HDFC Used Car Loan Interest Rate for Existing Customers: A Simple Guide

Buying a pre-owned car is an excellent way to save money while upgrading your daily transit comfort. Pre-owned vehicles let you enjoy a premium driving experience without facing the steep initial depreciation hits that hurt a brand-new vehicle. Once you zero in on a reliable second-hand car, finding affordable financing lines is the logical next step.

When looking for used vehicle loans, borrowing from your existing bank branch brings massive financial advantages. HDFC Bank values long-term banking relationships and offers distinct advantages to its current members. The hdfc used car loan interest rate for existing customers framework features reduced interest margins, minimal processing steps, and instant digital approvals.

CreditMantri

This honest financial overview breaks down the exclusive preferential interest rate bands available in 2026, hidden operational fees, eligibility shortcuts, and step-by-step digital application methods for current account holders.

3 Direct Answer Snippets for Quick Understanding

What is the HDFC used car loan interest rate for existing customers?

The hdfc used car loan interest rate for existing customers typically starts from 9.40% to 11.25% per annum for premium relationship profiles. Current account holders, salary account savers, and existing home loan borrowers receive a clear loyalty discount compared to the standard market rack rates that start from 11.25% onwards.

Why do existing HDFC customers get lower pre-owned vehicle rates?

Existing HDFC customers get lower interest rates because the bank can check their historical savings patterns, monthly salary credits, and credit card usage data internally. This deep visibility lowers the bank's default risk, allowing credit managers to waive extra risk premium fees and offer rapid, low-interest approvals.

How fast can an existing HDFC customer get a used car loan?

If you have a pre-approved loyalty offer under programs like the Xpress Pre-Owned Car Loan, the digital verification engine can approve your profile within 10 to 30 minutes. Once your vehicle appraisal checks are completed, the cash reaches the car seller's bank account within 24 to 48 hours.

The Advantages of an Existing Relationship with HDFC Bank

Commercial lenders always prioritize safety when processing vehicle loans. Because a second-hand vehicle loses value over time, banks apply strict verification checks to safeguard their funds. If you are an outsider applying for credit, the bank requires extensive paperwork to construct a clear picture of your honesty.

However, if you already route your corporate salary or handle an active business current account through HDFC Bank, you skip these long introductory hurdles. The bank treats your active history as a valid trust certificate.

By leveraging your banking data internally, HDFC Bank can bypass manual verification steps. This helps them offer special interest rate concessions, lower documentation rules, and higher funding limits directly on your net banking app.

Breaking Down the Interest Rate and Fee Structure

HDFC Bank structures its pre-owned vehicle finance loans using fixed internal borrowing metrics. Here is a clear look at the interest rates and standard operational fees active in 2026:

Preferential Interest Rate Window

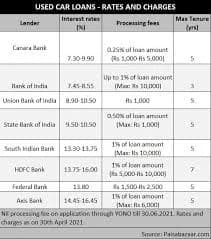

While standard market customers pay higher annual interest rates that go up to 16.51% for aged assets, existing relationship members hold a strong advantage. Premium savers with a CIBIL score above 750 can secure initial interest rates starting from 9.40% to 11.25% per annum, depending on the age of the vehicle.

Processing and Administrative Fees

The bank charges a standard one-time processing fee capped at 1% of the total loan amount, with a baseline minimum of 3,500 and a ceiling maximum of 9,000. Additionally, a minor asset valuation and vehicle verification charge of 750 is collected to execute the physical surveyor check.

ClearTax+ 1

Part-Payment and Foreclosure Rules

To protect your long-term budget agility, check the closure rules before accepting an offer. HDFC Bank permits part-payments twice during the loan tenure after you complete 12 initial EMIs. If you decide to close the loan early, the premature closure fees vary based on time:

HDFC Bank

Within 1 Year: 6% of the remaining principal outstanding balance.

HDFC Bank

13 Months to 24 Months: 5% of the remaining principal outstanding balance.

HDFC Bank

Post 24 Months: 3% of the remaining principal outstanding balance.

HDFC Bank

Core Factors That Determine Your Final Interest Rate

Even within the exclusive customer bracket, the bank does not distribute identical rate structures to everyone. The credit underwriting engine evaluates three key variables to fix your final margin:

CreditMantri

1. Age and Category of the Used Car

Lenders prefer financing younger pre-owned cars manufactured by trusted brands that retain a high resale value. A 2-year-old certified vehicle with a clean service history will easily secure the lowest interest rate bracket compared to an 8-year-old model.

2. Personal CIBIL Credit Score

Your personal financial track record remains a critical trust factor. Maintaining a personal credit score of 750 or above tells HDFC Bank that you manage your liabilities responsibly, enabling you to secure lower rate quotes.

