Understanding Your Personal Loan

A personal loan is an "unsecured" loan. This means you do not have to put up collateral like your house or car. Because the bank takes a higher risk, the interest rates can be higher than a mortgage.

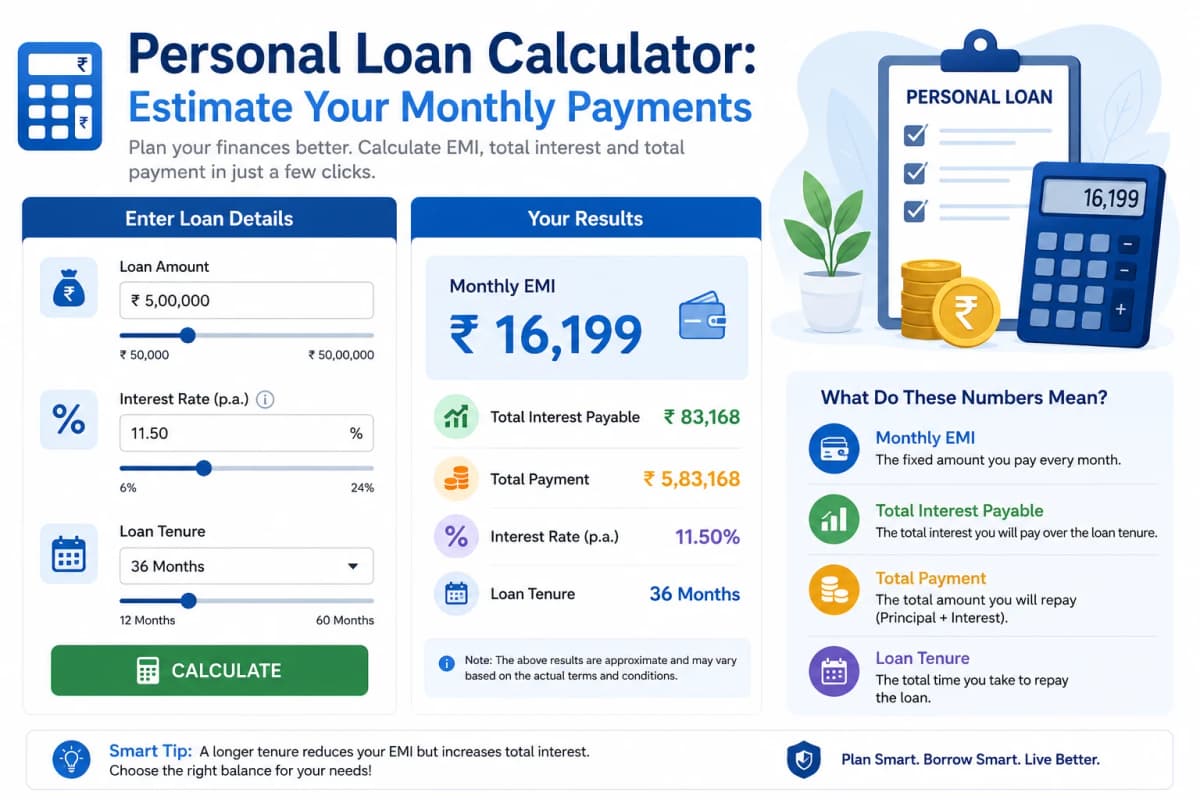

Before you apply, you must understand three main things: the principal, the interest rate, and the tenure. A personal loan calculator uses these three numbers to tell you your future.

The Principal Amount

The principal is the total amount of money you want to borrow. If you need 10,000 for a medical bill, 10,000 is your principal.

The Interest Rate

This is the "price" of borrowing money. It is usually shown as an Annual Percentage Rate (APR). The lower your credit score, the higher this rate will usually be.

The Loan Tenure

Tenure is how long you have to pay the money back. This is usually measured in months or years. A longer tenure means lower monthly payments, but you will pay more in total interest over time.

How a Personal Loan Calculator Works

Most people find math confusing, and that is okay. The personal loan calculator does the hard work for you. It takes your numbers and applies them to a standard formula.

Breaking Down the EMI

EMI stands for Equated Monthly Installment. It is a fixed amount you pay to the lender every month. Part of this money goes toward paying off the interest, and the rest goes toward the principal.

In the beginning of your loan, most of your EMI goes toward interest. As time goes on, more of your payment starts to eat away at the principal. This process is called amortization.

Visualizing Your Debt

A good personal loan calculator often provides an amortization schedule. This is a table that shows exactly how much interest and principal you pay each month until the balance reaches zero.

