5 Lakh Home Loan EMI for 10 Years: A Simple Beginner's Guide

Buying a house is a big milestone, and managing your loan smartly is the key to stress-free ownership. If you are planning to take a smaller loan or looking to top up an existing one, you might be calculating the monthly costs.

Specifically, you want to know what a 5 lakh home loan EMI for 10 years looks like in real numbers. This guide cuts out the confusing bank jargon to give you plain, honest facts.

We will break down exactly how much you will pay each month, how interest rates change your total bill, and how you can save cash on your bank payments.

Google Featured Snippet Answers

What is the monthly EMI for a 5 lakh home loan for 10 years? The monthly EMI for a 5 lakh home loan for 10 years generally ranges from six thousand rupees to six thousand seven hundred rupees. The exact amount depends entirely on your bank's interest rate, which typically hovers between seven percent and eleven percent per annum based on your personal credit profile.

How much total interest do you pay on a 5 lakh loan over 10 years? On a five lakh loan with a ten-year tenure, your total interest payout will be around two lakh rupees to three lakh fifteen thousand rupees. This means your total repayment amount back to the lending bank over the decade will sit between seven lakh rupees and eight lakh fifteen thousand rupees.

Can you reduce your 10-year home loan EMI? Yes, you can reduce your monthly payment by making a higher down payment initially or by maintaining a high credit score above 750 to secure lower interest rates. You can also make partial prepayments during the loan tenure to reduce your remaining principal balance quickly.

Understanding Your 5 Lakh Home Loan EMI for 10 Years

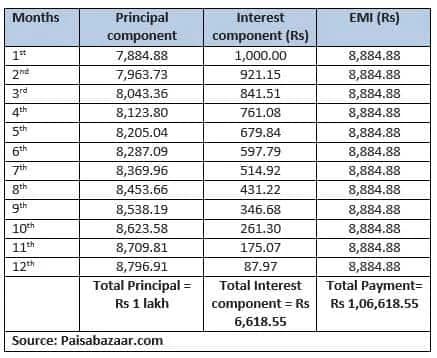

Before you sign any bank paperwork, you need to understand how your monthly Equated Monthly Instalment, or EMI, is calculated. Every single monthly payment you make is split into two parts: the principal amount and the interest fee.

The principal is the actual five lakh rupees you borrowed to buy your house. The interest is the fee the bank charges you for letting you borrow their money.

In the early years of your ten-year tenure, a bigger portion of your monthly payment goes toward paying off the interest. As time passes, more of your money goes toward reducing the actual principal balance.

Expected Monthly Payment Table

Because market interest rates fluctuate, your actual monthly bill will change depending on the lender you choose. Here is a clear breakdown of what your monthly payments will look like at different interest percentages:

Loan Amount | Interest Rate (Per Year) | Monthly EMI | Total Interest Paid | Total Repayment |

5 Lakhs | 7.5% | 5,935 Rupees | 2,12,242 Rupees | 7,12,242 Rupees |

5 Lakhs | 8.5% | 6,199 Rupees | 2,43,912 Rupees | 7,43,912 Rupees |

5 Lakhs | 9.5% | 6,470 Rupees | 2,76,389 Rupees | 7,76,389 Rupees |

5 Lakhs | 10.5% | 6,747 Rupees | 3,09,644 Rupees | 8,09,644 Rupees |

Key Factors That Decide Your Housing Loan Cost

Your monthly budget is affected by several moving pieces. Understanding these factors helps you negotiate a better deal with your lender.

1. Your Personal Credit Score

Your credit score is a three-digit number that tells banks how responsible you are with your finances. If your score is above 750, banks view you as a safe borrower and will give you their lowest rates.

If your score is low because of late payments or existing credit card debts, banks will charge you a much higher interest percentage. This extra percentage can add thousands of rupees to your total interest bill over ten years.

2. Type of Interest Rate Selected

When you apply for a housing loan, you will choose between a fixed rate and a floating rate:

Floating Rate: This rate is tied to central bank benchmarks and can go up or down over time. It usually starts lower, making it popular for long-term buyers.

Fixed Rate: This rate stays exactly the same for your entire ten-year window. It offers great predictability but usually costs a bit more upfront.

3. Extra Fees and Processing Charges

The total cost of your loan is not just the interest rate. Banks also charge a processing fee to verify your property and paperwork.

These fees usually range from 0.25% to 1.00% of your total loan value. Make sure to ask about these upfront costs so you are not caught off guard by extra fees when the loan gets approved.

Smart Ways to Lower Your Monthly Payments

No one wants to pay more money to a bank than they absolutely have to. Use these honest, simple tips to keep your loan expenses as low as possible.

Build a Strong Down Payment

Even though you are looking at a smaller five lakh loan, paying a bit more cash upfront reduces the amount you actually need to borrow. A smaller loan means smaller monthly payments and much less interest spent over the decade.

Choose a Shorter Tenure Wisely

A ten-year loan is an excellent choice because it keeps you from trapped in debt for twenty or thirty years. While a shorter timeline means your monthly payment is higher, it saves you massive amounts of money on long-term interest costs.