What is a mini loan? A mini loan is a small amount of money borrowed for a short period, typically used to cover urgent or unexpected costs. Unlike traditional bank loans that involve large sums, these are designed for quick fixes.

How do mini loans work? You apply for a specific small amount, receive the funds quickly—often within the same day—and pay it back over a few weeks or months. They are ideal for those who need a bridge until their next paycheck.

Are mini loans safe? Yes, provided you use a licensed lender. While they have higher interest rates than long-term mortgages, they offer a legal and structured way to handle financial gaps without asking friends or family for help.

Understanding the Basics of a Mini Loan

When you hear the term mini loan, think of it as a financial "band-aid." It isn't meant to buy a house or a car. Instead, it is there to help you when your bike needs a repair or your phone screen cracks.

Most people prefer a mini loan because the application process is much faster than a standard bank loan. You don't usually need to provide stacks of paperwork or wait weeks for an answer.

Because the amounts are small, the risk to the lender is lower. This often means that even students or people starting their first job can qualify, provided they have a steady way to pay it back.

Why People Choose Mini Loans Over Traditional Loans

Traditional banks often don't like dealing with small amounts. They prefer lending thousands of dollars over many years. This leaves a gap for people who only need a tiny boost.

A mini loan fills this gap perfectly. Whether it is for textbooks, an emergency dental visit, or an unexpected utility bill, these loans provide the exact amount you need without unnecessary debt.

Furthermore, the speed is a major factor. In the digital age, most mini loan providers operate online. You can apply from your phone and see the money in your account almost instantly.

Key Features of a Mini Loan

To understand if this is the right choice for you, it is important to look at the defining characteristics of these small financial products.

1. Small Borrowing Limits

Usually, a mini loan ranges from a tiny amount up to a few hundred units of currency. This keeps the debt manageable and ensures you aren't tempted to overspend.

2. Short Repayment Periods

You aren't locked into a 5-year plan. Most of these loans are settled within 30 to 90 days. This means you can get out of debt quickly and move on with your life.

3. Rapid Approval Process

The "mini" in mini loan also refers to the wait time. Automated systems check your eligibility in minutes, making it a top choice for genuine emergencies.

Eligibility: Who Can Apply for a Mini Loan?

One of the best things about a mini loan is that the entry requirements are usually quite simple. You don't need to be a millionaire to get approved.

Most lenders require you to be at least 18 years old. This ensures that you are legally allowed to enter into a contract. You will also need a valid ID to prove who you are.

A steady source of income is usually necessary. This doesn't always have to be a full-time corporate job; part-time work, freelance income, or even certain stipends might count.

Lenders also look for a bank account. Since the mini loan is usually sent electronically, they need a place to deposit the funds and a way to collect repayments automatically.

The Step-by-Step Application Process

Applying for a mini loan is designed to be stress-free. Here is a breakdown of how the process usually looks from start to finish.