Why You Need a Personal Loan Calculator

Many people make the mistake of looking only at the monthly payment. While the monthly payment matters for your budget, it doesn't tell the whole story.

1. Comparing Different Lenders

Different banks offer different rates. One bank might offer 10 percent, while another offers 12 percent. By plugging these into a personal loan calculator, you can see exactly how much money you save over three years by choosing the lower rate.

2. Finding the Right Tenure

If your monthly payment is too high, you can use the personal loan calculator to see what happens if you extend the loan by one year. While your monthly cost drops, you will see the total interest cost go up. This helps you find a balance between "affordable now" and "cheap in the long run."

3. Avoiding Hidden Costs

While the calculator focuses on interest, it reminds you to look for processing fees. If a loan has a 1 percent processing fee, you can add that to your total cost to see if the loan is still a good deal.

Steps to Use an Online Personal Loan Calculator

Using these tools is very simple. Most websites have sliders that you can move back and forth to see real-time changes.

Step 1: Enter the Principal

Move the slider to the amount you need. Be honest with yourself—only borrow what you truly need to solve your problem.

Step 2: Input the Interest Rate

Enter the rate you think you will qualify for. If you have great credit, use a lower number. If your credit is fair, use a higher number to be safe.

Step 3: Choose the Timeframe

Select how many years or months you want to take to pay it back. Watch how the EMI changes as you adjust the time.

Step 4: Analyze the Results

Look at the "Total Interest Payable." If that number shocks you, try to shorten the loan tenure or borrow a smaller principal.

Factors That Affect Your Personal Loan Rates

When you use a personal loan calculator, you are making an estimate. The actual rate a bank gives you depends on several personal factors.

Your Credit Score

This is the most important factor. A high score tells the bank you are a responsible borrower. This leads to lower interest rates.

Your Income and Employment

Lenders want to see that you have a steady job. They often look at your debt-to-income ratio. This is the percentage of your monthly income that already goes toward paying debts.

The Loan Amount

Sometimes, borrowing a very small amount has a higher interest rate because the bank makes less money on it. Conversely, very large loans might require more strict checks.

Common Mistakes to Avoid When Borrowing

Even with a personal loan calculator, borrowers can fall into traps. Here is how to stay safe.

Ignoring the Total Cost: Don't just look at the EMI. Look at the total amount repaid at the end of the loan.

Borrowing More Than Needed: It is tempting to take extra cash for a vacation, but you will pay interest on every cent.

Missing the Fine Print: Check for "prepayment penalties." Some lenders charge you a fee if you try to pay the loan off early to save on interest.

The Benefits of Personal Loans

If used correctly, personal loans are great tools. They are usually cheaper than credit cards. Using a personal loan calculator to replace high-interest credit card debt with a lower-interest personal loan is a smart move.

Fast Funding

Most personal loans are approved quickly. Some online lenders can put money in your account within 24 to 48 hours.

Fixed Payments

Unlike credit cards, where the minimum payment changes, a personal loan has a fixed EMI. This makes it very easy to plan your monthly budget.

Frequently Asked Questions (FAQs)

1. Does using a personal loan calculator affect my credit score? No. Using a calculator is just for your own information. It does not involve a credit check, so you can use it as many times as you like without any risk to your score.

2. Why is the interest rate on a personal loan higher than a car loan? A car loan is secured by the vehicle. If you don't pay, the bank takes the car. A personal loan has no collateral, so the bank charges more interest to cover the risk of you not paying.

3. Can I pay off my personal loan early? In most cases, yes. However, some banks charge a "prepayment penalty." You should check your loan agreement. If there is no penalty, paying early saves you a lot of money in interest.

4. What is a good interest rate for a personal loan? Interest rates change based on the economy and your credit score. Generally, anything below 10-12 percent is considered good, while rates for those with poor credit can go above 25 percent.

5. Is the EMI amount fixed for the whole tenure? Yes, for most personal loans, the interest rate is fixed. This means your monthly payment will stay exactly the same from the first month to the last month.

6. Should I choose a longer tenure to have a smaller EMI? Only if you absolutely have to. A smaller EMI is easier to pay each month, but you will end up paying much more in total interest over the life of the loan.

Conclusion

A personal loan calculator is a vital tool for anyone looking to borrow money responsibly. It removes the guesswork and provides a clear picture of your financial commitment. By understanding your EMI, interest costs, and tenure, you can make a choice that protects your financial future.

Remember to compare different lenders, check your credit score, and always read the terms and conditions. Being an informed borrower is the first step toward debt-free living. Use the personal loan calculator today to start your journey toward a better-managed budget.