive lending traps.

Remember to look beyond just the raw interest percentage; always evaluate processing fees and foreclosure terms to understand the true total cost of your credit line. By partnering with transparent, reputable banking partners, you can comfortably finance your dream vehicle while keeping your monthly budget safe and stress-free.

Frequently Asked Questions (FAQs)

1. What is the maximum loan tenure available for a used car in India?

Most prominent banks and financial institutions restrict the maximum repayment tenure for a pre-owned car loan to 5 years (60 months). However, for select premium certified vehicles that are less than two years old, institutions like HDFC Bank and ICICI Bank may extend the tenure up to 7 years.

2. Can I get 100% financing on a second-hand car loan?

No, getting 100% on-road funding is generally reserved for new vehicles. For used cars, banks usually fund 80% to 85% of the vehicle's value based strictly on their internal surveyor's valuation report. The remaining 15% to 20% margin must be paid by the buyer as a down payment.

3. Does making a higher down payment help in lowering the interest rate?

Yes, making a substantial down payment of 20% to 25% directly reduces the total loan amount you need to borrow. This instantly lowers the bank's background risk profile, giving you excellent leverage to negotiate a lower annual interest rate margin with the credit manager.

4. What are the typical processing fees for a pre-owned car loan?

Processing fees vary depending on your chosen bank. Public sector banks often charge a small, flat fee ranging from 1,000 to 3,000 plus GST. Large private commercial banks usually charge a percentage-based processing fee, typically ranging from 0.5% to 1% of the total sanctioned loan amount.

5. What happens if I want to close my used car loan early?

If you choose a floating interest rate loan through a public bank, you can generally foreclose or prepay your loan for free. However, private banks and NBFCs often impose a foreclosure charge ranging from 3% to 5% on the remaining principal outstanding balance if you close the loan early.

6. Can I buy a used car directly from an individual owner using a bank loan?

Yes, you can easily finance a direct individual-to-individual sale. The bank will require the vehicle's original registration certificate, valid insurance copies, and a clear transfer of ownership framework. Once the title check is approved, the bank transfers the loan cash directly to the original owner's bank account.