Forbes

3. Your Account Category and Vintage

A current or salary account holder who has maintained a large, healthy average monthly balance for over three years will receive much better interest rate terms and processing fee discounts than a newly registered account holder.

Essential Documents Checklist for Existing Members

One of the best benefits of executing an hdfc used car loan interest rate for existing customers application is the minimal paperwork. If your account is fully KYC-compliant, you only need basic car papers. Keep these items ready:

HDFC Bank

Promoter Personal Identification: Your PAN card and Aadhaar card (used primarily to generate a secure login OTP verification).

Vehicle Authenticity Records: The car's original Registration Certificate (RC) booklet, active comprehensive vehicle insurance sheets, and a clear tax clearance receipt.

Dealer Proforma Bill: A clear pricing sheet or valuation invoice issued by an authorized car dealer or certified pre-owned car showroom platform.

Step-by-Step Online Application Path for HDFC Customers

Filing your pre-owned vehicle loan request online minimizes manual administrative friction. Follow this step-by-step path using your smartphone:

Step 1: Log in to HDFC NetBanking or Mobile App

Open your HDFC Bank internet banking dashboard. Navigate directly to the "Offers" section to check if you possess a pre-approved pre-owned vehicle loan limit waiting on your profile.

Step 2: Use the Digital Pre-Owned EMI Calculator

Input your desired vehicle funding values into the bank's digital car loan calculator. Adjust the repayment months (up to a maximum of 60 months) until the monthly installment fits safely within your salary budget.

HDFC Bank

Step 3: Fill Out the Electronic Vehicle Information Form

Enter the exact make, model, age, and registration details of the second-hand car you wish to buy. Submit your information to generate a preliminary sanction letter.

Step 4: Complete the Physical Asset Valuation

HDFC Bank will coordinate a brief physical inspection of the car through an authorized automobile surveyor to check the engine status and verify its true market valuation bounds.

Step 5: Sign via OTP and Receive Disbursal

Once the system confirms your asset parameters, review the loan agreement to check interest rates and processing fees. Sign the contract digitally using an Aadhaar OTP to allow the bank to transfer the funds directly to the car seller or dealer.

Conclusion

Fulfilling the simple application process for an hdfc used car loan interest rate for existing customers is a highly efficient, practical, and pocket-friendly way to purchase a pre-owned car. By turning your long-term banking loyalty and high credit score into a distinct financing edge, you can bypass heavy interest expenses and access immediate liquidity safely.

Remember to balance your short-term desires with long-term budget parameters; select a fuel-efficient vehicle model, verify vehicle title histories on the government's Vahan database, and avoid delayed payments to keep your credit history spotless. By partnering with your home bank responsibly, you can drive your ideal vehicle home while keeping your financial future safe and secure.

Frequently Asked Questions (FAQs)

1. What is the maximum loan value an existing customer can get for a used car at HDFC Bank?

HDFC Bank offers extensive funding lines for pre-owned cars, with loan limits reaching up to a maximum value of 2.5 Crore. The exact approved amount depends heavily on your verified annual household income, your personal CIBIL score, and the surveyor's valuation report.

HDFC Bank

2. Can I get a 100% on-road loan for a second-hand car from HDFC Bank?

Yes, under specialized pre-approved customer programs like the Xpress Pre-Owned Car Loan, HDFC Bank can extend up to 100% financing on the certified value of select car models. However, for a standard vehicle, the bank typically finances 80% to 85% of the market value, requiring you to cover the balance as a down payment.

HDFC Bank

3. What is the maximum allowed car age at the time of loan maturity?

HDFC Bank mandates that the total age of the pre-owned vehicle should not exceed 10 years at the exact time your loan tenure finishes safely. For instance, if you are purchasing a car that is already 6 years old, the maximum repayment tenure you can select is restricted to 4 years.

HDFC Bank

4. Are there any specialized search assistance features provided by the bank?

Yes, HDFC Bank operates a dedicated digital marketplace called the "Car Bazaar." Existing customers can use this platform to browse, compare, and research thousands of certified used cars by price or brand, ensuring you discover a high-quality vehicle with a clean title history.

5. What happens if I pay my monthly HDFC used car loan EMI late?

If you miss your installment due date, HDFC Bank charges an overdue installment interest penalty of 18% per annum (1.5% per month) on the delayed amount for the exact number of days your payment is late. Additionally, a payment return or bounce fee of 450 is applied if your bank auto-debit fails.

ClearTax+ 1

6. Can I add a co-applicant to lower my interest rate at HDFC Bank?

Yes, adding a close family member (such as a spouse or parent) who holds a steady independent salary or an excellent credit track record as a co-applicant is a smart financial strategy. It instantly lowers the background lending risk for the bank, helping you secure higher loan quantities and better interest rate terms.