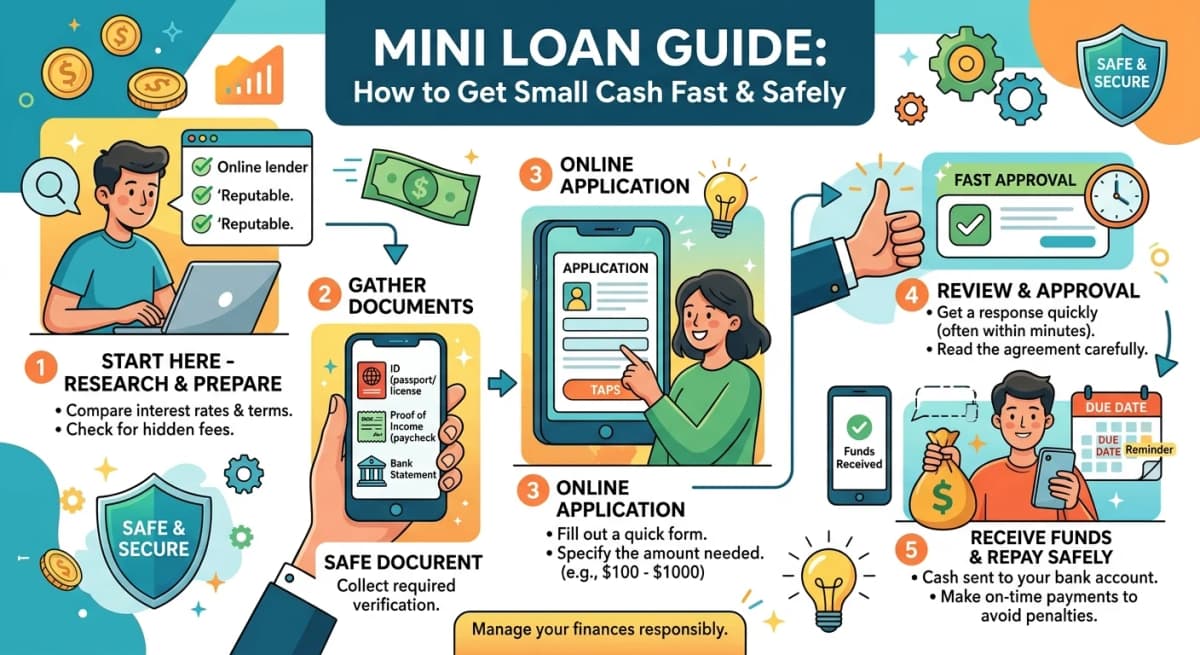

Step 1: Research and Compare

Don't just click the first link you see. Look for a mini loan provider with good reviews and transparent terms. Check their interest rates and any hidden fees.

Step 2: Fill Out the Online Form

You will provide basic details like your name, address, and income. Most mini loan applications take less than ten minutes to complete.

Step 3: Verification

The lender might ask for a digital copy of your ID or a recent bank statement. This is a standard security measure to prevent fraud and protect your identity.

Step 4: Approval and Funding

Once approved, you will receive a contract. Read it carefully! After you sign, the mini loan is typically transferred to your account within hours.

Managing Your Repayments Effectively

Getting the money is the easy part; paying it back requires a bit of discipline. Since a mini loan is a short-term commitment, you need a plan.

Set a reminder on your phone for the due date. Many lenders use automatic withdrawals, so you must ensure there is enough money in your account on that specific day.

If you find that you cannot make a payment, contact the lender immediately. Most mini loan companies are willing to work with you if you are honest about your situation.

Avoid taking out a second mini loan to pay off the first one. This creates a cycle of debt that can be very hard to break. Only borrow what you are certain you can return.

Pros and Cons of a Mini Loan

Every financial tool has two sides. Being aware of both will help you make an informed and honest decision for your future.

The Benefits

Accessibility: Easier to get than a credit card or a large personal loan.

Speed: Ideal for situations where time is of the essence.

No Long-Term Debt: You pay it off quickly and stay debt-free.

The Risks

Cost: The interest rates are often higher than larger, secured loans.

Late Fees: Missing a deadline can result in extra charges that add up fast.

Impact on Credit: If you don't pay back your mini loan, it can hurt your credit score.

Conclusion: Is a Mini Loan Right for You?

In summary, a mini loan is a powerful tool for managing short-term financial hurdles. It offers a level of speed and convenience that traditional banking simply cannot match.

However, it should be used responsibly. It is not a solution for long-term financial problems or for buying luxury items you don't really need.

If you have a clear plan for repayment and a genuine need for quick cash, a mini loan can provide the peace of mind you need to get through a tough week. Always borrow wisely and read the fine print.

Frequently Asked Questions (FAQs)

1. How quickly can I get a mini loan?

Most online lenders process applications within minutes. If you are approved, the funds for your mini loan are often sent to your bank account on the same business day, though it depends on your bank's processing times.

2. Can students apply for a mini loan?

Yes, students can often apply. As long as you are over 18 and can show a consistent way to repay the money—such as a part-time job or a regular allowance—many lenders will consider your application.

3. Does a mini loan require a credit check?

Most lenders will perform a "soft" or "hard" credit check. However, because the mini loan amounts are small, some lenders focus more on your current income and ability to pay than on your past credit history.

4. What happens if I pay back my mini loan early?

Many modern lenders allow you to pay back your loan early without any penalties. Doing this can actually save you money on interest, as you are only paying for the days you actually used the money.

5. What are the typical interest rates for a mini loan?

Interest rates for a mini loan are generally higher than for a mortgage or an auto loan. This is because they are unsecured and short-term. Always check the Annual Percentage Rate (APR) on the lender's website before signing.

6. Can I have more than one mini loan at a time?

While it may be legally possible in some places, it is highly discouraged. Taking multiple loans increases your financial burden and makes it much harder to manage your monthly budget effectively.